The next generation to retire is likely to have much lower retirement savings. Those aged 40 to 55 are effectively a lost generation.

They have limited defined benefit (DB) pensions as many occupational schemes closed early on in their careers and it took the government many years to develop and implement auto-enrolment.

These are some of the underlying themes of the 2019 UK Defined Contribution (DC) Investment Forum (DCIF) report. A summary and discussion of this report was recently published in an IPE Article.

The key findings of the DCIF Report:

- Members are sleepwalking into retirement and choosing the path of least resistance

- The industry has been slow to address the challenges posed by pension freedoms

- The best approach is seen as income drawdown in earlier years and longevity protection later in retirement

- Further policy initiatives are required to build consensus and provide clarity

In summary, “The DC industry needs to do more to address post-retirement challenges”.

There are obviously issues specific to the UK market e.g. it has been five years since pensioners in the UK gained greater freedom to use their defined contribution (DC) pots.

Nevertheless, retirement issues are universal and key learnings can be gained from individual markets.

The IPE article outlined the key challenge facing providers: “how do you ensure members retain flexibility and choice, while ensuring those members can manage both the investment and longevity risk over decades of retirement?”

Overall, the UK industry response has been slow. It appears “Pension providers have been focused on designing the best default fund with little energy spent on the post-retirement phase.”

Interestingly, research in the UK by Nest, a €8.3bn auto-enrolment provider, found most members expect their pension pot to pay an income automatically on retirement.

Members are also surprised by the level of complexity involved in draw down products.

Post Retirement Investment Solution Framework

Despite the lack of innovation to date there appears to be a consensus about the shape of the post-retirement investment solution.

An appropriate Post-Retirement Investment Strategy would allow retirees to have decent levels of income during the first two active decades of retirement and longevity protection for after 80.

“Not only does this remove the burden of an unskilled person having to manage both investment and longevity risk, but it also prevents members from either underspending or overspending their pots”.

The idea is to turn a DC pension pot into an income stream with minimal interaction from the scheme member.

This is consistent with the vision expressed by Professor Robert Merton in 2012, see this Kiwi Investor Blog Post: Designing a new Retirement System for more detail.

As the IPE article highlights, it is important retirees are provided guidance to ensure they understand their choices.

Albeit, a core offering will deliver a sustainable income. This is potentially a default solution which can be opted out of at any stage.

Some even argue that the “trustees would then make a judgement about what a sustainable income level would be for each member and then devise a product to pay this out.”

“In addition, this product could also provide a small pot of cash for members to take tax-free on retirement as well buying later-life protection. This could take the form of deferred annuities or even a mortality pool.”

Early Product Development in the UK

The IPE article outlines several approaches to assist those entering retirement.

By way of example, Legal & General Investment Management have developed a retirement framework which they call ‘four pots for your retirement’.”

- First pot is to fund the early years of retirement – assuming retirees will spend the first 15 years wanting to enjoy no longer working; they will travel and be active.

- Second pot provides a level of certainty to ensure retirees do not outlive their savings, this may include an annuity type product.

- Third pot is a rainy-day pot for one-off expenses.

- Final pot is for inheritance.

Greater Policy Direction

Unsurprisingly, there is a call for clearer policy direction from Government. Particularly in relation to adequacy, and the relation between adequacy and retirement products.

Unlike a greater consensus around what an investment solution might look like, consensus around the regulatory environment will be harder to achieve.

This may slow investment solution innovation to the detriment of retirees.

Concluding remarks

The following point is made within the IPE article: “While pension providers in both the US and Australia have come to the same conclusions as the UK about the way to address the retirement market, no-one in these markets has yet developed a viable product.”

As the IPE article note “It is likely the industry will be pushing at an open door if it develops a product that provides an income in retirement.”

This is a significant opportunity for the industry.

Interestingly, the investment knowledge is available now to meet the Post Retirement challenge. Also, Post-Retirement Investment solutions are increasingly being developed and are available. It is going to take a change in industry mind-set before they are universally accepted.

The foundations of the investment knowledge for the Post-Retirement Investment solution as outlined above have regularly been posted on Kiwi Investor Blog.

For those wanting more information, see the following links:

- A key foundation knowledge is Liability Driven Investing (LDI): More on Liability Driven Investing (LDI) for beginners. LDI is used by insurance companies and Defined Contribution Fund to manage their investments to match future cashflows/Income requirements.

- There needs to be a greater focus on generating Income in retirement during the accumulation phases: What Matters for Retirement is Income not the Value of Accumulated Wealth.

- Goal-Based Investing (GBI) is the wealth management application of LDI. The EDHEC Risk Institute GBI framework is amongst the most comprehensive and practical available. I try to do it justice in this Post: A More Robust Retirement Income Solution.

- EDHEC also advocate the concept of flexicurity. Flexicurity is the concept that individuals need both security and flexibility when approaching retirement investment decisions: Flexicurity in Retirement Income Solutions – making finance useful again.

- This Post: Evolution within the Wealth Management Industry, the death of the Policy Portfolio, builds on the concepts above and notes a paradigm shift within the industry to address the Post Retirement challenges. EDHEC provide a framework for the Mass-Customisation of the Retirement investment solution, which is very powerful.

There will be change, a paradigm shift is already occurring internationally, and those savings for retirement need a greater awareness of these developments and the likely Investment Solution options available, so that they are not “sleepwalking into retirement and choosing the path of least resistance”.

I don’t see enough of the Post Retirement Challenges being addressed in New Zealand by solution providers. More needs to be done, the focus in New Zealand has been on accumulation products and the default option as occurred in the UK.

The approach to date has been on building as big as possible retirement pot, this may work well for some, for others not so well.

Investment strategies can be developed that more efficiently uses the pool of capital accumulated – avoiding the dual risks of overspending or underspending in the early years of retirement and providing a greater level of flexibility compared to an annuity.

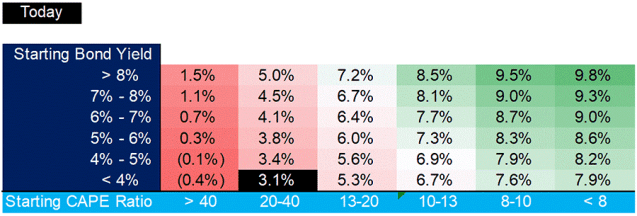

These strategies are better than Rules of Thumb, such as the 4% rule which has been found to fail in most markets.

More robust and innovative retirement solutions are required.

In New Zealand there needs to be a greater focus on decumulation, Post Retirement solutions, including a focus on generating a secure and stable level of income throughout retirement.

The investment knowledge is available now and being implemented overseas.

Let’s not leave it until it is too late before the longevity issues arise for those retiring today and the next generation, who are most at risk, begin to retire.

Happy investing.

Please read my Disclosure Statement