Active engagement and stewardship have leapt in importance as a way for asset managers to drive sustainable change. This is a key conclusion of a study undertaken by Schroders in 2020.

Schroders conclude “The results suggest that engagement and voting are now increasingly being viewed as an important aspect of achieving change, rather than simply divesting.”

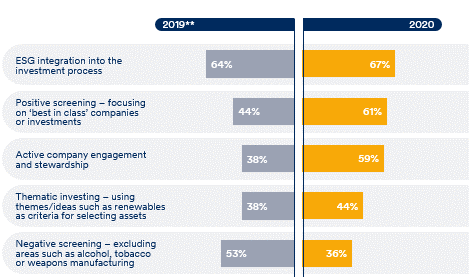

Their study found that nearly 60% of “institutions said active company engagement and stewardship was a key approach to integrating sustainability.” This is a significant rise on 38% a year ago.

The survey also highlighted:

- ESG Integration into the investment process and positive screening (focusing on the best in class companies) are the top two important drivers for asset managers to drive sustainable change;

- Positive screening has also grown sharply in importance, from 44% of survey respondence to 61%; and

- Conversely Negative Screening has fallen in importance (53% to 36%).

Investors noted signs of successful engagement included:

- Transparent reporting;

- Tangible outcomes; and

- Consistently voting against companies in order to drive change.

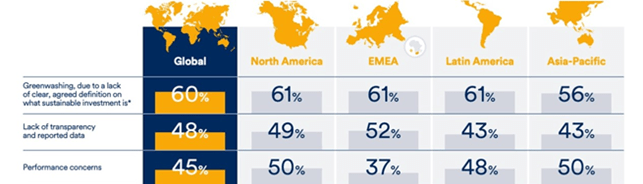

Greenwashing, poor data, and increased Regulation

Greenwashing, as described by Schroders “‘a lack of clear, agreed sustainable investment definitions’” was seen as the most significant obstacle to investor’s sustainable investment intentions. 60% of those surveyed found green-washing as one of the most significant obstacles impeding their sustainable investing intentions.

The lack of transparency and reported data was also raised as an issue restricting the ability to invest sustainably.

Both measures increased in importance on last year, while performance concerns continued to decline. 45% of investors cited performance as concern in relation to investing sustainably.

These results were recently picked up in an Alternative Investment Management Association (AIMA) article, which focused on the increased integration of ESG into Hedge Fund’s investment processes. Hedge funds start integrating ESG (aima.org).

In relation to green-washing, AIMA notes that regulators are also concerned about green-washing, noting the introduction of the Sustainable Finance Disclosure Regulation (SFDR) rule in the European Union. The SFDR came into effect on March 10 of this year, aimed at ensuring financial firms such as fund managers, insurers, and banks providing financial products and services comprehensively disclose just how committed to sustainability they truly are.

The AIMA notes “The EU rules will also create a taxonomy as regulators look to facilitate greater consistency in terms of what can be classified as being a sustainable economic activity.”

The AIMA also noted more global investors are now prioritising ESG, and it is something which hedge funds need to respond to. Although they felt the US was behind the rest of the world, particularly Europe (I would add Australian and New Zealand as well), this was changing.

By way of example, the AIMA article highlighted “that several high profile US institutions – including the likes of CALPERS and Wespath – have signed up to the UN-backed Net Zero Asset Owner Alliance, a consortium comprised of 30 of the world’s largest investors – all of whom have committed to reduce carbon emissions linked to the companies they invest in by 29% within the next four years.”

Failure to transition towards net zero is widely seen as a important risk management issue for companies. Arguably, companies failing to adapt or transition towards net zero will see their businesses and valuations suffer.

Lastly, AIMA highlighted the concerns over the quality of ESG data being disclosed by managers to their investors.

“One of the primary problems is that there are no harmonised ESG data standards. Instead, there are many different ESG standards and protocols, all of which have their own characteristics. With different managers subscribing to different ESG standards, the reports they produce for clients are often inconsistent and even contradictory. Similarly, ratings agencies will often have their own bespoke methods of collecting data from companies they are scoring. ……… Without a common data collection methodology, the ratings agencies’ scoring processes will be fragmented.”

Key Engagement Issues

The survey by Schroders found environmental issues remained the most important engagement issue for investors.

In total, 68% of investors globally said they expected investing sustainably to grow in importance over the next five years.

“Driving this focus were institutions looking to align their investments with their own corporate values, responding to regulatory and industry pressure, and, positively, the belief that investing sustainably can drive higher returns and lower risk.”

The Schroder study included 650 institutional investors encompassing $25.9 trillion in assets.

Please read my Disclosure Statement

For Outsourced Chief Investment Officer (OCIO) and investment consulting services please see here.