The Value Factor (value) offers the potential for additional returns relative to the broader sharemarket in the years ahead.

Exploring an array of different investment strategies and questioning the role of bonds in a portfolio are key to building a robust portfolio in the current low interest rate environment.

There will also be a need to be more dynamic and flexible to take advantage of market opportunities as they arise.

From this perspective, a value tilt within a portfolio is one investment strategy to consider in potentially boosting future investment returns.

The attraction of Value

Evidence supporting a value tilt within a robust portfolio is compelling, albeit opinion is split.

Nevertheless, longer-term, the “Rotating into Value stocks offers substantial upside in terms of return versus the broad market” according to GMO.

GMO presents the case for a value tilt to navigate today’s low interest rates in their Second Quarter 2020 Letter, which includes two insightful articles, one by Ben Inker and another by Matt Kadnar.

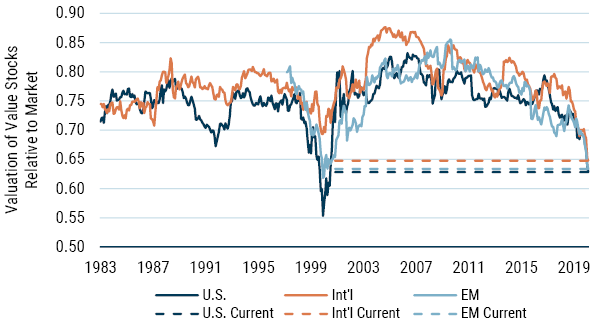

Value is at cheapest relative to the broader market since 1999, based on GMO’s analysis. Value is in the top decile of attractiveness around the world, as highlighted in the following figure.

Spread of Value for MSCI Regional Value Factors (GMO)

Is Value Investing Dead

As mentioned, the opinion on value is split.

A research paper by AQR earlier in the year addressed the key criticisms of value, Is (Systematic) Value Investing Dead?

For a shorter read on the case for value Cliff Asness, of AQR, Blog Post of the same title is worth reading.

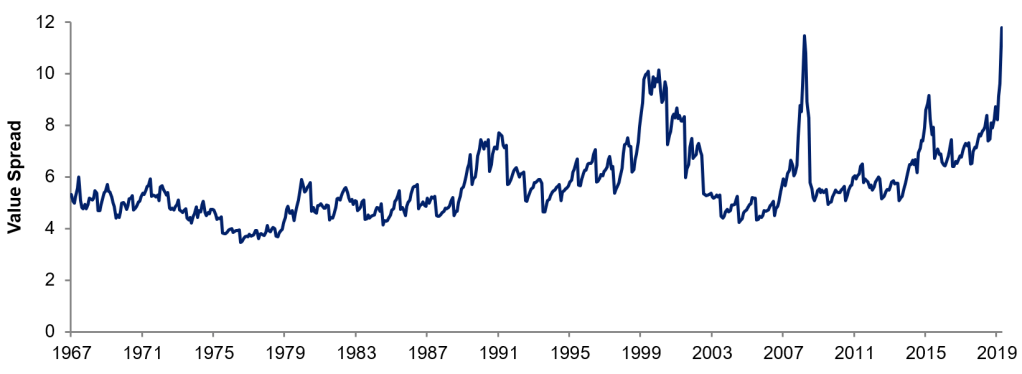

AQR’s analysis is consistent with GMO’s, as highlighted in the Graph and Table below.

The Graph below measures the Price-to-Book spread of the whole US sharemarket from December 1967 to March 2020.

This spread was at the 100th percentile versus 50+ years of history on the 31 March 2020 i.e. value is at it cheapest based on 50 years of data.

Price-to-Book Spread (AQR)

Asness’s Blog Post highlights “expensive stocks are sometimes only <4x as expensive as the cheap stocks, the median is that they are 5.4x more expensive, but today they are almost 12x more expensive.” (March 2020).

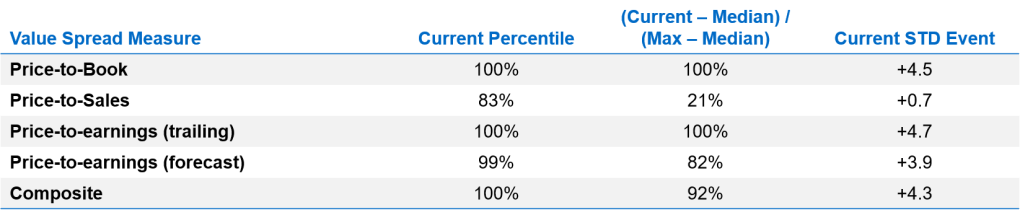

It is the same story when looking at different measures of value for the US sharemarket, as highlighted in the Table below.

Value is at its cheapest on many measures (AQR)

‘Don’t ask the barber whether you need a haircut’

This quote by Warren Buffett springs to mind when considering the analysis from GMO and AQR, both being value orientated investors. As Asness states, AQR has a horse in the race.

However, as outlined in his Post, he undertakes the same analysis as above and controls for, just to name a few:

- Excluding all Technology, Media, and Telcom Stocks

- Excluding the largest stocks

- Excluding the most expensive stocks

- Industry bets

- Industry neutrality

- Quality of company

Analysis is also undertaken using other measures of value, Price-Sales, P/E, using trailing and forecast earnings (these are in addition to Price-Book).

The attraction of value remains based on different measures of value and when making the adjustments to market indices as outlined above.

Asness argues value is exceptionally cheap, probably the cheapest it has ever been in history (March 2020).

The AQR analysis shows this is not because of an outdated price-to-book nor because of the dominance of highly expensive mega-cap stocks. Investors are paying more than usual for stocks they love versus the ones they hate. There is a very large mispricing.

The AQR research paper mentioned above, looked at the common criticisms of value, such as:

- increased share repurchase activity;

- the changing nature of firm activities, the rise of ‘intangibles’ and the impact of conservative accounting systems;

- the changing nature of monetary policy and the potential impact of lower interest rates; and

- value measures are too simple to work.

Across each criticism they find little evidence to support them.

Are we there yet?

We do not know when and how the valuation gap will be closed.

Nevertheless, the evidence is compelling in favour of maintaining a value tilt within a portfolio, and certainly now is not the time to give up on value.

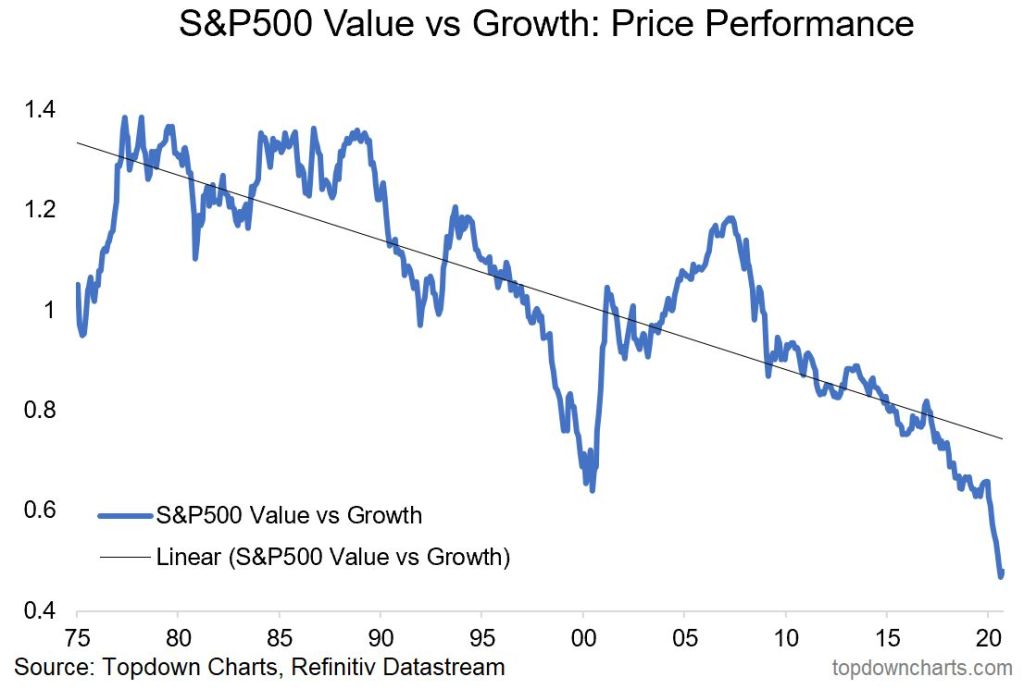

This is not a widely popular view, and quite likely a minority view, given the underperformance of value over the last ten years. As clearly demonstrated in the Graph below provided by Top Down Charts.

However, from an investment management perspective, the longer-term odds are in favour of maintaining a value tilt and thereby providing a boost to future investment returns in what is likely to be a low return environment over the next ten years.

It is too early to give up on value, news of its death are greatly exaggerated, on this, Asness makes the following point, value is “a strategy that’s “worked” through the 1920s – when a lot of stocks were railroads, steel, and steamship companies – through the Great Depression, WWII, the 1950s – which included some small technological changes like rural electrification, the space race and all the technology that it spanned – the internet age (remember these same stories for why value was broken back in 1999-2000?)………. Value certainly doesn’t depend on technological advancement being stagnant! But in a time when it’s failed for quite a while (again, that just happens sometimes even if it’s as good as we realistically think it is), it’s natural and proper that all the old questions get asked again. Is now different?”

I don’t think so.

Please see my Disclosure Statement