GMO concluded some time ago the time was right to consider moving away from the 60/40 Portfolio. Which is a “Balanced Portfolio” of 60% equities and 40% fixed income.

In a more recent note, GMO identify two key problems that lie ahead for the Balanced Portfolio, which are supportive of their conclusion. Which I think are problems facing all investors, but particularly for US and New Zealand investors.

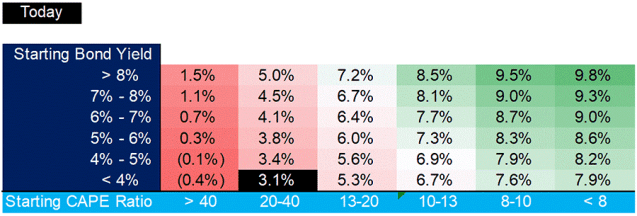

First, stock and bond valuations are both extended, suggesting they will deliver less than they have historically.

As GMO point out, the math with fixed income (bonds) is straightforward. The 10-Year U.S. Treasuries yield is under 1% today. New Zealand’s yield is also near 1%.

Today’s yield is the best predicator of future returns.

Real returns, after inflation, will likely be negative over the next 10 years from fixed income.

In short, GMO highlight “It is more or less impossible for a bond index yielding roughly 2% to deliver the 5% nominal returns investors have become accustomed to over any period of time approaching or exceeding the index’s duration.”

GMO also highlight stockmarket valuations have risen. Recent market weakness provides some valuation relief, albeit, US valuations remain elevated relative to history.

GMO conclude, “the passive 60/40 portfolio will likely deliver disappointing returns. The low starting yield of a 60/40 portfolio represents the first problem we see ahead.”

The second issue identified by GMO is that risks within fixed income have risen, and not just from a valuation perspective.

As can be seen in the graph below, provided by GMO, duration is near its highest level in history. (Duration is the key measure of risk for a fixed income portfolio. It measures the sensitivity of a fixed income security’s price movements to changes in interest rates.)

So, not only are interest rates at historical lows (low expected returns), but risk, as measured by duration, is amongst highest level in history.

This dynamic, low expected returns and heightened risk highlights the folly of an Index approach, similarly a set and forget approach in allocating to different asset classes. Similar dynamics also play out in sharemarket indices. Risks within markets vary over time.

Furthermore, the credit risk of many fixed income indices is also higher now than compared to the Global Financial Crisis. BBB and AA rated securities currently make up a greater proportion of the fixed income indices. Therefore, the credit quality of these indices has fallen over the last ten years, while the amount of corporate debt has grown. These dynamics need to be considered, preferably before the next credit crisis.

As GMO point out “Today, the sensitivity of a 60/40 portfolio to a change in yield is nearly as high as it has ever been. Both stocks and bonds are levered to future changes in discount and interest rates. Even a small amount of mean reversion upward in the aggregate yield of the 60/40 portfolio will be painful because there is less underlying yield to cushion any capital losses and those capital losses should be expected to be larger than normal for any change in yield given the high duration.”

Because of the higher duration and lower yields, smaller movements higher in interest rates will result in greater capital losses from fixed income securities compared to times when yields were higher. This is also the math.

At the same time, given the high valuation of sharemarkets, they are more susceptible to a movement higher in interest rates. Particularly those sectors of the equity market more sensitive to interest rate movements such as Listed Property.

Therefore, the historical diversification benefits from holding fixed income and equities are likely to less in the future.

GMO conclude “While investors have become conditioned to believe that a 60/40 portfolio delivers consistently strong returns, history shows this has not always been the case and the twin problems weighing on such a construction today suggest robust returns are unlikely going forward. Due to elevated valuations (low yields) and extended durations of both stocks and bonds, it is possible that in a future downturn investors will not receive the diversification they expect from their bond portfolio. Stocks and bonds have risen together and could certainly fall in unison as well.”

Although recent market events may have delayed this moment, they have not derailed the underlying dynamics within a Balanced Portfolio which will see it struggling to meet investor’s expectations over the next decade. The risks identify above remain.

The Balanced Portfolio is riskier than many appreciate. I covered this in a previous Post. It is not uncommon for the Balanced Portfolio to have a lost decade of returns and losses of up to 30% over a twelve-month period.

Possible Solution

To address the threats to the Balanced Portfolio identified above GMO suggest the inclusion of Liquid Alternatives across multi-asset portfolios.

Such strategies provided portfolio diversification, importantly they have very little duration risk within them, a risk both equities and fixed income are exposed too.

GMO articulate the benefits of such strategies as follows: “Liquid Alternatives can provide diversifying and uncorrelated returns. While Alternatives should not be expected to keep up with robust equity markets, they can help shield large drawdowns given their lower equity beta exposure.”

Liquid alternatives largely generate their return outcomes independently from the returns generated by equity markets (beta) and fixed income market (duration). Thus they provide exposure to different risk and return outcomes from equities and fixed income.

GMO conclude “Liquid alternatives improve the robustness of our multi-asset portfolios by helping to protect against the problems that today’s low yields and high durations present.”

The benefits of such strategies has been evident over the last few weeks, helping to diversify portfolios from the sharp fall in global sharemarkets as a result of the spreading of the coronavirus.

To finish, I would add to the GMO commentary that well diversified portfolios should also have an exposure to Real assets such as Farmland, Timberland, Infrastructure, Natural Resources, Real Estate, TIPS (Inflation Protected Fixed Income Securities), Commodities, Foreign Currencies, and Gold. These assets offer real diversification benefits relative to equities and fixed income, and to Balanced Portfolio in different macro-economic environments, such as low economic growth, high inflation, stagflation, and stagnation.

I covered the investment characteristics and benefits of Real Assets to a Balanced Portfolio in different economic environments in a recent Post.

Happy investing.

Please read my Disclosure Statement

Global Investment Ideas from New Zealand. Building more Robust Investment Portfolios.