The greatest risk to the global economy is that economic activity surprises on the upside in 2021.

Currently consensus forecasts are for the global economy to grow 5.8% in 2021, lead higher by the US 5.7%, China 8.5%, and India 9.4%.

Global economic consensus forecasts are likely to move higher as the year progresses, reflecting:

economic activity surprises on the upside post COVID-19 vaccination reopening,

which will be supported by very low interest rates and the expected continuation of accommodative policy by central banks for some time to come, and

the very large government spending packages being rolled out. For example, the recently proposed $2.2 trillion spending package on infrastructure and other benefits over the next 10 years by President Biden in the USA, this is addition to $1.9tn spending stimulus he announced earlier in the year (American Rescue Plan).

The size of the US government spending program is huge, $5 trillion in measures have been announced since March 2020, over 80% of this will be “spent” by the end of 2021. This does raise economic risks for the future and $2 trillion in tax increases is being planned.

Concerns over inflation overdone……………for the time being.

Global interest rates have moved higher over the first three months of 2021 due to optimism over the rollout of the COVID-19 vaccine, better than expected economic data, the highest level of US government spending outside of war times, and the US Federal Reserves’ commitment to maintaining easy policy settings until higher inflation is sustainable.

Arguably interest rates have risen on a growth scare, rather than an inflation scare.

For the time being inflation is not a major issue and is probably not likely to be so for some time given “under-employment” (spare capacity) within the US, and global, economy.

Inflation in the US is expected to spike in the months ahead, this will reflect base effects from the shock to measures of inflation 12 months ago.

Albeit the risks to inflation are rising and higher inflation is likely to be an issue by the middle of the current decade, resulting in central banks raising interest rates.

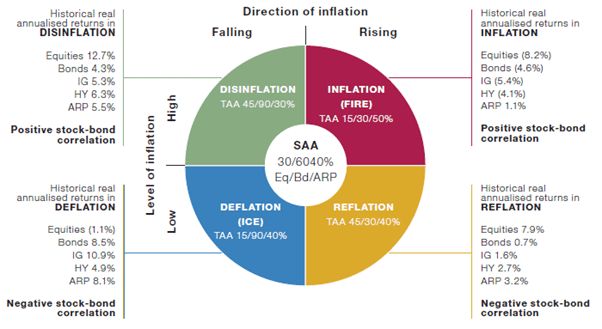

From a portfolio construction perspective, investors with a longer-term view should reduce portfolio duration and start considering the allocation to inflation linked bonds and real assets (such as property and infrastructure).

Either way, the outlook for fixed income is not encouraging in either the short or longer term, and particularly relative to returns experienced over the last 10-20 years.

In the US, the 10-year government bond yield recently reached its highest level since January 2020, trading at 1.77%, this compares to 0.62% a year ago and a low of 0.55% in August of 2020.

In New Zealand, the 10-year Government Bond yield finished March 2021 at 1.76%, the highest month end level since May 2019, and over 1% higher than the May 2020 low of 0.6%.

US 10-Year Government Bond Yield

Source: CNBC

Vaccine and Economic Data

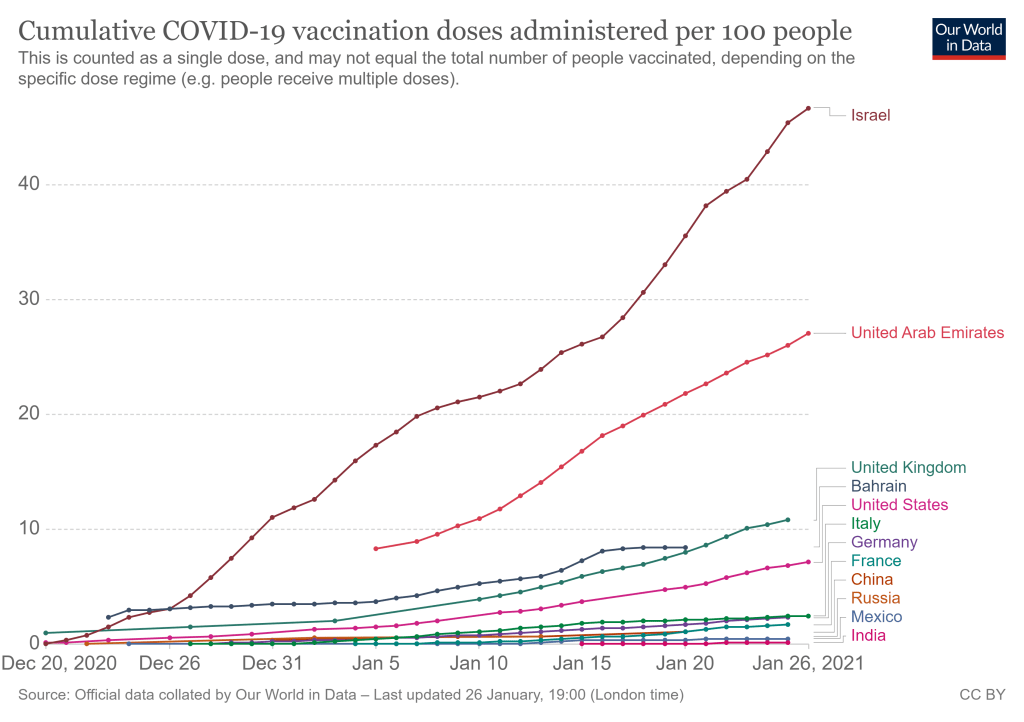

By the end of the first Quarter of 2021 61% of the population had received their first vaccine shot in Israel, this compares to 46% in the UK, 30% in the US and 12.6% across Europe.

The daily pace of new doses administered is approximately 1.5m in the European Union, 2.8m in the US, and 0.5m in the UK.

Economic data has surprised on the upside, particularly in the US where the reopening of the economy is accelerating economic activity:

The number employed in the US grew by 916k in March, well above consensus forecasts. The unemployment rate dropped to 6.0%, from 6.2%, with an increase in the participation rate restricting a larger decline in the unemployment rate.

US Consumer confidence also increased by a much larger amount in March than anticipated.

Expectations for US manufacturing activity increased by more than expected and reached the highest level since 1983.

A measure for US services sector activity also exceeded expectations.

Likewise, measures of economic activity in the Euro Zone and China have recorded stronger than expected numbers.

European measures of expected manufacturing activity are at all-time highs.

China’s industrial profits have grown by 179% from last year, reflecting the low base of 2020 but also the very strong increase in revenues and profits over the last 12 months.

While China is further advanced in its economic recovery, Europe lags both China and the US, nevertheless, the ongoing vaccine roll out and an increase in government spending should see the Euro Zone’s economy strengthen over the second half of 2021.

The US Federal Reserve (Fed), unsurprisingly, has upgraded their economic forecasts significantly reflecting the above factors, specifically larger than expected government spending and the improving public health situation.

The Fed also see inflation temporarily rising above 2% in the near term and then to settle to around 2% until 2023, they see the risks to inflation as balanced.

Market Performance

The above environment has been good for global equity markets, but not so good for global fixed income markets.

Base effects are also impacting Global Equity Market returns, as highlighted in the Table below.

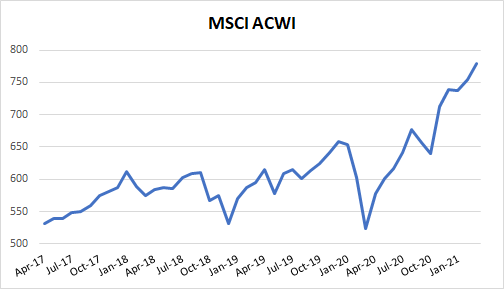

As can be seen, global equities have returned nearly 50% over the last year, in part reflecting markets reached their lows in March 2020 amidst the global COVID-19 pandemic.

MSCI ACWI

MSCI EM

12 Months

48.7%

53.0%

6 Months

18.6%

20.6%

3 Months

5.5%

4.0%

1 Month

3.3%

-0.9%

Source MSCI

The strength of the rebound since last year is very evident in the following graph.

Source: MSCI

Emerging markets have outperformed developed markets over the last year despite underperforming over the first quarter of 2021.

Over the first three months of 2021, European markets climbed 8.7%, the US 5.8%, Australia +4.3% and New Zealand fell 4.0%.

In the fixed income markets, the NZ Government Bond Index fell 3.2% for the March Quarter, Aussie fixed income declined 3.5%. Smaller declines were experience in global fixed income.

As a general trend, value continued to outperform momentum and the financial and energy sectors did well. The Real Estate and Utilities sectors tended to lag the broader market.

The US dollar has been stronger relative to most currencies recently, reflecting firmer US economic growth and rising bond yields.

Commodity prices have also been strong, the Dow Jones Commodity Index return 8.4% over the first three months of 2021.

The most recent Monthly Financial Markets Commentary and Performance is for March 2021.

David vs Goliath

GameStop dominated headlines over the last week of January and distracted market participants from key fundamentals.

In a sign of our times, encouraged via social media platform Reddit retail investors brought into GameStop, one of the most heavily shorted stocks in the market. This led to a “short-squeeze”. As the stock price of GameStop rose, rising by over 1,500% in January, short-sellers had to buy back the stock to cover their loses, pushing the stock price higher. Loses from the short-squeeze are estimated to have totaled $6 billion at one stage, mainly incurred by hedge funds.

A Goldman Sachs’ index of the most heavily shorted stocks rose close to 30% in January, ouch! This is the index’s best monthly return since 2008, a painful month for short sellers. See graph below.

The GameStop short-squeeze is considered one of the largest in US history and resulted in increased market volatility.

Another Goldman Index of the most popular hedge funds stocks fell by over 5% in a week as hedge funds sold stock positions to cover losses on their shorts, double ouch!!

The events surrounding GameStop are not expected to derail global equities markets, which are best characterised as at the early stages of a new bull market run. Pull backs and corrections can be expected along the way.

Economic Fundamentals

The GameStop event detracted from developments earlier in the month and improving fundamentals in relation to the fight against the Coronavirus.

The US Democratic party took control of the US Senate by the slimmest of margins after winning both seats in the Georgia run-off elections held in early January. They now control the Presidency, Senate, and House of Representatives.

President Biden released his $1.9 trillion (over 8% of the economy) Covid-19 Relief package, this is in addition to the $900 billion of spending approved by Congress in December. The plan includes $1,400 in additional direct payments to individuals (raising checks to $2000) and aid to small businesses.

Although there are political risks around getting the complete packaged passed, a significant percentage of the package is likely to be passed into law. This will represent a sizable stimulus for the US economy in the months ahead.

The extra spending along with ultra-low interest rates argues well for the global and US economy in 2021 and 2022.

Interest rates are likely to remain low for some time. Many Central Banks, for example the US Federal Reserve and Reserve Bank of Australia, are unlikely to raise interest rates until annual inflation has run above 2% for some time. This is not expected to occur until late 2024.

Over the later part of January, the daily rate of global coronavirus cases and hospitalisations began to decline, particularly in the US, Europe, and Japan.

At the same time the global vaccine rollout continues to gather pace, approximately 4.5 million vaccine doses are being administrated daily.

In total, more than 100 million vaccine doses had been administrated in 56 countries by early February 2021. Israel is leading with over 57% of their population vaccinated. America has vaccinated over 32 million people, 9.6% of their population. The UK has reached 14% of their population.

Goldman Sachs predict: The UK is expected to vaccinate 50% of its population in March, with the US and Canada following in April. The EU, Japan, and Australia reach this 50% threshold in May.

Once the vaccine rollout gathers speed the reopening of economies will accelerate around the world.

Economic data

Although global economic activity slowed over the last few months of 2020, due to rising covid-19 cases and associated lock down measures, the global economy is on track for a V-shaped recover. The US and China are leading the way. Europe is at risk of a double dip recession.

The consensus forecast for world economic growth in 2021 is just over 5%, and approximately 4.0% for 2022. The global economy shrank by around 4.0% in 2020.

For the first time in over 10 years, we are likely to see strong and synchronised global economic growth over the years ahead.

The Chinese economy rose 6.5% in the last quarter of 2020 from a year earlier. A strong outcome to finish the year and resulted in the Chinese economy growing 2.5% last year, the only major economy to report positive economic growth for 2020. Albeit this is the country’s weakest annual economic expansion since the late 1970s.

Based on first estimates the US economy grew 4.0% (annualised rate) over the 2020 December Quarter, which is below consensus forecasts and down on the 33.4% annualised rate in the third quarter of last year.

The Euro area economy contracted 0.7% over the final three months of 2020, this was a little bit better than expected.

Economic activity in New Zealand and Australia is exceeding expectations. Most notable was the surprise fall in New Zealand’s unemployment to 4.9%, levels not seen since 2017 and much lower than the 5.6% anticipated. The export and housing sectors drove employment growth.

Market Performance

Reflecting the volatility arising from the GameStop short-squeeze the US sharemarket fell 1.0% in January. In the US smaller sized companies continued to outperform.

International sharemarket benchmarks performed a little better than the US market. Markets across Asia performing well, particularly China (+4.8%). Latin American markets underperformed.

Overall, Emerging Markets continued to outperform Developed Markets, EM markets returning over 3.0% in January.

The Australian and New Zealand sharemarkets eked out positive returns, +0.3% and 0.1% respectively.

Commodities performed well, +4.8%, oil outperformed in January (+7.5%) and the price of Gold fell (-2.5%).

By and large fixed income underperformed in January, particularly longer dated securities as interest rates drifted higher. In New Zealand, the Government Bond Index fell 0.3% and Australia’s -0.7%.

Regulatory approval of Covid-19 vaccine and commencement of global immunisation program

Democrat Party’s eventual control of Presidency, Senate, and House of Representatives will provide further support to the US economy from an increase in government spending

US Federal Reserve’s decision to adopt a more flexible “average inflation targeting” policy

In recent months there has been a tug of war between rising Covid-19 infections and the development, approval, and initial distribution of a Covid-19 vaccine.

Increasingly the roll out of the vaccine will win this battle, helped by increased spending in the US and ultra-low interest rates around the world. This is supportive of global economic activity and sharemarkets in 2021.

Key Risks

The Covid-19 vaccines are less effective than anticipated, particularly given existence of different strains

The US Federal Reserve change their policy settings earlier than expected

US consumers are cautious preferring to save rather than spend more of their $2,000 government handout

There is the risk that global economic activity surprises on the upside in 2021

Portfolio Considerations

Prefer equities over fixed income on a 12 – 18 months time horizon

Shorten duration exposures of portfolios

Emerging markets, cyclicals, and value to outperform

Any sharemarket pull-back should be seen as an opportunity to add too equities

Start preparing portfolios for a period of higher inflation

Effective and efficient implementation of investment strategies key.

Vaccine Roll Out

A successful vaccine has been developed in record time, less than one year. The previous record for the fastest time to develop a vaccine occurred in the late 1960s when it took four years to develop a vaccine for the mumps.

More than 68 million vaccine doses had been administrated in 56 countries by late January 2021. The daily rate is approximately 3.4 million doses a day. Israel is leading with 43% of their population vaccinated. America has given out 23.5 million doses, 7.1% of their population.

A World Health Organisation linked plan is in place to administer 2 billion vaccine doses globally in the first half of 2021. Expectations are for large portions of the population to be vaccinated by the middle of 2021.

Goldman Sachs forecast: The UK is expected to vaccinate 50% of its population by the end of March, with the US and Canada following in April. The EU, Japan, and Australia reach the 50% threshold in May.

These targets are likely given the expected ramping up of vaccine production over the months ahead and despite a slower start to the vaccine roll out than expected in some countries.

Albeit virus cases and deaths have reached new records and new variants of the virus have emerged in the UK, Ireland, and South Africa. This wave of infections across the world, particularly in Europe and the UK, has resulted in renewed lockdowns and ongoing restrictions on activities.

As a result, global economic activity is expected to be weaker over the last quarter of 2020, after a strong rebound in the third quarter of last year. This weakness is expected to flow over into the New Year, 2021, given the above and that it has been a harsh northern winter. This is reflected in recent economic data. For example, the US economy expanded at a 4% annualised rate in the fourth quarter of 2020, which was below expectations and down from the record 33.4% annualised rate in the previous three months.

However, once the vaccine rollout gathers speed the reopening of economies will accelerate around the world.

Democrats win Georgia Senate elections

The outlook for 2021 is positive and received a boost following the Democrats taking control of the US Senate by the slimmest of margins after winning both seats in the Georgia run-off elections held in early January.

President Biden has released his $1.9 trillion (over 8% of the economy) Covid-19 Relief package, this is in addition to the $900 billion of spending approved by Congress in December. The plan includes $1,400 in additional direct payments to individuals (raising cheques to $2000) and aid to small businesses.

The relief package aims to provide economic support until the threat of the pandemic has receded.

There are political risks around getting the complete packaged passed in to law. Albeit, a sizeable percentage of the package is likely to be passed into law, which will represent a sizable stimulus for the US economy.

The extra spending along with ultra-low interest rates argues well for the global and US economy.

Interest rates are likely to remain low for some time.

US Federal Reserve Policy Position

The US Federal Reserve (Fed) will now seek to achieve average inflation of 2% over time. Instead of targeting a 2% inflation rate, the Fed will allow higher inflation “for some time” to offset below 2% periods of inflation.

They will also target “broad and inclusive employment”, where employment is placed ahead of inflation in terms of policy priority.

This is a dramatic change in policy and has implications for financial markets now and in the future.

The key short-term impact, interest rates in the US are expected to remain lower for longer. Specifically, the Fed will likely keep the Feds Fund Rate at the currently level of 0.25% until after there has been a period of inflation above 2%. And this is not likely to happen until late 2024 – early 2025.

Longer-term, the risks to containing inflation have increased. Likewise, longer-term interest rates will likely drift upward in anticipation of higher inflation and as the Fed scales back on other areas of their Policy response, such as the buying of fixed income securities (tapering of Quantitative Easing Policy).

With regards to US inflation, core consumer prices have risen 1.6% over the last year in the USA.

Although inflation is expected to be well contained over the next few years, the risks of higher inflation in the future are mounting, particularly given the size of the government spending being undertaken in the US.

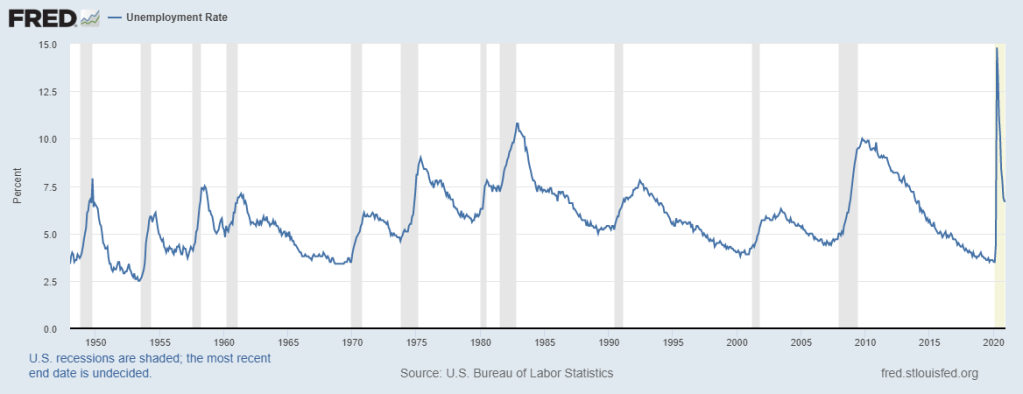

Although there might be some volatility in the inflation rate over 2021, reflecting the extreme disruption to the economy last year, core inflation is set to remain low given the level of spare capacity within the economy. By way of example, as presented in the graph below, US unemployment remains high despite a breathtaking recovery over the second half of 2020. The US unemployment rate is currently 6.7%. This compares to 14.8% at the end of April 2020 and 3.5% at the beginning of the year.

Nevertheless, the global economic environment is transforming to a more reflationary phase. This compares to the deflationary environment that has dominated the global economy since 2008 and the Global Financial Crisis (GFC).

As outlined in this Kiwi Investor Blog Post, investors are well advised to consider preparing their portfolios for the potential of a higher inflation environment.

Economic Outlook

The global economy is poised to rebound strongly in 2021, primarily driven by the factors outlined above, vaccine roll out, ultra-low interest rates, and government spending measures.

For the first time in over 10 years, we are likely to see strong and synchronised global economic growth over the years ahead.

The consensus forecast for world economic growth in 2021 is just over 5%, and approximately 4.0% in 2022. The global economy shrank 4.2% in 2020.

The V shape economic recovery is well on track around the world.

Given the Democrats win in Georgia as outlined above, economic growth forecasts for the US have been revised upwards recently on an expected increase in government spending. Consensus forecasts are for just over 4.0% growth in 2021, after a decline of 3.5% in 2020.

Many areas of the US economy are expected to perform well in 2021, including consumer spending, a rebound in capital expenditures, a strong housing market, and inventory rebuilding. Given above potential economic growth this year the level of unemployment should decline, reducing the slack in the US labour market.

The US economy has remained resilient in the face of the pandemic, with businesses learning to adapt to restrictions on activities. There is little evidence of economic scaring that would have negative longer-term impacts on economic activity.

This argues well for the US and risks to economic activity in 2021 could well be to the upside.

The Chinese economy rose 6.5% in the last quarter of 2020 from a year earlier. A strong outcome to finish the year and resulted in the Chinese economy growing 2.5% last year, the only major economy to report positive economic growth for 2020. Albeit this is the country’s weakest annual economic expansion since the late 1970s.

China is more advanced in its economic cycle post Covid relative to the rest of the world. The rebound in the economy is being driven by industrial production, exports, retail sales, and investment into fixed assets. Like the rest of the world, economic activity remains weak in tourist related industries, such as hotels and catering.

Around the rest of the world the Eurozone is expected to grow around 4.6% in 2021 after the sharp -7% contraction in 2020. The UK economy, which suffered one of the sharpest declines in 2020, estimated to have contracted by -11.2%, is on track to rebound in 2021 with over 5% GDP growth. The Japanese economy is expected to grow by around 2.5% in 2021.

The New Zealand economy expanded a stronger than expected 14% in the third quarter of 2020. This follows a historical 11% contraction in the second quarter. The economy is 2.2% smaller compared to a year ago. Construction and retail trade led the recovery following the second quarter lockdown. Accordingly, there has been an improvement in business confidence.

Inflation in the final quarter of 2020 was 0.5%, which was stronger than expected. Annual inflation was unchanged at 1.4%. The quarterly result in part reflects strong demand in some areas (e.g. accommodation and air travel) due to pent up demand following lockdown, supply issues in other sectors, and rising prices for housing construction.

Some volatility in inflation data can be expected in the quarters ahead, and Central Banks, such as the Reserve Bank of New Zealand, will look through this volatility.

In relation to New Zealand, a strong rise in house prices over the last three months of 2020 has reduced the likelihood of negative cash rates.

This turn of events has witnessed a steady appreciation of the New Zealand dollar (Kiwi) over the last quarter. The Kiwi is currently trading at around 72 cents versus the US dollar, compared to 67 cents at the end of September (+6%), and is 18% higher compared to 60 cents at the end of April 2020.

Brief Market and Portfolio Positioning Comments

Global equities climbed over 17% in the December 2020 Quarter, to finish the year 16.9% higher than at the end of 2019.

The US sharemarket ended the year at historical highs. The S&P500 returned 18.4% in 2020 and is over 70.0% higher from its yearly lows in late March.

The New Zealand sharemarket also finished the year strongly, rising 16.3% in the last quarter of the year, returning 14.7% in 2020. This is the Index’s ninth consecutive year of positive returns. The benchmark has more than quadrupled since the end of 2011, and more than doubled since 2015 (benchmark returns are based on S&P Dow Jones Index data).

The Australian sharemarket returned 13.7% over the last three months of 2020, eking out 1.4% for the year.

Information Technology and Consumer Discretionary tended to be the better performing sections, Energy and Real Estate sectors the worst.

Growth factor outperformed Value by a wide margin in 2020, as is has for some time. In the US, growth returned 33.5% and value 1.4% for the 12 months period.

Nevertheless, this hides a sharp reversal in market fortunes over the last quarter of 2020, in the US value returned 14.5% and growth 10.7%, enhanced value returned 24.6% for the period.

This reversal in market leadership has some legs and likely has further to run, given the economic backdrop outlined above.

Likewise, cyclicals and the energy sectors will benefit from stronger global growth and the releasing of pent-up demand as economies open-up following the roll out of the vaccine.

After 10-years of underperforming Development Markets, Emerging Markets are better placed to benefit from an increase in global manufacturing. These markets recently reached historical highs; surpassing levels last seen in 2007.

Within portfolios duration should be reduced.

The ultra-low interest rate environment presents challenges for investors in the years ahead. Over reliance on cash, fixed income, and equities to generate portfolio returns could lead to disappointing outcomes. Investors should look to increasingly diversify outside of the traditional asset class. This Post by Kiwi Investor Blog provides access to discussions on different portfolio investment strategies than could be considered in meeting the challenges ahead.

Global sharemarkets have performed strongly in recent months and are susceptible to a pull back.

Given the economic backdrop outlined above, this would provide an opportunity to consider adding to equity positions.

The latest monthly commentary, for March 2021, can be found here.

Cautious Optimism

Caution optimism prevailed across markets and economies as the global annus horribilis ended. Wishing you all an annus mirabilis for 2021 (a wonderful year).

Global markets finished the year buoyed by the commencement of the Covid-19 vaccines roll out, ultra-low interest rates, and finally a new US government spending package.

Global equities climbed 4.9% in December and are 16.9% higher than at the end of 2019. Who would have thought that was possible after the near 30% declines earlier in the year?

The US sharemarket ended the year at historical highs. The S&P500 returned 18.4% in 2020 and is almost 70.0% higher from its yearly lows in late March.

The New Zealand sharemarket also finished the year strongly, rising 5.5% in December, returning 14.7% in 2020. This is the Index’s ninth consecutive year of positive returns. The benchmark has more than quadrupled since the end of 2011, and more than doubled since 2015! (benchmark returns are based on S&P Dow Jones Index data).

The Australian sharemarket returned 1.2% in December, eking out 1.4% for the year. The Information Technology sector posted a 9.5% gain in December and 57.8% for the twelve months period. The energy sector lost 27.6% for the year, and utilities fell 16.7% over the same period. These sector relative performance outcomes have been experienced internationally, along with the momentum and growth factors outperforming value over the last twelve months. Although growth and momentum outperformed value in December they have trailed value over the last three months of 2020. In Australia, value returned 18.1% over the last quarter of 2020, momentum and growth returned 7.8% and 10.1% respectively.

The V shape economic recovery is well on track around the world. The New Zealand economy expanded a stronger than expected 14% in the third quarter of 2020. This follows a historical 11% contraction in the second quarter. The economy is 2.2% smaller compared to a year ago. Construction and retail trade led the recovery following the second quarter lockdown. As the Kiwi Bank economics team highlighted, 95% of New Zealand’s economy is doing well, but the other 5%, primarily the tourism and education sectors, are not, and we should spare a thought for them. The peak over the Kiwi summer period, December – March, will be a test for them.

As mentioned above, the USA has instigated additional government spending to combat COVID-19. The relief package is worth around $900 billion, 4% of the economy. It was larger than many expected and includes $600 personal payments to most Americans, along with additional unemployment benefits, and further support for businesses. This package should help to support US economic activity over the first quarter of 2021.

Japan also announced additional economic stimulus measures in early December, this includes around 30 trillion Yen in additional spending to prevent the spread of COVID-19, transform the economy post the pandemic, and enhance infrastructure. The Japanese economy grew 5.3% in the July – September period, after declining 8.3% in the second quarter.

Chinese industrial profits have grown 15% over the last year and exports are booming. Over the twelve months ending November Chinese exports have grown 21%, the highest level of annual growth in almost 10 years.

European manufacturing activity has been stronger than expected, suggesting fourth quarter economic activity is going to be higher than anticipated.

Likewise, US manufacturing has been resilient at a time of rising COVID-19 cases.

In Australia, Consumer sentiment has reached its highest level in 10 years.

The UK and Europe have agreed on a post-Brexit Free Trade Agreement that will result in zero tariffs and quotas on goods that comply with rules of origin. Terms on trade in services have also been reached, which are flexible reflecting the closeness of business activities.

The Year ahead

Although economic activity is expected to moderate in the fourth quarter of 2020, given rising COVID-19 cases, complicated by the northern hemisphere winter, consensus expectations are for just over 5% global economic growth in 2021, led higher by Europe, UK, China, and India.

After a sluggish start to the year the global economy should accelerate due to the rollout of the vaccines, and mass immunisation reduces the virus threat, the continued accommodative central bank policy settings of ultra-low interest rates, and government spending packages.

More than 12 million vaccine doses have been administrated in 30 countries so far. Israel is leading with 10.5% of their population vaccinated. America has given out 4.3 million doses, 1.3% of their population. A World Health Organisation linked plan is in place to administer 2 billion vaccine doses globally in the first half of 2021.

The US Federal Reserve’s (Fed) adoption of a flexible average inflation targeting will see global interest rates remain low for some time. The Fed is not expected to raise interest rates until 2025.

In this environment, global equities are more than likely to outperform in the year ahead, global bond yields rise moderately, and the US dollar weakens further. Emerging markets are well placed in this environment, the value factor will benefit from greater economic certainty in 2021, and commodities such as oil may also find greater support.

In America, Georgia Senate run-off elections in mid-January provide a short-term focal point for markets. The result will determine control of the US Senate. A switch to a Democratic party-controlled Senate will likely see changes to US tax policies in the months ahead.

Inflation, although anticipated not to be an issue over the next few years, will become more of a threat in later years.

The latest monthly commentary, for January 2021, can be found here.

Vaccine Recovery

Risk assets (e.g. equities and commodities) performed strongly in November following encouraging Covid-19 vaccine trial results from Pfizer-BioNTech, AstraZeneca, and Moderna.

Global equities returned 13.3% in November, many markets had one of their best monthly returns in several years. Some markets reached historical highs, including New Zealand and the US. European markets outperformed, Spain and Italy returned 28.3% and 26.3% respectively.

US Food and Drug Administration (FDA) approval of a Covid-19 vaccine could be as early as 10th December 2020. Europe is likely to approve a vaccine(s) by the end of the year.

A great way to finish a very challenging year.

Expectations are for widespread vaccinations in the US by April 2021, high-risk individuals will receive the vaccine earlier, as early as mid-December 2020.

Likewise, it is anticipated large proportions of the population in the UK, European Union, Japan, and Australia will be vaccinated by May 2021. It is estimated New Zealand will get their first doses of the vaccine in March 2021.

In addition to the widespread public health benefits, global economic activity is expected to pick up in the second quarter of 2021, underpinning the V(accine)-Shaped Recovery, as expressed by Goldman Sachs. They forecast 5% growth in the US over 2021, and 6% for the global economy.

In the interim, global economic activity is expected to weaken over the last quarter of 2020 and into the first quarter of 2021 due to the rise in Covid-19 cases over the last couple of months in Europe and the US, and as the northern hemisphere heads into the winter months (a high risk period).

There has been a softening of European high-frequency data recently, such as truck milage data in Germany, UK retail sales, and cinemas and restaurants have witnessed declining revenues due to the tightening of lockdown measures. Although less severe than actions undertaken in Europe, State and Local restrictions have increased in the USA.

The outcome of the US elections buoyed markets at the beginning of the month. Although Biden has been elected the 46th President of the United States of America, congress will likely remain divided. A divided government means regulatory risks have decline, taxes are likely to remain lower, some pro-business policies will remain in place, and government spending to be less relative to the Blue wave outcome. A $1 trillion dollar US Government stimulus package is now expected, less than half of what was previously anticipated.

Recent US earnings have also surprised on the upside, supporting markets, as US companies managed to maintain profit margins better than expected despite the large hit to revenues.

November was characterised by a “pro-cyclical” trade, where those stocks that have lagged the market for some time and will benefit more from an opening of economies outperformed. From a sector perspective Energy, Financials, and Consumer Discretionary performed well. The “Covid” trade sectors, Consumer Staples, Healthcare, and Utilities lagged the broader market. Likewise, value and high beta stocks outperformed, low volatility, momentum, and growth underperformed – this will be reflected in relative manager performance in November.

In other asset classes, commodities returned 8.6% in November, crude oil was up 25.7%, surpassing pre-covid-19 highs, and gold fell -5.6%.

Fixed income performed well, particularly corporate credit and high yield, both returning over 3% in the US.

Emerging markets equities underperformed developed markets, returning 8.9%. (above returns based on S&P Index data.)

The US dollar continued to weaken over the month. This saw the New Zealand dollar (Kiwi) trade at a two and half year high versus the Greenback, rising from 66.25 cents to 70.41 cents (+6.3%).

The strength in the Kiwi partly reflects a scaling back of expectations the Reserve Bank of New Zealand (RBNZ) will move the Official Cash Rate (OCR) into negative territory, given rising house prices e.g. house prices in New Zealand’s largest city, Auckland, have risen 10.8% since June averages based on sales by New Zealand’s biggest real estate business, Barfoot and Thompson.

Key risks include ongoing uncertainty over transition of power in the US, global economic activity slows more than expected due to recent rise in covid-19 cases, US government stimulus package disappoints, and vaccine roll out is slower than anticipated.

Albeit the medium-term outlook for equities is well supported by an eventual roll out of a vaccine and ultra-low interest rates. Low interest rates are expected to remain in place for some time, the US Federal Reserve is not expected to raise interest rates until 2025.

Equities remain attractive relative to bonds. Although longer-term interest rates are likely to drift higher over the next few years, a significant move higher is unlikely given an absence of inflation. Therefore, higher interest rates are not expected to be a threat to global equity markets for some time.

Markets appear to have moved on from the US election result, reflected in the 7.3% gain in the US S&P 500 index last week (its best week since April).

The US sharemarket declined 2.7% over October. Global equities fell 2.4% and Oil 11.0% on rising COVID-19 cases internationally and US election uncertainty. Europe led markets lower, falling -5.6%. Emerging markets rose 2.1%, driven higher by Chinese stocks.

The “Blue wave” failed to materialise. Although Biden won the US Presidency and the Democrats retained their majority in the House, control of the Senate will be decided in runoff elections in Georgia in January. It was not the resounding win predicted by the “Polls”.

With a divided government, regulatory risks decline for some sectors, and government spending is likely to be less robust relative to a Blue wave outcome. A $1 trillion dollar US Government stimulus package is now expected, less than half of what was previously anticipated.

Global interest rates are expected to remain lower for longer given the US election outcome.

The result is also slightly positive for emerging markets due to lower interest rates for longer and an expected friendlier global trade environment under a Biden Presidency.

October witnessed a rise in COVID-19 cases across Europe and in the US, resulting in fresh lockdown announcements in Europe and the UK.

In view of the above outcomes, economists are trimming their economic growth forecasts for the US and Europe. Albeit the “V” shaped global economic recovery remains on track.

In more positive economic news, the US Labour market is rebounding more quickly than anticipated, largely due to a rehiring of temporarily laid off workers. Measures of global manufacturing activity have also improved more than forecasted.

The US economy grew at a 33% annualised rate in the third quarter of 2020 but remains 2.9% lower compared to a year ago. In the US retail sales, manufacturing, CAPEX, and the housing market underpin the bounce back in economic activity.

The Chinese economy continues to recover, economic activity is 4.9% higher compared to a year ago, driven by industrial production, rising retail sales, and strengthening exports.

The Red Wave

In a red wave New Zealand’s Labour Party (which is more aligned with the US Democratic Party) claimed a decisive victory in the General Election.

Like the rest of world, New Zealand is expected to see a sharp rebound in economic activity over the second quarter (the economic growth data is not available yet). Consistent with this, Business confidence has rebounded sharply to be above pre-pandemic levels, according to the NZIER Survey of Business Opinions.

New Zealand’s unemployment rate rose by 1.3% to 5.3% in the third quarter’s Employment Report. Workers covered under the Government’s wage subsidy programme are counted as employed in the official data. Accordingly, the unemployment rate is expected to rise further.

The New Zealand Sharemarket continues to perform strongly in absolute terms and relative to the rest of the world. The strong performance of F&P Healthcare and the electricity generating sector helped push the market 2.9% higher over the month.

The Australian sharemarket also outperformed, returning 1.9%, on an improving economy and expectations the Reserve Bank of Australia (RBA) would reduce interest rates further, which they delivered in early November by reducing the cash rate to 0.1% from 0.25%.

Australia and New Zealand remain relatively well placed for 2021 as the global economy transitions into a recovery phase.

Australia is expected to benefit from a pickup in global economic activity, particularly if a vaccine becomes available.

A COVID-19 vaccine is anticipated to become available by January 2021. If so, global economic growth is expected to pick up strongly over the second quarter of 2021.

Global equities are likely to perform strongly in this scenario.