Over the years Kiwi Investor Blog has covered alternatives and the benefits they can bring to a well-diversified portfolio. What I have not done is provide a practical framework for how to actually introduce them.

This post attempts to do that. It is not a complete list. Think of it as a starting point.

A word on scope first. This is not an argument against equities and bonds. They will remain the core of most well-constructed portfolios and rightly so.

The case for alternatives is about enhancing those exposures, improving the overall risk and return profile of a portfolio, and building a portfolio that is more resilient across a range of different market environments.

The inclusion of alternatives is additive, not a replacement. Portfolio evolution, not revolution.

A Different Mindset Is Worth Considering

Successfully introducing alternatives into a portfolio is as much about mindset as it is about manager selection or asset allocation. The mindset question comes first.

A return-focused approach to investing, where the primary goal is maximising returns, beating a benchmark, or ranking well against peers, is a perfectly reasonable starting point for a traditional portfolio of equities and bonds. Returns are visible, measurable, and easy to communicate. There is nothing wrong with this orientation.

When it comes to including alternatives, a somewhat different way of thinking tends to be more useful. The investors who have most successfully built alternatives into their portfolios have generally approached the question from the perspective of risk and resilience first, with return as the outcome rather than the objective. The shift is subtle but it matters.

Rather than asking “how do we get more return?”, the question becomes “how do we build a portfolio that holds up well across a range of economic environments, and what role can alternatives play in that?” It is a different frame, and it opens up different possibilities.

This mindset is also consistent with maximising returns and ranking well against peers. Actually, it could be argued this mindset increases the probability of achieving these objectives.

This point is worth dwelling on, because it is subtle but important. Expected return is a single number, a central estimate of where a strategy might land on average. What an investor actually experiences, however, is just one outcome from a wide range of possibilities. A strategy with a higher expected return but a wide spread of potential outcomes may, in practice, have a lower probability of meeting a given return target than a strategy with a slightly lower expected return but a narrower spread.

Including alternatives can increase the probability of achieving an objective, even where the expected return of the portfolio is similar, or modestly lower. By reducing volatility around that expected return, alternatives can narrow the range of likely outcomes, which in turn lifts the probability of landing at or above whatever return is actually required. The goal shifts from maximising expected return to maximising the probability of achieving the return that is needed, a subtly different objective, but one that tends to align more closely with what investors are actually trying to do.

We will expand on this below, as alternatives have different roles to play in a well-diversified portfolio.

Anchoring to Goals and Outcomes Over the Cycle

This mindset shift is perhaps the most practical: moving from benchmark-relative thinking to goal-based thinking. Rather than measuring success against an index, the focus is on achieving clearly defined risk and return outcomes over the full market cycle. A market cycle is typically five to seven years.

The questions this raises are straightforward but important. What does the portfolio actually need to achieve? What income needs to be generated, and when? What level of drawdown is genuinely tolerable? What does success look like at the end of the investment horizon?

These questions are applicable for all investors, including KiwiSaver funds, those planning for retirement, charitable trusts, and ultra-high net worth individuals.

These different investors will have different answers. A charitable endowment might need to preserve real capital while distributing 4–5% per annum. A KiwiSaver member approaching retirement might prioritise avoiding a sharp drawdown in the final years before withdrawal. A family office might focus on inflation protection and multi-generational income. Each implies a different portfolio.

This longer-term, outcome-oriented framing is also what creates the right conditions for alternatives to be included. Once success is measured over a cycle rather than a quarter, the illiquidity of private markets becomes more of a feature than a constraint.

The investors who have thought carefully about their genuine liquidity needs, and found they can afford to look through short-term fluctuations, have generally been rewarded for it.

From Asset Allocation to Risk Allocation

A natural extension of this thinking is to consider not just how capital is allocated across asset classes, but how risk is allocated.

In a traditional 60/40 portfolio, roughly 90% of the portfolio’s volatility comes from equities, even though equities represent only 60% of the capital. The portfolio looks diversified on paper but is, in terms of risk, heavily concentrated. Making this visible is a useful exercise: it often motivates a genuine rethink of what diversification actually means in practice.

As I have written previously on this blog, true portfolio diversification does not come from investing in many different asset classes, it comes from investing in different risk factors. That is a foundation principle.

True diversification requires exposure to different risk factors. That is what alternatives, thoughtfully selected, can provide.

Designing for a Range of Environments

One of the most helpful ways to think about portfolio construction, and one that lends itself naturally to the inclusion of alternatives, is to design for uncertainty rather than optimise for a single forecast. Markets move in ways that surprise us. Economic conditions shift. What works well in one environment may struggle in another.

A useful starting point is to consider how a portfolio would perform across different economic conditions: periods of rising growth, falling growth, rising inflation, and falling inflation.

No single asset class does well in all four. Equities tend to thrive in rising growth and benign inflation. Bonds provide ballast in slowing growth and deflation. Real assets and inflation-linked securities come into their own when prices are rising.

A portfolio with some exposure across all of these environments is likely to be more resilient over time than one concentrated heavily in just one or two.

This way of thinking naturally leads to a broader set of portfolio building blocks, and alternatives, thoughtfully chosen, are part of that broader investment set.

Thinking About Downside, Not Just Upside

Another useful shift is to give more weight to downside protection. Returns compound, and losses interrupt compounding. A portfolio that falls 50% needs to gain 100% just to recover. Avoiding large drawdowns is not timidity; it is one of the more powerful tools available to long-term investors.

Thinking about the conditions under which a portfolio might suffer badly, and whether those risks have been adequately addressed, is a worthwhile complement to thinking about return potential. It does not mean avoiding risk. It means being deliberate about which risks are taken, and ensuring the portfolio is not unduly exposed to a single adverse scenario.

This framing also helps evaluate alternatives more clearly. A trend following strategy, for example, is often most useful not because it outperforms equities but because it tends to hold up, or even contribute positively, when equities are under stress. Evaluating alternatives on those terms, rather than purely against a return benchmark, tends to lead to better portfolio construction decisions.

A Framework for Thinking About Alternatives

Alternatives are not a monolith. Each category serves a different purpose within a portfolio, and understanding those purposes is critical to building a coherent strategy.

As Preqin have noted, investors’ motivations for investing in alternatives are quite distinctive. A useful way to think about this is through the lens of what each alternative brings to the table.

Private Equity — Access to companies and growth opportunities not available on public markets. The evidence for long-run outperformance over listed equities is well established, particularly among top-quartile managers. The trade-off is illiquidity and manager selection risk. Private equity rewards investors with long time horizons and the patience to stay the course.

Infrastructure (Unlisted) — Real, long-duration assets (e.g. toll roads, utilities, airports, renewable energy) that generate stable, predictable cash flows, often with inflation linkage. For portfolios with long-term income objectives, unlisted infrastructure is particularly compelling. It also tends to have lower correlation with listed markets, which is precisely the point.

Private Debt — Loans and credit instruments made outside the public bond markets. Private debt has grown substantially since the global financial crisis as banks retrenched from certain lending markets. It typically offers a meaningful yield premium over public credit in exchange for illiquidity, an attractive trade for investors who do not need immediate access to their capital.

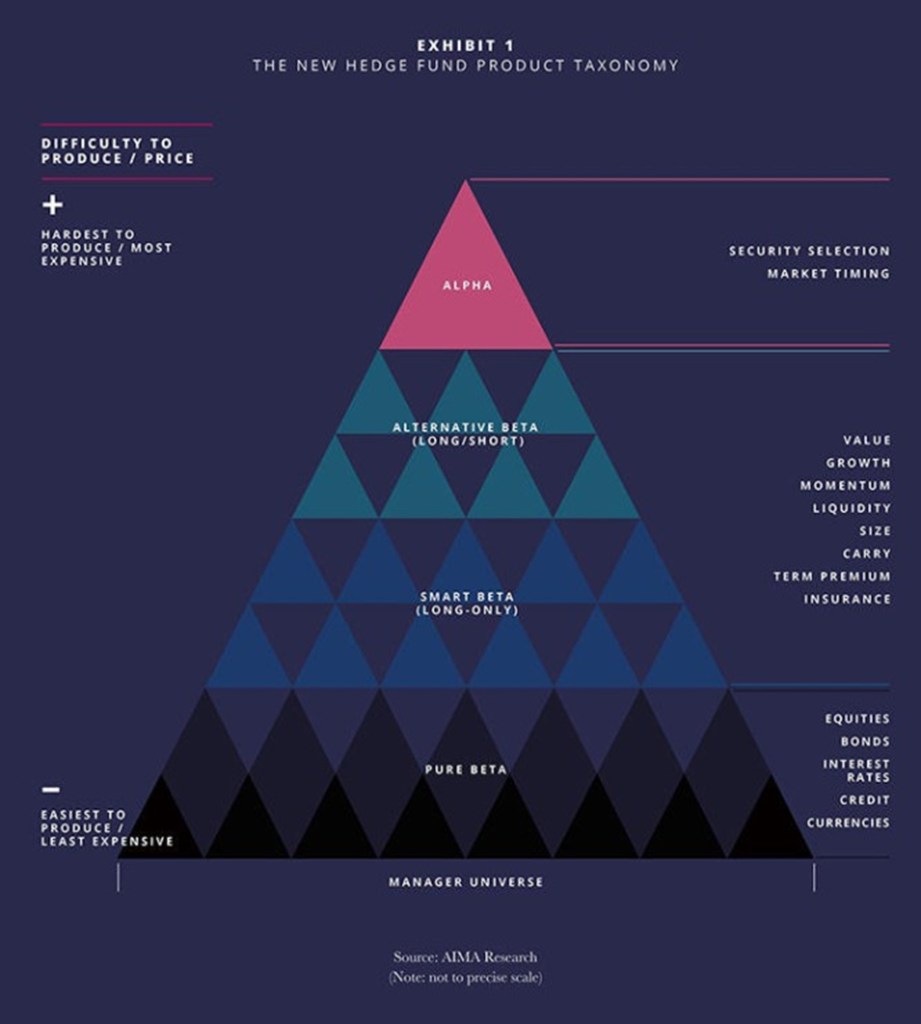

Hedge Funds (and Alternative Risk Premia) — A broad category, but at their best, hedge fund strategies can provide genuine diversification: returns that are lowly correlated with both equities and bonds. Managed futures, global macro, and market-neutral strategies have historically performed well precisely when traditional portfolios have struggled. Not all hedge funds deliver on this promise. Manager selection and fee discipline matter enormously here.

The Attraction of Alternatives

Alternatives are generally added to portfolios for two primary reasons.

- Enhance returns — for example, private equity and venture capital, where the objective is to access return premiums not available in public markets.

- Diversification — for example, hedge funds and liquid alternatives, used to reduce portfolio declines at times of severe sharemarket falls.

Inflation hedging and yield enhancement are other reasons for allocating toward alternatives.

The motivations behind each allocation are quite distinctive. A Preqin survey of institutional investors found that investors’ reasons for holding different alternative asset classes vary considerably depending on the role each is expected to play in the portfolio. I covered this in more detail in Further growth expected for an Alternative future – Preqin.

The table below summarises the key findings.

| Alternative Asset Class | Primary Investor Motivations |

| Private Equity and Venture Capital | High absolute and risk-adjusted returns |

| Infrastructure and Real Estate | An inflation hedge and a reliable income stream |

| Private Debt | High risk-adjusted returns and an income stream |

| Hedge Funds | Diversification and low correlation with other asset classes |

| Natural Resources | Diversification and low correlation with other asset classes |

| Insurance-Linked Securities | Income and diversification |

What stands out from this table is that no single alternative is being held for the same reason. Some are held for return enhancement, some for income, some for inflation protection, and some purely for diversification. This reinforces the broader point made: alternatives are not a single decision but a set of distinct building blocks, each chosen for a specific role within the overall portfolio.

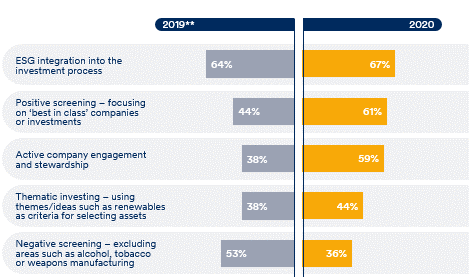

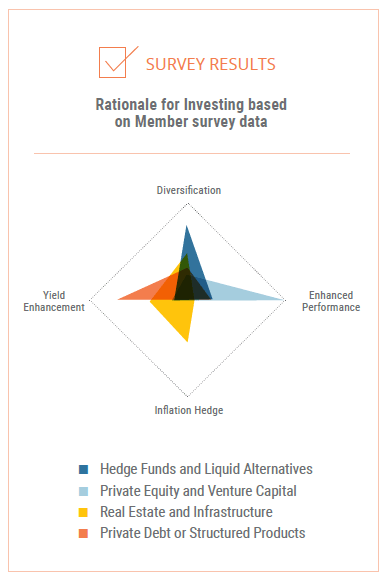

Consistent with the above commentary, the following graph presents the rationale for investing in alternatives based on the CAIA Members surveyed in 2020.

Practical Considerations: Liquidity, Fees, and Manager Selection

Moving into alternatives is not without complexity. Three issues deserve careful consideration.

Liquidity is the most important starting point. Before allocating to illiquid strategies, investors should rigorously assess their true liquidity needs, not their perceived needs, but their actual cash flow requirements over a 5–10 year horizon. Liquidity should be treated as a budget: deploy it wisely.

Fees in alternatives are higher than in traditional asset classes, and that is a legitimate consideration. But higher fees are not automatically a problem. What matters is the return after fees. A private equity fund that delivers 4–5% above public equity returns net of all costs is clearly worthwhile. Every alternative should be assessed on its after-fee contribution to the portfolio. For a more detailed discussion on fees and alternatives, please see my previous post Investment Fees and Investing like an Endowment – Part 2.

Manager selection matters far more in alternatives than in listed markets. The spread between top-quartile and bottom-quartile private equity managers, for example, is enormous, far greater than the equivalent spread in traditional asset classes. Gaining access to top-tier managers is both critical and, for many smaller investors, genuinely challenging. Although fund-of-funds structures, co-investment platforms, and specialist advisers can all play a role here, the layering of fees and risk exposures is important, e.g. the liquidity framework.

Where to Start

For investors new to alternatives, a phased approach is sensible. A reasonable starting point for a medium-to-long-term investor might include the following:

- Set a target allocation of 10–15% as an initial ambition, with the intention to build over time as governance capability and manager relationships develop.

- Start with the most accessible categories. Unlisted infrastructure, private equity, and private debt tend to be more straightforward entry points than hedge funds. They are also easier to explain to stakeholders.

- Build governance capability first. Alternatives require more active oversight, deeper due diligence, and clearer investment policy frameworks than listed strategies.

- Commit across vintages. Private markets operate on multi-year cycles. Spreading commitments across different vintage years reduces timing risk significantly.

Pulling It Together

The argument here is not that equities and bonds should be abandoned, far from it. They remain the foundation of a well-constructed portfolio.

The argument is that a portfolio composed only of equities and bonds is leaving risk-adjusted return potential on the table, and accepting a concentration of risk that long-term investors can afford to reduce.

The mindset shift comes first: from a focus on return to one of risk management and resilience, from benchmark-beating to goal achievement, from optimising for one environment to building a portfolio that can perform across many. The framework for alternatives follows naturally from that shift.

The world’s best long-term investors understood this a long time ago. The opportunity for New Zealand investors, whether managing KiwiSaver assets, endowment funds, or family wealth, is to apply the same thinking here. The evidence is clear. The framework exists.

Happy investing.

Disclosure

Please read the Kiwi Investor Blog Disclosure Statement before relying on any information in this post. This blog is written for information and discussion purposes only. Nothing in this post constitutes financial advice. All investment strategies involve risk, including the loss of principal. Readers should seek independent financial advice before making any investment decisions. The views expressed in this post are my own and do not represent the views of my employer or any organisation with which I am affiliated.