The most read Kiwi Investor Blog Posts in 2020 have been relevant to the current environment facing investors. They have also focused on building more robust portfolios.

The ultra-low interest rate environment and sobering low return forecasts present a bleak outlook for the Traditional Balanced Portfolio (60% Equities and 40% Fixed Income.) This outlook for the Balanced Portfolio was a developing theme in 2020, which gained greater prominence as the year progressed.

In essence, there are two themes that present a challenge for the Traditional Balanced Portfolio in the years ahead:

That fixed income and equities (mainly US equities) are expensive, so now may not be a great time to invest too heavily in these markets; and

With interest rates at very low levels, there is increasing doubt that fixed income can still effectively protect equity portfolios in a severe market decline in ways they have done historically.

My highest read Posts address the second theme above.

The Balance Portfolio has served investors well in recent years. Although equities and fixed income still have a role to play in the future, there is more that can be done.

The most read Kiwi Investor Blog Posts outline strategies that are “more that can be done”.

I have no doubt investors are going to have to look for alternative sources of returns and new asset classes outside equities and fixed income over the years ahead. In addition, investors will need to prepare for a period of higher inflation.

Not only will this help in increasing the odds of meeting investment return objectives; it will also help protect portfolios in periods of severe sharemarket declines, thus reducing portfolio volatility.

The best way to manage periods of severe sharemarket declines, as experienced in the first quarter of 2020, is to have a diversified portfolio. It is impossible to time these episodes.

Arguably the most prudent course of action for an investor to pursue in the years ahead is to take advantage of modern investment strategies that deliver portfolio diversification benefits and to employ more advanced portfolio construction techniques. Both of which have been successfully implemented by large institutional investors for many years.

From my perspective, maintaining an array of diversification strategies is preferred, investors should diversify their diversifiers.

The most read Kiwi Investor Blog Posts in 2020 were:

Canada’s largest Pension Funds plan to increase their investments into emerging markets over the following years. Asia, particularly India and China, are set to benefit.

The increased exposures are expected to be achieved by increasing portfolio target allocations to emerging markets, partnering on new deals, and boosting staff with expertise to the area.

The expected growth in the share of global economic activity in the years ahead and current attractive sharemarket valuations underpin the case for considering a higher weighting to emerging markets within portfolios. Particularly considering the low interest rate environment and stretched valuation of the US sharemarket. This dynamic is very evident in the market return forecasts provided below.

Additionally, emerging markets bring the benefits of diversification into different geographies and asset classes for investors, including both public and private markets.

As outlined in the P&I article, the Ontario Teachers’ Pension Plan (C$201.4 billion) is investing significantly into emerging markets, particularly Asia. Their exposure to emerging markets fluctuates between 10% and 20% of the total Portfolio.

The Fund’s investments across the emerging markets includes fixed income, infrastructure, and public and private equities. They plan to double the number of investment staff in Asia over the next few years, they already have an office in Hong Kong.

The Canada Pension Plan Investment Board (CPPIB) (C$400.6 billion) anticipates up to one-third of their fund to be invested in emerging markets by 2025.

CPPIB sees opportunities in both equity and debt. Investments in India are expected to grow, along with China.

The Attraction of Emerging Markets

The case for investing into emerging markets is well documented: rising share of global economic activity, under-representation in global market indices, and currently very attractive sharemarket valuations.

Although the current global economic and pandemic uncertainty provides pause for concern, the longer-term prospects for emerging market are encouraging.

From the P&I article “CPPIB estimates the share of global gross domestic product represented by emerging markets will reach 47% by 2025 and surpass the GDP of developed economies by 2029”.

Based on the expected growth outlook CPPIB “feel there are attractive returns available over the long term to those investors who take the time to study the characteristics and fundamentals of these markets and are able to identify trends and opportunities in those markets,”…..

CPPIB also highlight the benefit of diversification into different geographies and asset classes for the Fund.

Lastly, the valuations within emerging market sharemarkets are attractive.

This is highlighted in the following Table from GMO, which provides their latest (Sept 2020) Forecasts Annual Real Returns over the next 7 years (after inflation).

As can be seen, emerging market is one of only two asset classes that provides a positive return forecast. Emerging market value offers the prospect of the highest returns over the next 7 years. As GMO highlight, the forecasts are subject to numerous assumptions, risks and uncertainties. Actual results may differ from those forecasted.

Nevertheless, GMO provided the following brief commentary in this LinkedIn Post “From an absolute perspective, broad markets in the US are frighteningly bad; non-US developed markets, however, are not as bad, but that is faint praise, as our official forecast for this basket is also in negative territory. “Safe” bond forecasts are not much better. With yields this low, the very foundational justification for holding bonds — as providers of income and/or as anti-correlated money makers when equities decline — has been shaken to its core. The traditional 60/40 portfolio, consisting of heavy doses of US and International stocks and Government Bonds, is poised for a miserable and prolonged period.”

GMO Annual Real Returns over 7 years

In February 2020, GMO advised that it was time to move away from the Balanced Portfolio, as outlined in this Kiwi Investor Blog Post. GMO provide a historical performance of the traditional Balanced Portfolio (60% equities and 40% fixed income). Overall, the Balanced Fund is riskier than people think.

In the LinkedIn Post mentioned above, GMO comment that “Our Asset Allocation team believes this is the best opportunity set we’ve seen since 1999 in terms of looking as different as possible from a traditional benchmarked portfolio.” Where the traditional benchmarked portfolio is the Balanced Portfolio of 60% equities and 40% fixed income.

Why the Balanced Portfolio is expected to underperform and potential solutions to enhancing future portfolio returns is covered in this Post.

The Value Factor (value) offers the potential for additional returns relative to the broader sharemarket in the years ahead.

Exploring an array of different investment strategies and questioning the role of bonds in a portfolio are key to building a robust portfolio in the current low interest rate environment.

There will also be a need to be more dynamic and flexible to take advantage of market opportunities as they arise.

From this perspective, a value tilt within a portfolio is one investment strategy to consider in potentially boosting future investment returns.

The attraction of Value

Evidence supporting a value tilt within a robust portfolio is compelling, albeit opinion is split.

Nevertheless, longer-term, the “Rotating into Value stocks offers substantial upside in terms of return versus the broad market” according to GMO.

GMO presents the case for a value tilt to navigate today’s low interest rates in their Second Quarter 2020 Letter, which includes two insightful articles, one by Ben Inker and another by Matt Kadnar.

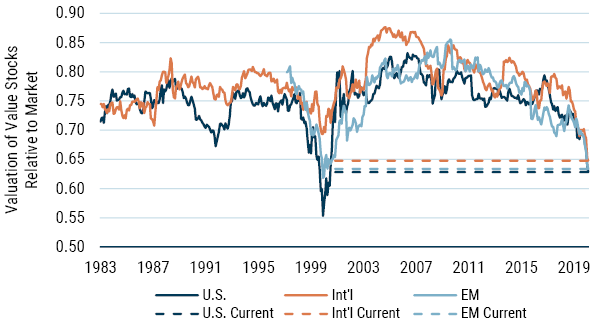

Value is at cheapest relative to the broader market since 1999, based on GMO’s analysis. Value is in the top decile of attractiveness around the world, as highlighted in the following figure.

Spread of Value for MSCI Regional Value Factors (GMO)

As of 6/30/2020 | Source: MSCI, Worldscope, GMO

Is Value Investing Dead

As mentioned, the opinion on value is split.

A research paper by AQR earlier in the year addressed the key criticisms of value, Is (Systematic) Value Investing Dead?

For a shorter read on the case for value Cliff Asness, of AQR, Blog Post of the same title is worth reading.

AQR’s analysis is consistent with GMO’s, as highlighted in the Graph and Table below.

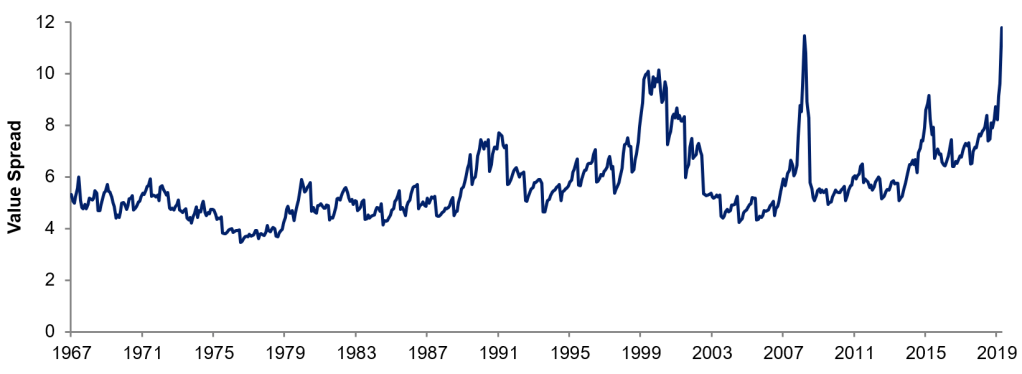

The Graph below measures the Price-to-Book spread of the whole US sharemarket from December 1967 to March 2020.

This spread was at the 100th percentile versus 50+ years of history on the 31 March 2020 i.e. value is at it cheapest based on 50 years of data.

Price-to-Book Spread (AQR)

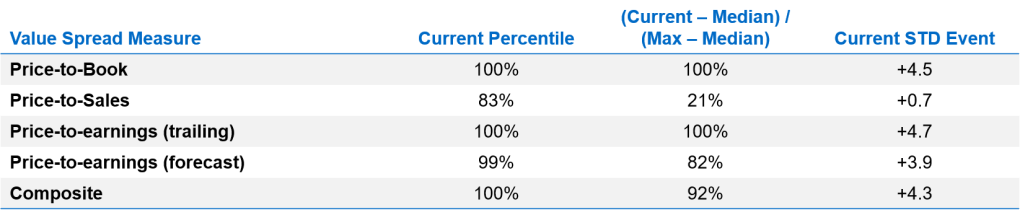

Asness’s Blog Post highlights “expensive stocks are sometimes only <4x as expensive as the cheap stocks, the median is that they are 5.4x more expensive, but today they are almost 12x more expensive.” (March 2020).

It is the same story when looking at different measures of value for the US sharemarket, as highlighted in the Table below.

Value is at its cheapest on many measures (AQR)

‘Don’t ask the barber whether you need a haircut’

This quote by Warren Buffett springs to mind when considering the analysis from GMO and AQR, both being value orientated investors. As Asness states, AQR has a horse in the race.

However, as outlined in his Post, he undertakes the same analysis as above and controls for, just to name a few:

Excluding all Technology, Media, and Telcom Stocks

Excluding the largest stocks

Excluding the most expensive stocks

Industry bets

Industry neutrality

Quality of company

Analysis is also undertaken using other measures of value, Price-Sales, P/E, using trailing and forecast earnings (these are in addition to Price-Book).

The attraction of value remains based on different measures of value and when making the adjustments to market indices as outlined above.

Asness argues value is exceptionally cheap, probably the cheapest it has ever been in history (March 2020).

The AQR analysis shows this is not because of an outdated price-to-book nor because of the dominance of highly expensive mega-cap stocks. Investors are paying more than usual for stocks they love versus the ones they hate. There is a very large mispricing.

The AQR research paper mentioned above, looked at the common criticisms of value, such as:

increased share repurchase activity;

the changing nature of firm activities, the rise of ‘intangibles’ and the impact of conservative accounting systems;

the changing nature of monetary policy and the potential impact of lower interest rates; and

value measures are too simple to work.

Across each criticism they find little evidence to support them.

Are we there yet?

We do not know when and how the valuation gap will be closed.

Nevertheless, the evidence is compelling in favour of maintaining a value tilt within a portfolio, and certainly now is not the time to give up on value.

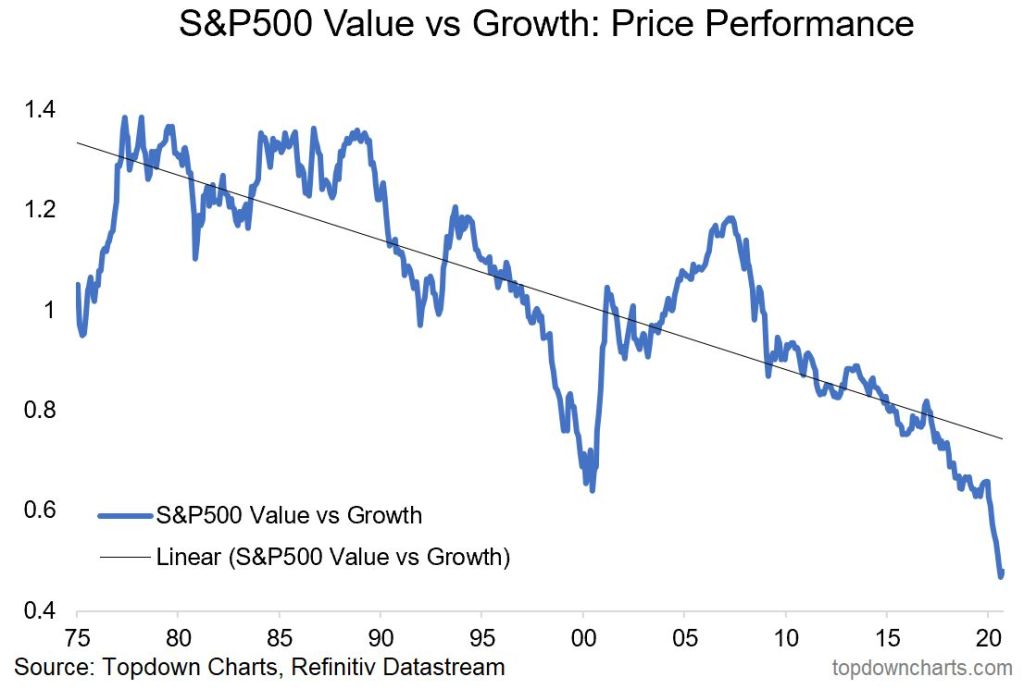

This is not a widely popular view, and quite likely a minority view, given the underperformance of value over the last ten years. As clearly demonstrated in the Graph below provided by Top Down Charts.

However, from an investment management perspective, the longer-term odds are in favour of maintaining a value tilt and thereby providing a boost to future investment returns in what is likely to be a low return environment over the next ten years.

It is too early to give up on value, news of its death are greatly exaggerated, on this, Asness makes the following point, value is “a strategy that’s “worked” through the 1920s – when a lot of stocks were railroads, steel, and steamship companies – through the Great Depression, WWII, the 1950s – which included some small technological changes like rural electrification, the space race and all the technology that it spanned – the internet age (remember these same stories for why value was broken back in 1999-2000?)………. Value certainly doesn’t depend on technological advancement being stagnant! But in a time when it’s failed for quite a while (again, that just happens sometimes even if it’s as good as we realistically think it is), it’s natural and proper that all the old questions get asked again. Is now different?”

The case for holding Government Bonds is all about certainty. The question isn’t why would you own bonds but, in the current environment, why wouldn’t you own bonds to deliver certainty in such uncertain times?

This is the central argument for holding government bonds within a portfolio. The case for holding government bonds is well presented in a recent article by Darren Langer, from Nikko Asset Management, Why you can’t afford not to own government bonds.

As he argues, government bonds are the only asset where you know with absolute certainty the amount of income you will get over its life and how much it will be worth on maturity. For most other assets, you will only ever know the true return in arrears.

The article examines some of the reasons why owning government bonds makes good sense in today’s investment and economic climate. It is well worth reading.

Why you can’t afford not to own government bonds

The argument against holding government bonds are based on expectations of higher interest rates, higher inflation, and current extremely low yields.

As argued in the article, although these are all very valid reasons for not holding government bonds, they all require a world economy that is growing strongly. This is far from the case currently.

They key point being made here, in my opinion, is that the future is unknown, and there are numerous likely economic and market outcomes.

Therefore, investors need to consider an array of likely scenarios and test their assumptions of what is “likely” to happen. For example, what is the ‘normal’ level of interest rates? Are they likely to return to normal levels when the experience since the Global Financial Crisis has been a slow grind to zero?

Personally, although inflation is not an issue now, I do think we should be preparing portfolios for a period of higher inflation, as I outline here. Albeit, this does not negate the role of fixed income in a portfolio.

The article argues that current conditions appear to be different and given this it is not unrealistic to expect that inflation and interest rates are likely to remain low for many years and significantly lower than the past 30 years.

In an uncertain world, government bonds provide certainty. Given multiple economic and market scenarios to consider, maintaining an allocation to government bonds in a genuinely diverse and robust portfolio does not appear unreasonable on this basis.

Return expectations

Investors should be prepared for lower rates of returns across all assets classes, not just fixed income.

A likely scenario is that governments and central banks will target an environment of stable and low interest rates for a prolonged period.

In this type of environment, government bonds have the potential to provide a reasonable return with some certainty. The article argues, the benefits to owning bonds under these conditions are two-fold:

A positively sloped yield curve in a market where yields are at or near their ceiling levels. Investors can move out the curve (i.e. by buying longer maturity bonds) to pick up higher coupon income without taking on more risk.

Investors can, over time, ride a position down the positively-sloped yield curve (i.e. over time the bond will gain in value from the passing of time because shorter rates are lower than longer rates). This is often described as roll-down return.

The article concludes, that although fixed income may lose money during times of strong economic growth, rising interest rates, and higher inflation, these losses can be offset by the gains on riskier assets in a portfolio. Losses on fixed income are small compared to potential losses on other asset classes and are generally recovered more quickly.

No one would suggest a 100% allocation to government bonds is a balanced investment strategy; likewise, not having an allocation to bonds should also be considered unbalanced.

“But a known return in an uncertain world, where returns on all asset classes are likely to be lower than the past, might just be a good thing to have in a portfolio.”

The article on the case for government bonds helps bring some balance to the discussion around fixed income and the points within should be considered when determining portfolio investment strategies in the current environment.