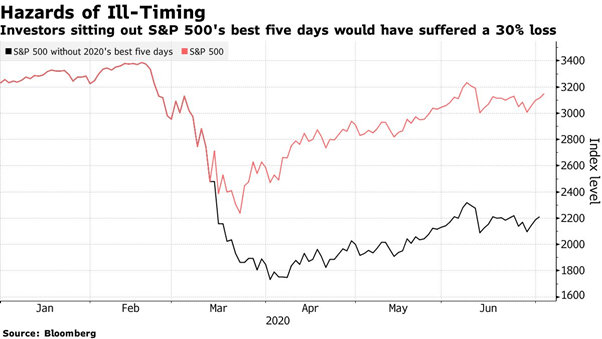

Missing the sharemarket’s five best days in 2020 would have led to a 30% loss compared to doing nothing.

The 2020 covid-19 sharemarket crash provides a timely example of the difficulty and cost of trying to time markets.

The volatility from global sharemarkets has been extreme this year, nevertheless, the best thing would had been to sit back and enjoy the ride, as is often the case.

By way of example, the US S&P 500 sharemarket index reached a historical high on 19th February 2020. The market then fell into bear market territory (a decline of 20% or more) in record time, taking just 16 trading days, beating the previous record of 44 days set in 1929.

After falling 33% from the 19th February high global equity markets bounced back strongly over the following weeks, recording their best 50-day advance.

The benchmark dropped more than 5% on five days, four of which occurred in March. The same month also accounted for four of the five biggest gains.

Within the sharp bounce from the 23rd March lows, the US sharemarkets had two 9% single-day increases. Putting this into perspective, this is about equal to an average expected yearly return within one day!

For all the volatility, the US markets are nearly flat for the period since early February.

A recent Bloomberg article provides a good account of the cost of trying to time markets.

The Bloomberg article provides “One stark statistic highlighting the risk focuses on the penalty an investor incurs by sitting out the biggest single-day gains. Without the best five, for instance, a tepid 2020 becomes a horrendous one: a loss of 30%.”

As highlighted in the Bloomberg article, we all want to be active, we may even panic and sit on the side line, the key point is often the decision to get out can be made easily, however, the decision to get back in is a lot harder.

The cost of being wrong can be high.

Furthermore, there are better ways to manage market volatility, even as extreme as we have encountered this year.

For those interested, the following Kiwi Investor Blog Posts are relevant:

Navigating through a bear market – what should I do?

One of the best discussions I have seen on why to remain invested is provided by FutureSafe in a letter to their client’s 15th March 2020.

FutureSafe provide one reason why it might be the right thing for someone to reduce their sharemarket exposure and three reasons why they might not.

As they emphasis, consult your advisor or an investment professional before making any investment decisions.

I have summarised the main points of the FutureSafe letter to clients in this Post.

The key points to consider are:

- Risk Appetite should primarily drive your allocation to sharemarkets, not the current market environment;

- We can’t time markets, not even the professionals;

- Be disciplined and maintain a well-diversified investment portfolio, this is the best way to limit market declines, rather than trying to time market

- Take a longer-term view; and

- Seek out professional investment advice before making any investment decisions

Protecting your portfolio from different market environments

Avoiding large market losses is vital to accumulating wealth and reaching your investment objectives, whether that is attaining a desired standard of living in retirement or a lasting endowment.

The complexity and different approaches to providing portfolio protection has been highlighted by a recent twitter spat between Nassim Nicholas Taleb and Cliff Asness.

The differences in perspectives and approaches is very well captured by Bloomberg’s Aaron Brown article, Taleb-Asness Black Swan Spat Is a Teaching Moment.

I provide a summary of this debate in Table format in this Post.

Also covered in this Post is an article by PIMCO on Hedging for Different Market Scenarios. This provides another perspective and a summary of different strategies and their trade-offs in different market environments.

Not every type of risk-mitigating strategy can be expected to work in every type of market environment.

Therefore, maintaining an array of diversification strategies is preferred “investors should diversify their diversifiers”.

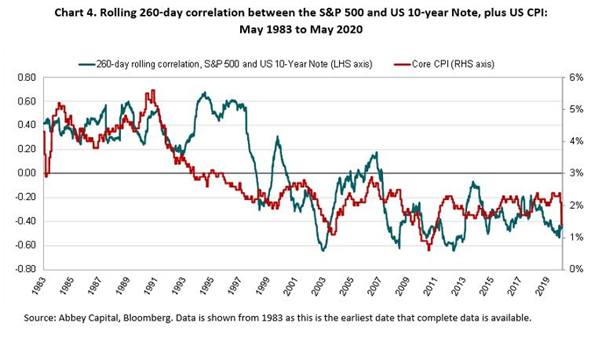

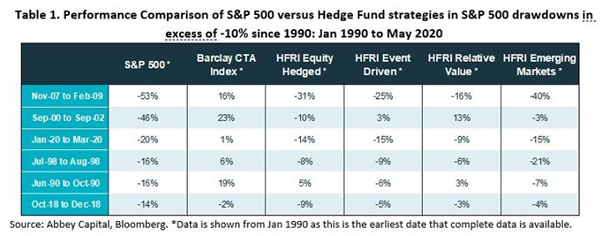

Sharemarket crashes, what works best in minimising loses, market timing or diversification?

The best way to manage periods of severe sharemarket declines is to have a diversified portfolio, it is impossible to time these episodes.

AQR has evaluated the effectiveness of diversifying investments during market drawdowns, which I cover in this Post.

They recommend adding investments that make money on average and have a low correlation to equities.

Although “hedges”, e.g. Gold, may make money at times of sharemarket crashes, there is a cost, they tend to do worse on average over the longer term.

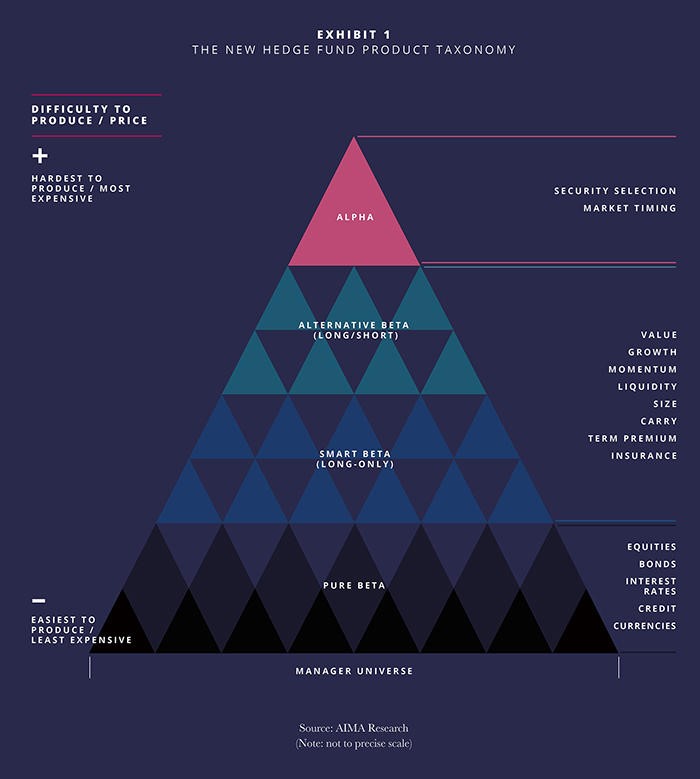

Alternative investments are more compelling relative to the traditional asset classes in diversifying a portfolio, they provide the benefits of diversification and have higher returns.

Portfolio diversification involves adding new “risks” to a portfolio, this can be hard to comprehend.

Happy investing.

Please see my Disclosure Statement