In a well-diversified portfolio, when one asset class is performing extremely well (like global equity markets), the diversified portfolio is unlikely to keep pace.

In these instances, the investor is likely to regret that they had reduced their exposure to that asset class in favour of greater portfolio diversification.

This is a key characteristic of having a well-diversified portfolio. On many occasions, some part of the portfolio will be “underperforming” (particularly relative to the asset class that is performing strongly).

Nevertheless, stay the course, over any given period, diversification will have won or lost but as that period gets longer diversification is more and more likely to win.

True diversification comes from introducing new risks into a portfolio. This can appear counter-intuitive. These new risks have their own risk and return profile that is largely independent of other investment strategies within the Portfolio. These new risks will perform well in some market environments and poorly in others.

Nevertheless, overtime the sum is greater than the parts.

The majority of the above insights are from a recent Willis Tower Watson (WTW) article on Diversification, Keep Calm and Diversify.

The article provides a clear and precise account of portfolio diversification. It is a great resource for those new to the topic and for those more familiar.

WTW conclude with the view “that true diversification is the best way to achieve strong risk adjusted returns and that portfolios with these characteristics will fare better than equities and diversified growth funds with high exposures to traditional asset classes in the years to come.”

Playing with our minds – Recent History

As the WTW article highlights the last ten-twenty years has been very unusual for both equity and bond markets have delivered excellent returns.

This is illustrated in the following chart they provide, the last two rolling 10-year periods have been periods of exceptional performance for a Balanced Portfolio (60%/40% equity/fixed income portfolio).

WTW made the following observations:

- The last ten years has tested the patience of investors when it comes to diversification;

- For those running truly diversified portfolios, this may be the worst time to change approach (the death of portfolio diversification is greatly exaggerated);

- Diversification offers ‘insurance’ against getting it wrong e.g. market timing; and

- Diversification has a positive return outcome, unlike most insurance.

WTW are not alone on their view of diversification, for example a AQR article from 2018 highlighted that diversification was the best way to manage periods of severe sharemarket declines, as recently experienced. I covered this paper in a recent Post: Sharemarket crashes – what works best in minimising losses, market timing or diversification.

WTW also note that it is difficult to believe that the next 10-year period will look like the period that has just gone.

There is no doubt we are in for a challenging investment environment based on many forecasted investment returns.

What is diversification?

WTW believe investors will be better served going forwards by building robust portfolios that exploit a range of return drivers such that no single risk dominates performance. (In a Balanced Portfolio of 60% equities, equities account for over 90% of portfolio risk.)

They argue true portfolio diversification is achieved by investing in a range of strategies that have low and varying levels of sensitivity (correlation) to traditional asset classes and in some instances have none at all.

Other sources of return, and risks, include investing in investment strategies with low levels of liquidity, accessing manager skill e.g. active returns above a market benchmark are a source of return diversification, and diversifying strategies that access return sources independent of traditional equity and fixed income returns. These strategies are also lowly correlated to traditional market returns.

Sources of Portfolio Diversification

Hedge Funds and Liquid Alternatives

Hedge Funds and Liquid Alternatives are an example of diversifying strategies mentioned above. As outlined in this Post, covering a paper by Vanguard, they both bring diversifying benefits to a traditional portfolio.

Access to the Vanguard paper can be found here.

It is worth highlighting that hedge fund and liquid alternative strategies do not provide a “hedge” to equity and fixed income markets.

Therefore they do not always provide a positive return when equity markets fall. Albeit, they do not decline as much at times of market crisis, as we have recently witnesses. Technically speaking their drawdowns (losses) are smaller relative to equity markets.

As evidenced in the Graph below provided by Mercer.

Private Markets

TWT also note there are opportunities within Private Markets to increase portfolio diversification.

There will be increasing opportunities in Private markets because fewer companies are choosing to list and there are greater restrictions on the banking sector’s ability to lend.

This is consistent with key findings of the recently published CAIA Association report, The Next Decade of Alternative Investments: From Adolescence to Responsible Citizenship.

The factors mentioned above, along with the low interest rate environment, the expected shortfall in superannuation accounts to meet future retirement obligations, and the maturing of emerging markets are expected to drive the growth in alternative investments over the decade ahead.

A copy of the CAIA report can be found here. I covered the report in a recent Post: CAIA Survey Results – The attraction of Alternative Investments and future trends.

TWT expect to see increasing opportunities across private markets, including a “range from investments in the acquisition, development, and operation of natural resources, infrastructure and real estate assets, fast-growing companies in overlooked parts of capital markets, and innovative early-stage ventures that can benefit from long-term megatrends.”

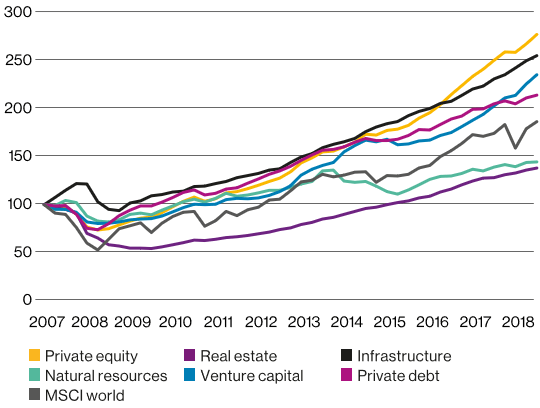

Continuing the theme of lending where the banks cannot, they also see the opportunity for increasing portfolios with allocations to Private Debt.

WTW provided the following graph, source data from Preqin

Real Assets

In addition to Hedge Funds, Liquid Alternatives, and Private markets (debt and equity), Real Assets are worthy of special mention.

Real assets such as Farmland, Timberland, Infrastructure, Natural Resources, Real Estate, TIPS (Inflation Protected Fixed Income Securities), Commodities, Foreign Currencies, and Gold offer real diversification benefits relative to equities and fixed income in different macro-economic environments, such as low economic growth, high inflation, stagflation, and stagnation.

These are a conclusive findings of a recent study by PGIM. The PGIM report on Real Assets can be found here. I provided a summary of their analysis in this Post: Real Assets offer real diversification benefits.

Conclusion

To diversify a portfolio it is recommended to add risk and return sources that make money on average and have a low correlation to equities.

Diversification should be true both in normal times and when most needed: during tough periods for sharemarkets.

Diversification is not the same thing as a hedge. Although “hedges” make money at times of sharemarket crashes, there is a cost, investments with better hedging characteristics tend to do worse on average over the longer term. Think of this as the cost of “insurance”.

Therefore, alternatives investments, as outlined above, are more compelling relative to the traditional asset classes in diversifying a portfolio, they provide the benefits of diversification and on average over time their returns tend to keep up with sharemarket returns.

Importantly, investing in more and more traditional asset classes does not equal more diversification e.g. listed property. As outlined in this Post.

As outlined above, we want to invest in a combination of lowly correlated asset classes, where returns are largely independent of each other. A combination of investment strategies that have largely different risk and return drivers.

Good luck, stay healthy and safe.

Happy investing.

Please see my Disclosure Statement

Global Investment Ideas from New Zealand. Building more Robust Investment Portfolios.

Like!! I blog frequently and I really thank you for your content. The article has truly peaked my interest.

LikeLike

Pingback: Kiwi Investor Blog has published 150 Posts….. so far | Kiwi Investor Blog

Pingback: Most read Kiwi Investor Blog Posts in 2020 | Kiwi Investor Blog

This blog is an amazing source of information and I’m so glad I found it!

LikeLike