The latest monthly commentary, for March 2021, can be found here.

Cautious Optimism

- Caution optimism prevailed across markets and economies as the global annus horribilis ended. Wishing you all an annus mirabilis for 2021 (a wonderful year).

- Global markets finished the year buoyed by the commencement of the Covid-19 vaccines roll out, ultra-low interest rates, and finally a new US government spending package.

- Global equities climbed 4.9% in December and are 16.9% higher than at the end of 2019. Who would have thought that was possible after the near 30% declines earlier in the year?

- The US sharemarket ended the year at historical highs. The S&P500 returned 18.4% in 2020 and is almost 70.0% higher from its yearly lows in late March.

- The New Zealand sharemarket also finished the year strongly, rising 5.5% in December, returning 14.7% in 2020. This is the Index’s ninth consecutive year of positive returns. The benchmark has more than quadrupled since the end of 2011, and more than doubled since 2015! (benchmark returns are based on S&P Dow Jones Index data).

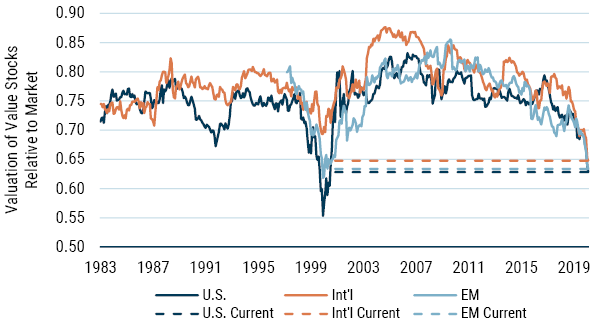

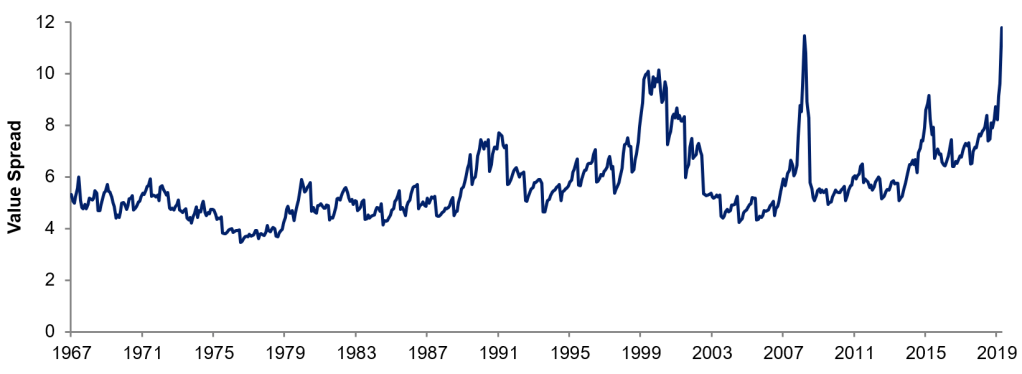

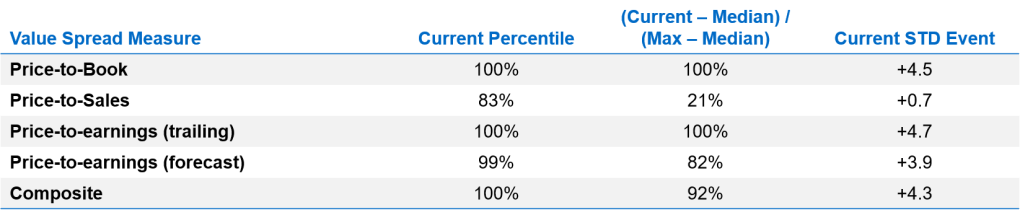

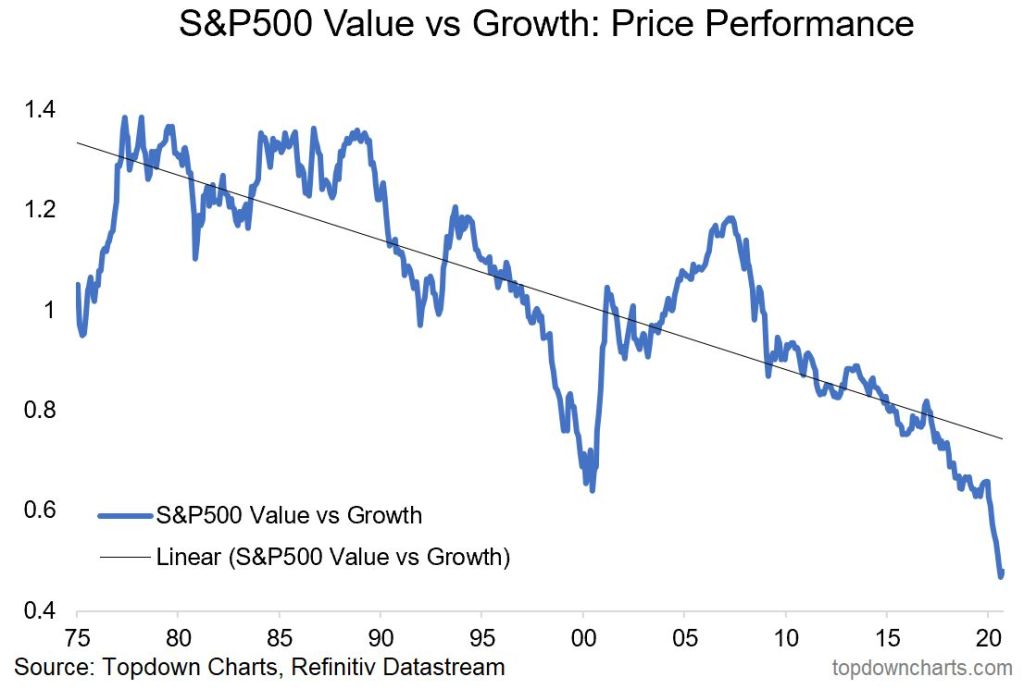

- The Australian sharemarket returned 1.2% in December, eking out 1.4% for the year. The Information Technology sector posted a 9.5% gain in December and 57.8% for the twelve months period. The energy sector lost 27.6% for the year, and utilities fell 16.7% over the same period. These sector relative performance outcomes have been experienced internationally, along with the momentum and growth factors outperforming value over the last twelve months. Although growth and momentum outperformed value in December they have trailed value over the last three months of 2020. In Australia, value returned 18.1% over the last quarter of 2020, momentum and growth returned 7.8% and 10.1% respectively.

- The V shape economic recovery is well on track around the world. The New Zealand economy expanded a stronger than expected 14% in the third quarter of 2020. This follows a historical 11% contraction in the second quarter. The economy is 2.2% smaller compared to a year ago. Construction and retail trade led the recovery following the second quarter lockdown. As the Kiwi Bank economics team highlighted, 95% of New Zealand’s economy is doing well, but the other 5%, primarily the tourism and education sectors, are not, and we should spare a thought for them. The peak over the Kiwi summer period, December – March, will be a test for them.

- As mentioned above, the USA has instigated additional government spending to combat COVID-19. The relief package is worth around $900 billion, 4% of the economy. It was larger than many expected and includes $600 personal payments to most Americans, along with additional unemployment benefits, and further support for businesses. This package should help to support US economic activity over the first quarter of 2021.

- Japan also announced additional economic stimulus measures in early December, this includes around 30 trillion Yen in additional spending to prevent the spread of COVID-19, transform the economy post the pandemic, and enhance infrastructure. The Japanese economy grew 5.3% in the July – September period, after declining 8.3% in the second quarter.

- Chinese industrial profits have grown 15% over the last year and exports are booming. Over the twelve months ending November Chinese exports have grown 21%, the highest level of annual growth in almost 10 years.

- European manufacturing activity has been stronger than expected, suggesting fourth quarter economic activity is going to be higher than anticipated.

- Likewise, US manufacturing has been resilient at a time of rising COVID-19 cases.

- In Australia, Consumer sentiment has reached its highest level in 10 years.

- The UK and Europe have agreed on a post-Brexit Free Trade Agreement that will result in zero tariffs and quotas on goods that comply with rules of origin. Terms on trade in services have also been reached, which are flexible reflecting the closeness of business activities.

The Year ahead

- Although economic activity is expected to moderate in the fourth quarter of 2020, given rising COVID-19 cases, complicated by the northern hemisphere winter, consensus expectations are for just over 5% global economic growth in 2021, led higher by Europe, UK, China, and India.

- After a sluggish start to the year the global economy should accelerate due to the rollout of the vaccines, and mass immunisation reduces the virus threat, the continued accommodative central bank policy settings of ultra-low interest rates, and government spending packages.

- More than 12 million vaccine doses have been administrated in 30 countries so far. Israel is leading with 10.5% of their population vaccinated. America has given out 4.3 million doses, 1.3% of their population. A World Health Organisation linked plan is in place to administer 2 billion vaccine doses globally in the first half of 2021.

- The US Federal Reserve’s (Fed) adoption of a flexible average inflation targeting will see global interest rates remain low for some time. The Fed is not expected to raise interest rates until 2025.

- In this environment, global equities are more than likely to outperform in the year ahead, global bond yields rise moderately, and the US dollar weakens further. Emerging markets are well placed in this environment, the value factor will benefit from greater economic certainty in 2021, and commodities such as oil may also find greater support.

- In America, Georgia Senate run-off elections in mid-January provide a short-term focal point for markets. The result will determine control of the US Senate. A switch to a Democratic party-controlled Senate will likely see changes to US tax policies in the months ahead.

- Inflation, although anticipated not to be an issue over the next few years, will become more of a threat in later years.

- Investors should prepare themselves for the risk of higher inflation as outlined in these Kiwi Investor Blog Posts: Preparing your Portfolio for a period of higher inflation and Asset Allocations decisions for the conundrum of inflation or deflation

Please read my Disclosure Statement