Investors seeking to generate higher returns are going to have to look for new sources of income, allocate to new asset classes, and potentially take on more risk.

Investing into a broader array of fixed income securities, dividend-paying equities, and alternatives such as real assets and private credit is likely required.

Investors will need to build more diversified portfolios.

These are key conclusions from a recent article written by Tony Rodriquez, of Nuveen, Rethinking the ‘40’ in 60/40 Portfolios, which appeared recently in thinkadvisor.com.

The 60/40 Portfolio being 60% equities and 40% fixed income, the Balanced Portfolio. The ‘40’ is the Balanced Portfolio’s 40% allocation to fixed income.

In my mind, the most value will be added in implementation of investment strategies and manager selection.

In addition, the opportunity for Investment Advisors and Consultants to add value to client investment outcomes over the coming years has probably never been more evident now than in recent history.

The value of good investment advice at this juncture will be invaluable.

Putting It All Together

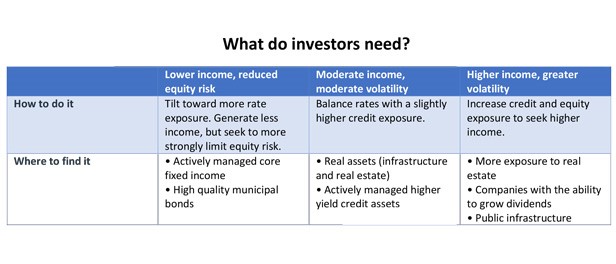

The thinkadvisor.com article provides the following Table.

This Table is useful in considering potential investment ideas. Actions taken will depend on the individual’s circumstances, including investment objectives, and risk tolerance.

The Table provides a framework across three dimensions to consider how to tackle the current investment challenge of very low interest rates.

Those dimensions are:

- The trade-off between level of income generated and risk tolerance (measured by portfolio volatility), e.g. lower income and reduced equity risk

- “How to do it” in meeting the trade-off identified above e.g. increase credit and equity exposures to seek higher income

- “Where to find it”, types of investments to implement How to do it e.g. active core fixed income, real assets (e.g. infrastructure and real estate), higher yielding credit assets.

Current Investment Environment

These insights reflect the current investment environment of extremely low interest rates.

More specifically the article starts with the following comments: “For decades, the 40% in the traditional 60/40 portfolio construction model was supposed to provide stable income with reduced volatility. But these days, finding income in the usual areas is as hard for me as a professional investor as it is for our clients.”

Tony calls for action, “With yields at historic lows, we’re forced to choose between accepting lower income or expanding into higher risk asset classes. We need to work together to change the definition of the 40 in the 60/40 split. So what do we do?”

This would be a worthy discussion for Investment Advisers and Consultants to have with their clients.

Returns from fixed income are relatively predictable, unlike equity market returns. Current fixed income yields are the best predictor of future returns. With global government bond yields around zero and global investment grade credit providing not much more, a return of greater than 1% p.a. from traditional global bond markets over the next 10 years is unlikely.

Fixed income returns over the next 10 years are highly likely to be below the rate of inflation. Therefore, the risk of the erosion of purchasing power from fixed income is very high. This is a portfolio risk that needs to be managed.

Although forecasted returns from equities are also low compared to history, they are higher than those expected from traditional fixed income markets.

What should Investors do?

The article provides some specific guidance in relation to fixed income investments and a view on the outlook for the global economy.

The key point from the article, in my mind, is that for investors to meet the current investment challenges over the next decade they are going to need a more broadly diversified portfolio than the traditional 60/40 portfolio.

I also think it is going to require greater levels of active management.

This will involve a rethink of the ‘40’ fixed income allocation. Specifically, the focus will be on generating higher returns and that fixed income is likely to provide less protection to a Balanced Portfolio at times of sharemarket declines than has been experienced historically.

Ultimately, a broader view of the 60/40 Portfolio’s construction will need to be undertaken.

This is likely to require thinking outside of the fixed income universe and implementing a more robust and truly diversified portfolio.

Implementation will be key, including strategy and manager selection.

There will still be a role for fixed income within a Portfolio, particularly duration. Depending on individual circumstances, higher yielding securities, emerging market debt, and active management of the entire fixed income universe, including duration, is something to consider. More of an absolute return focus may need to be contemplated.

Outside of fixed income, thought should be given to thinking broadly in implementing a more robust and truly diversified portfolio.

Kiwi Investor Blog has highlighted the following areas in previous Posts as a means to diversify a portfolio and address the current investment challenge:

- Real Assets offer real diversification: this Post outlines the investment risk and return characteristics of the different types of Real Assets and the diversification benefits they can bring to a Portfolio under different economic scenarios, e.g. inflation, stagflation.

- Sharemarket Crashes – what works best in minimising loses, market timing or diversification: This Post outlines the rationale for broad portfolio diversification to manage sharp sharemarket declines rather than trying to time markets. The Post presents the reasoning and benefits of investing into Alternative Assets.

- Is it an outdated Investment Strategy? If so, what should you do? Tail Risk Hedging: This Post outlines the case for Tail Risk Hedging. A potential strategy is to maintain a higher allocation to equities and to protect the risk of large losses through implementing a tail risk hedge.

- Protecting your portfolio from different market environments – including tail risk hedging debate: This Post compares the approach of broad portfolio diversification and tail risk hedging. Highlighting that that not one strategy can be effective in all market environments. Therefore, investors should diversify their diversifiers.

There have been a number of articles over recent months calling into question the robustness of the Balanced Portfolio of 60% Equities / 40% Fixed Income going forward. I have covered this issue in previous Posts, here and here.

Why the Balanced Portfolio is expected to underperform is outlined in this Post.

Lastly, also relevant to the above discussion, please see this Post on preparing Portfolios for higher levels of inflation.

Call to Action

In appealing to Tony’s call for action, there has probably never been a more important time in realising the value of good investment advice and honest conversations of investment objectives and portfolio allocations.

Perhaps it is time to push against some outdated conventions, seek new investments and asset classes.

The opportunity for Investment Advisors and Consultants to add value to client investment outcomes over the coming years has probably never been more evident now than in recent history.

The value of good investment advice at this juncture will be invaluable.

Addendum

For a perspective on the current market environment this podcast by Goldman Sachs may be of interest.

In the podcast, Goldman Sachs discuss their asset allocation strategy in the current environment, noting both fixed income and equities look expensive, this points to lower returns and higher risks for a Balanced Portfolio. They anticipate an environment of below average returns and above average volatility.

Happy investing.

Please see my Disclosure Statement

Pingback: Understanding the Impact of Volatility on your Portfolio | Kiwi Investor Blog

Pingback: The Case for holding Government Bonds | Kiwi Investor Blog

Pingback: Kiwi Investor Blog has published 150 Posts….. so far | Kiwi Investor Blog

Pingback: Coronavirus – Financial Planning Challenges | Kiwi Investor Blog

Pingback: Investment strategies for the year(s) ahead – how to add value to a portfolio | Kiwi Investor Blog