One of the key questions facing investors at the moment is whether inflation or deflation represents the bigger risk in the coming years.

Now more than ever, given the likely economic environment in the years ahead, investors need to consider all their options when building a portfolio for their future. This may mean a number of things, including: increasing diversification, investing in new or different markets, being active, and flexible to take advantage of unique opportunities as they arise.

Those portfolios overly reliant on traditional markets, such as equities and fixed income in particular, run the risk of failing to meet to their investment objectives over the next ten years.

Conundrum Facing Investors

A recent article by Alan Dunne, Managing Director, Abbey Capital, The Inflation-Deflation debate and its Implications for Asset Allocation, which recently appeared in AllAboutAlpha.com, clearly outlines the conundrum currently facing investors.

As the article highlights, one of the “key questions facing investors at the moment is whether inflation or deflation represents the bigger risk for the coming years. Economists are split on this….”

Following a detailed analysis of the current and likely future economic environment and potential influences on inflation or deflation (which is well worth reading) the article covers the Implications for Asset Allocations.

Inflation or Deflation: Implications for Asset Allocations

The article makes the following observations as far as asset class performance in different inflation environments, based on historical observations:

- Deflation like in the 1930s, is negative for equities but positive for Bonds.

- If inflation picks ups, or even stagflation, that would be negative for real returns on financial assets and real assets may be favoured.

They conclude: “the current uncertainty highlights the importance of holding diversified portfolios, with exposure to a range of traditional and alternative assets and strategies with the potential to deliver returns in different market environments.”

Current Environment

Abbey Capital anticipate greater co-ordination of policy between governments (fiscal policy) and central banks (monetary policy).

As they note, “many economists draw a parallel between the current scenario and the substantial increase in government debt during World War II. One of the consequences of higher debt levels is that we may see pressure on central banks to maintain interest rates at low levels and maintain asset purchases to ensure higher bond issuance is not disruptive for bond markets i.e. coordination of monetary and fiscal policies.”

I think this will be the case. The Bank of Japan has maintained a direct yield curve control policy for some time and the Reserve Bank of Australia has implemented a similar policy recently. Direct yield curve control is where the central bank will target an interest rate level for the likes of the 3-year government bond.

In the environment after World War II debt levels were brought back to more manageable levels by keeping interest rates low (a process known as financial repression).

From a government policy perspective, financial repression reduces the real value of debt over time. It is the most palatable of a number of options.

Financial repression is potentially negative for government bonds

With interest rates so low, and likely to remain low for some time given policies of financial repression the real return (after inflation) on many fixed income instruments and cash could be negative.

A higher level of inflation not only reduces the real return on bonds but potentially also reduces the diversification benefits of holding bonds in a portfolio with equities.

The diversification benefits of bonds in the traditional 60 / 40 equity-bond portfolio (Balanced Portfolio) has been a strong tail wind over the last 20 years.

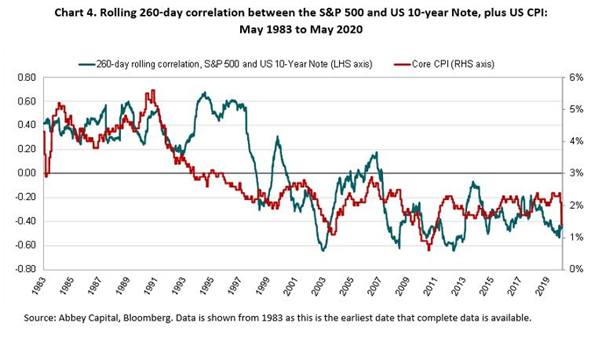

The more recent low correlation between bonds and equities is evident in the Chart below, which was presented in the article.

The Chart also highlights that the relation of low correlation between equities and bonds, which benefits a Balanced Portfolio, has not always been present.

As can be seen in the Chart, in the 1980s, when inflation was a greater concern, inflation surprises were negative for both bonds and equities, they became positively correlated.

What should investors do?

“Investors are therefore left with the challenge of finding alternatives for government bonds, ideally with a low or negative correlation to equities and protection against possible inflation.”

The article runs through some possible investment solutions and approaches to meet the likely challenges ahead. I have outlined some of them below.

I think duration (interest rate risk) and credit can still play a role within a broad and truly diversified portfolio. Within credit this would likely involve expanding the universe to include the likes of high yield, securitised loans, private debt, inflation protections securities, and emerging market debt as examples.

The key and most important point is that a robust portfolio will be less reliant on tradition asset classes, traditional asset class betas, to drive investment return outcomes. This is likely to be vitally important in the years ahead.

Accordingly, investors will need to be more active, opportunistic, and maintain very broad and truly diversified portfolios. Not only within asset classes, such as the fixed income example provided above, but across the portfolio to include the likes of real assets and liquid alternatives.

Real assets

Abbey Capital comment that “Real assets such as property and infrastructure should provide protection against higher inflation for long-term investors but may not be attractive for investors valuing liquidity.”

Although the maintenance of portfolio liquidity is important, Real assets can play an important role within a robust portfolio.

For the different types of real assets, their investment characteristics, and likely performance and sensitivity to different economic environments, including economic growth, inflation, inflation protection, stagflation, and stagnation please see the Kiwi Investor Blog Post, Real Assets Offer Real Diversification. The extensive analysis has been undertake by PGIM.

Liquid Alternatives

Abbey Capital provide a brief discussion on liquid alternatives with a focus on managed futures. Not surprisingly given their pedigree.

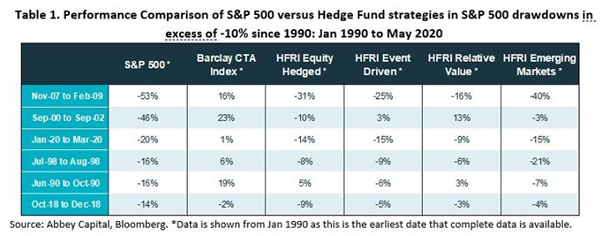

They provide the following Table which highlights the benefit of liquid alternatives and hedge funds at time of significant sharemarket declines (drawdowns).

Concluding Remarks

Being a managed futures manager, it is natural to be cautious of Abbey Capitals concluding remarks, being reminded of the Warren Buffet quote, “Never ask a barber if you need a haircut.”

Nevertheless, the Abbey Capital’s economic analysis and investment recommendations are consistent with a growing chorus, all singing from a similar song sheet. (Perhaps we could call this a “Barbers Quartet”!)

Without having an axe to grind, and in all seriousness, I have covered similar analysis and comments in previous Posts, the conclusions of which have a high degree of validity and should be considered, if not a purely from portfolio risk management perspective so as to understand any gaps in current portfolios for a number of likely economic environments.

The key and most important point is that robust portfolios will be less reliant on traditional asset classes, traditional asset class betas, to drive investment return outcomes.

Accordingly, investors will need to be more active, opportunistic, and maintain very broad and truly diversified portfolios

Therefore, it is hard to disagree with one of the concluding remarks by Abbey Capital “To account for the competing requirements in a portfolio of returns, low correlation to equities, liquidity and possible inflation protection, investors may need to build robust portfolios with a broader mix of assets and strategies.”

Other Reading

For those interested, previous Kiwi Investor Blog posts of relevance to the Abbey Capital article include:

Preparing your Portfolio for a period of Higher Inflation, this is the Post of most relevance to the current Post, and covers a recent Man article which undertook an analysis of the current economic environment and historical episodes of inflation and deflation.

Man conclude that although inflation is not an immediate threat, the likelihood of a period of higher inflation is likely in the future, and the time to prepare for this is now. Man recommends several investment strategies they think will outperform in a higher inflation environment.

Protecting your portfolio from different market environments – including tail risk hedging debate, compares the contrasting approaches of broad portfolio diversification and tail risk hedging to manage through difficult market environments.

It also includes analysis by PIMCO, where it is suggested to “diversify your diversifiers”.

Lastly, Sharemarket crashes – what works best in minimising losses, market timing or diversification, covers a research article by AQR, which concludes the best way to manage periods of severe sharemarket decline is to have a diversified portfolio, it is impossible to time these episodes. AQR evaluates the effectiveness of diversifying investments during sharemarket drawdowns using nearly 100 years of market data.

Happy investing.

Please see my Disclosure Statement

Pingback: Kiwi Investor Blog has published 150 Posts….. so far | Kiwi Investor Blog

Pingback: Monthly Financial Markets Commentary and Performance– December 2020 | Kiwi Investor Blog