“ESG is not an equity return factor in the traditional, academic sense”.…… “Nevertheless, ESG can be a very powerful theme in the portfolio management process in the years ahead.”

These are two key conclusions from a recent Research Affiliates article, Is ESG a Factor?

ESG investing is incorporating Environment, Social and Governance considerations into investment portfolios.

Research Affiliates conclude “that ESG does not need to be a factor for investors to achieve their ESG and performance goals.”

They also call for greater clarity around exactly what ESG is and what it is not.

“Currently, various stakeholders are sending a whole host of mixed messages. Investors, particularly fiduciaries, need education and alignment. If ESG remains a heterogeneous basket of claims, we will likely never see it fulfill its vast promise.”

Lastly, they believe ESG is likely to be a powerful theme for the new owners of capital, in particular woman and millennials. Increasingly investors will prioritise ESG in their portfolios in the years ahead.

In my view, it is a stretch to say ESG is an investment factor in the context of Factor Investing. Nevertheless, the active management of ESG considerations into the investment process has the potential to add value.

You can’t capture the benefits of ESG by just being an ESG investor. Capturing the benefits from ESG are harder to attain relative to implementing an equity factor strategy such as value or low volatility.

The risks, and therefore the rewards of ESG, are more company specific.

Therefore, it is not good enough to say one incorporates ESG into the investment management process to gain the benefits from ESG.

There is no specific ESG factor that can be “harvested” passively. The ESG value add comes from implementing successfully and having the ability to identify company specific ESG risks.

What Is a Factor?

Before we can determine if ESG is an investment factor we first need to establish what an investment factor is.

In short, factors are characteristics associated with long-term risk and return outcomes associated with investing into a group of securities.

The “market”, sharemarkets and fixed income markets are factors themselves (Market Factors). We know that over time we can expect to generate a return over cash, a premia over cash (premia), from investing in sharemarkets, credit markets (corporate debt), and longer-term fixed income securities (interest rate duration).

Within markets there are also investment factors, which have been shown to deliver a premia (excess return adjusted for risk) over the “market factors” identified above.

The most common of these investment factors, and one receiving a lot of media attention currently, is the value factor. There are other well know and academically supported factors, including momentum, carry, quality, and low volatility. Investment factors are also known as Premias or Style Premia.

To be considered a robust investment factor, it is generally considered their needs to be support from an economic perspective or there is a behavioural-based explanation for the factor.

For those interested, I have previously Posted on Factor Investing, and this article on Andrew Ang discussing Factor Investment might also be of interest.

Research Affiliates have their own framework on determining the robustness of a Factor, which can be found here.

The Evidence – Is ESG an investment Factor?

To determine if ESG is a factor, Research Affiliates maintain it should satisfy the following three critical requirements, it should be:

- grounded in a long and deep academic literature;

- robust across definitions; and

- robust across geographies.

Academic Literature

The common factors of value, momentum, and low beta have been thoroughly researched and have a track record spanning several decades, as Research Affiliates conclude “very little debate currently exists regarding their robustness.”

In reviewing the academic literature on ESG, Research Affiliates find little agreement on the robust of generating excess returns. (Their article provides a good source of academic ESG research for those interested.)

In their view ESG is not an equity return factor in the traditional academic sense.

I have posted previously on the Research spanning Responsible Investing, see: Unscrambling the Sustainable Investing Return Puzzle.

In my mind there is value in undertaking a Responsible Investing approach, including the incorporation of ESG into the investment management process. This can be the case yet ESG not be a Factor as defined in academia. The research covered in the above Post provides support for this view.

Factors should be robust across definitions.

This is an interesting observation. Research Affiliates argue that “even slight variations in the definition of a factor should still produce similar performance results.”

They use value as an example, using different valuation metrics for value results in similar results over the longer-term. The value factor is robust across different definitions of value.

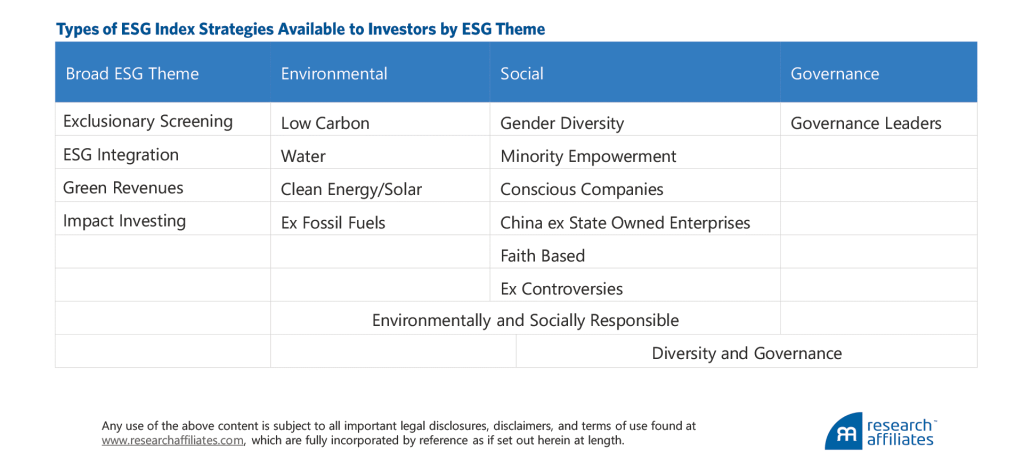

Unfortunately, ESG does not have a common definition and is a broad continuum of philosophies, approaches, and strategies.

See a previous Post discussing the continuum of Responsible Investing, which includes ESG: Sustainable Responsible Investing Spectrum

The broad spectrum is highlighted in the following Table presented in the Research Affiliates article to emphasise “ESG has no common standard definition and is a broad term that encapsulates a range of themes and subthemes.”

As they note, the strategies align more with investor preferences rather than a particular investment factor.

In the article Research Affiliates present the findings of their research to display how variations in the definition of ESG results in different performance outcomes.

From this analysis, they conclude:

- None of the ESG strategies as defined displayed material excess returns;

- There was a lack of historical track record, which is a significant impediment to conducting research in ESG investing; and

- Only after decades of quality data will it be possible to accurately test the claim that EG is a robust factor.

Research Affiliates also highlight there is an issue with the lack of consistency among ESG rating providers which hinders the ability to determine if ESG is a robust factor. They provide an example of this in the Article.

With regards to the last requirement, Research Affiliates find that ESG performance results are not robust across regions.

ESG Is Not a Factor, but Could Be a Powerful Theme

“ESG does not need to be a factor for investors to achieve their ESG and performance goals.”

Encouragingly, Research Affiliates see a role for the incorporation of ESG within an investment portfolio. I Agree!

They highlight that there are companies with poor ESG characteristics and that these risks should be incorporated into the stock selection process.

These risks are company specific risks, idiosyncratic risks technically speaking.

Research Affiliates consider carbon as an example, particularly coal. Notably there has been a move away from coal in the US. Therefore, “Investment managers who do not consider and integrate the ESG risk of, in this case, climate change may be blindsided.”

The successful implementation of ESG is a key determinant in capturing the value from company specific characteristics. Specifically, having the ability to identify mispricing of securities due to ESG risk.

It is not good enough to say one incorporates ESG into the investment management process and therefore the portfolios will benefit.

There is no a specific ESG factor that can be “harvested” passively, the value add comes from implementing successfully and having the ability to identify company specific risks.

Increasing Adoption of ESG Investing

Lastly, and quickly, Research Affiliates note that there is a “large shift in investor preference toward ESG is occurring as two distinct groups—women and millennials—take greater control of household assets.” This is backed up by third party research which notes that there will be a wave of assets ready to invest in highly rated ESG companies.

A regulatory push globally is also likely to accelerate this trend.

Happy investing.

Please see my Disclosure Statement