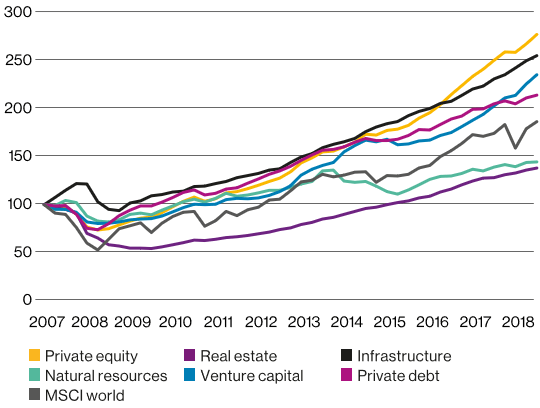

Avoiding large market losses is vital to accumulating wealth and reaching your investment objectives, whether that is attaining a desired standard of living in retirement or an ongoing and uninterrupted endowment.

The complexity and different approaches to providing portfolio protection (tail-risk hedging) has been highlighted by a recent twitter spat between Nassim Nicholas Taleb, author of Black Swan, and Cliff Asness, a pioneer in quant investing.

The differences in perspectives and approaches is very well captured by Bloomberg’s Aaron Brown article, Taleb-Asness Black Swan Spat Is a Teaching Moment.

I provide a summary of the contrasting perspectives in the Table below as outlined by Brown’s article, who considers both men as his friends.

There are certainly some important learnings and insights in contrasting the different approaches.

PIMCO recently published an article Hedging for Different Market Scenarios. This provides another perspective.

PIMCO provide a brief summary of different strategies and their trade-offs in diversifying a Portfolio.

They outline four approaches to diversify the risk from investing in sharemarkets (equity risk).

In addition to tail risk hedging, the subject of the twitter spat above between Taleb and Asness, and outlined below, PIMCO consider three other strategies to increase portfolio diversification: Long-term Fixed Income securities (Bonds), managed futures, and alternative risk premia.

PIMCO provide the following Graph to illustrate the effectiveness of the different “hedging” strategies varies by market scenario.

As PIMCO note “it’s important for investors to know in what types of environments each strategy is more likely to work and in what environments each are likely to be less effective.”

As they emphasise “not every type of risk-mitigating strategy can be expected to work in every type of market sell-off.”

A brief description of the diversifying strategies is provided below:

- Long Bonds – holding long term (duration) high quality government bonds (e.g. US and NZ 10-year or long Government Bonds) have been effective when there are sudden declines in sharemarkets. They are less effective when interest rates are rising. (Although not covered in the PIMCO article, there are some questions as to their effectiveness in the future given extremely low interest rates currently.)

- Managed Futures, or trend following strategies, have historically performed well when markets trend i.e. there is are consistent drawn-out decline in sharemarkets e.g. tech market bust of 2000-2001. These strategies work less well when markets are very volatile, short sharp movements up and down.

- Alternative risk premia strategies have the potential to add value to a portfolio when sharemarkets are non-trending. Although they generally provide a return outcome independent of broad market movements they struggle to provide effective portfolio diversification benefits when there are major market disruptions. Alternative risk premia is an extension of Factor investing.

- Tail risk hedging, is often explained as providing a higher degree of reliability at time of significant market declines, this is often at the expense of short-term returns i.e. there is a cost for market protection.

A key point from the PIMCO article is that not one strategy can be effective in all market environments.

Therefore, maintaining an array of diversification strategies is preferred “investors should “diversify their diversifiers””.

It is well accepted you cannot time markets and the best means to protect portfolios from large market declines is via a well-diversified portfolio, as outlined in this Kiwi Investor Blog Post found here, which coincidentally covers an AQR paper. (The business Cliff Asness is a Founding Partner.)

A summary of the key differences in perspectives and approaches between Taleb and Asness as outlined in Aaron Brown’s Bloomberg’s article, Taleb-Asness Black Swan Spat Is a Teaching Moment.

| My categorisations | Asness | Taleb |

| Defining a tail event | Asness refers to the worst events in history for investors, such as the 5% worst one-month returns for the S&P 500 Index.

Research by AQR shows that steep declines that last three months or less do little or no damage to 10-year returns. It is the long periods of mediocre returns, particularly three years or longer, that damages longer term performance. |

Taleb defines “tail events” not by frequency of occurrence in the past, but by unexpectedness. (Black Swan)

Therefore, he is scathing of strategies designed to do well in past disasters, or based on models about likely future scenarios.

|

| Different Emphasis |

The emphasis is not only on surviving the tail event but to design portfolios that have the highest probability of generating acceptable long-term returns. These portfolios will give an unpleasant experience during bad times.

|

Taleb prefers tail-risk hedges that deliver lots of cash in the worst times. Cash provides a more pleasant outcome and greater options at times of a crisis.

Investors are likely facing a host of challenges at the time of market crisis, both financial and nonfinancial, and cash is better. |

| Different approaches | AQR strategies usually involve leverage and unlimited-loss derivatives.

|

Taleb believes this approach just adds new risks to a portfolio. The potential downsides are greater than the upside. |

| Costs | AQR responds that Taleb’s preferred approaches are expensive that they don’t reduce risk.

Also, the more successful the strategy, the more expensive it becomes to implement, that you give up your gains over time e.g. put options on stocks |

Taleb argues he has developed methods to deliver cash in crises that are cheap enough that they actually add to long-term returns while reducing risk.

|

| Investor behaviours | Asness argues that investors often adopt Taleb’s like strategies after a severe market decline. Therefore, they pay the high premiums as outlined above. Eventually, they get tire of the paying the premiums during the good times, exit the strategy, and therefore miss the payout on the next crash. | Taleb emphasises the bad decisions investors make during a market crisis/panic, in contrast to AQR’s emphasis on bad decisions people make after the market crisis.

|

Good luck, stay healthy and safe.

Happy investing.

Please see my Disclosure Statement