The current return assumption for the average US public pension fund is 7.25%, according to the National Association of State Retirement Administrators (NASRA), highlighted in a recent CFA Institute Blog: Global Pension Funds the Coming Storm.

This compares to the CFA Institute’s (CFA) article expected return for a Balanced Portfolio of 3.1% over the next 10 years. A Balanced Portfolio is defined as 60% Equities and 40% Fixed Income.

Therefore, the article concludes that a 7.25% return assumption is “overly optimistic in a low return interest rate environment”.

The expected low return environment will place increasing pressure on growing pension liabilities and funding deficits. This is over and above the pressures of an aging population and the shift toward Defined Contribution (DC) superannuation schemes e.g. KiwiSaver.

This environment will likely require a different approach to the traditional portfolio in meeting the growing liabilities of Define Benefit (DB) Plans and in meeting investment return objectives for DC superannuation Funds such as KiwiSaver in New Zealand.

The value will be in identifying and implementing the appropriate underlying investment strategies.

Past Returns

For comparison purposes an International Balanced Portfolio, as defined above, has returned around 7.8% over the last 10 years, based on international fixed income and global sharemarket indices.

A New Zealand Balanced Portfolio has returned 10.3%, based on NZ capital market indices only.

New Zealand has had one of the best performing sharemarkets in the world over the last 10 years, returning 13.5% per annum (p.a.), this compares to the US +11.3% p.a. and China -0.7% p.a.. Collectively, global sharemarkets returned 10.2% p.a. in the 2010s.

Similarly, the NZ fixed income markets, Government Bonds, returned 5.4% p.a. last decade. The NZ 5-year Government Bond fell 4.1% over the 10-year period, boosting the returns from fixed income. Interestingly, the US 5-year Bond is only 1% lower compared to what it was at the beginning of 2010.

It is worth noting that the US economy has not experienced a recession for over ten years and the last decade was the only decade in which the US sharemarket has not experienced a 20% or more decline. How good the last decade has been for the US sharemarket was covered in a previous Post.

In New Zealand, as with the rest of the world, a Balanced Portfolio has served investors well over the last ten or more years. This reflects the strong returns from both components of the portfolio, but more particularly, the fixed income component has benefited from the continue decline in interest rates over the last 30 years to historically low levels (5000 year lows on some measures!).

Future Return Expectations

Future returns from fixed income are unlikely to be as strong as experienced over the last decade. New Zealand interest rates are unlikely to fall another 4% over the next 10-years!

Likewise, returns from equities may struggle to deliver the same level of returns as generated over the last 10-years. Particularly the US and New Zealand, which on several measures look expensive. As a result, lower expected returns should be expected.

The lower expected return environment is highlighted in the CFA article, they provide market forecasts and consensus return expectations for a number of asset classes.

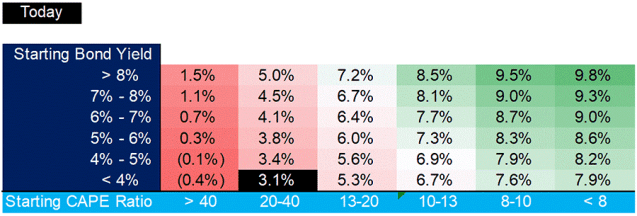

As the article rightly points out, one of the best estimates of future returns from fixed income is the current interest rate.

As the graph below from the article highlights, “the starting bond yield largely determines the nominal total return over the next decade. So what you see is what you get.”

US Bond Returns vs. US Starting Bond Yields

In fact, this relation has a score of 97% out of 100%, it is a pretty good predictor.

The current NZ 10 Government Bond yield is ~1.65%, the US 10-Year ~1.90%.

Predicting returns from equity markets is more difficult and comes with far less predictability.

Albeit, the article concludes “low returns for US equities over the next 10 years.”

Expected Returns from a Balanced Portfolio

The CFA Article determines the future returns from a Balance Portfolio “By combining the expected returns from equities and bonds based on historical data, we can create a return matrix for a traditional 60/40 portfolio. Our model anticipates an annualized return of 3.1% for the next 10 years. That is well below the 7.25% assumed rate of return and is awful news for US public pension funds.”

Subsequent 10-Year Annualized Return for Traditional 60/40 Equity/Bond Portfolio

This is a sobering outlook as we head into the new decade.

Over the last decade portfolio returns have primarily been driven by traditional market returns, equity and fixed income “beta“. This may not be the case when we look back in ten-years’ time.

This is a time to be cautious. Portfolio strategy will be important, nevertheless, implementation of the underlying strategies and manager selection will be vitally important, more so than the last decade. The management of portfolio costs will also be an essential consideration.

It is certainly not a set and forget environment. The challenging of current convention will likely not go unrewarded.

Forewarned is forearmed.

Global Pension Crisis

The Global Pension crisis is well documented. It has been described as a Financial Climate Crisis, the risks are increasingly with you, the individual, as I covered in a previous Post.

As the CFA article notes, the expected low return environment adds to this crisis, as a result deeper cuts to government pensions and greater increases in the retirement age are likely. This will led to greater in-equality.

This is a serious issue for society, luckily there is the investment knowledge available now to help increase the probability of attaining a desired standard of living in retirement.

However, it does require a shift in paradigm and a fresh approach to planning for retirement, but not a radical departure from current thinking and practices.

For those interested, I cover this topic in more depth in my post: Designing a New Retirement System. This post has been the most read Kiwi Investor Blog post. It covers a retirement system framework as proposed by Nobel Laureate Professor Robert Merton in his 2012 article: Funding Retirement: Next Generation Design.

Lastly, the above analysis is consistent with recent calls for the Death of the Balanced Portfolio, which I have also Blogged on.

Nevertheless, I think the Balanced Portfolio is being replaced due to the evolution within the wealth management industry globally, which I covered in a previous Post: Evolution within Wealth Management, the death of the Policy Portfolio. This covers the work by the EDHEC-Risk Institute on Goals-Based Investing.

In another Posts I have covered consensus expected returns, which are in line with those outlined in the CFA article and a low expected return environment.

In my Post, Investing in a Challenging Investment Environment, suggested changes to current investment approaches are covered.

Finally, Global Economic and Market outlook provides a shorter-to-medium term outlook for those interested.

Please note, I do not receive any payment or financial benefit from Kiwi Investor Blog, and a link to my Discloser Statement is provided below.

Happy investing.

Please read my Disclosure Statement