Balanced Funds are on track to experience one of their largest monthly losses on record.

Although this largely reflects the sharp and historical declines in global sharemarkets, fixed income has also not provided the level of portfolio diversification witnessed in previous Bear markets.

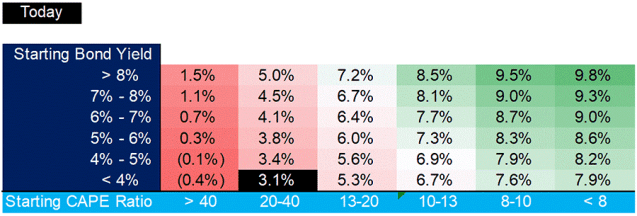

In the US, the Balanced Portfolio (60% Shares and 40% Fixed Income) is experiencing declines similar to those during the Global Financial Crisis (GFC) and 1987.

In other parts of the world the declines in the Balance Portfolio are their worst since the 1960s.

As you will be well aware the level of volatility in equity markets has been at historical highs.

After reaching a historical high on 19th February the US sharemarket, as measured by the S&P 500 Index, recorded:

- Its fastest correction from a peak, a fall of 10% but less than 19%, taking just 6 days; and

- Its quickest period to fall into a Bear market, a fall of greater than 20%, 22 days.

The S&P 500 entered Bear market territory on March 12th, when the market fell 9.5%, the largest daily drop since Black Monday in October 1987.

The 22 day plunge from 19th February’s historical high into a Bear market was half the time of the previous record set in 1929.

Volatility has also been historical to the upside, including near record highest daily positive returns and the most recent week was the best on record since the 1930s.

Volatility is likely to remain elevated for some time. The following is likely needed to be seen before there is a stabilisation of markets:

- The Policy response from Governments and Central Banks is sufficient to prevent a deepening of the global recessions;

- Coronavirus infection rates have peaked; and

- Cheap valuations.

Although currently there are cheap valuations, this is not sufficient to stabilise markets. Nevertheless, for those with a longer term perspective selective and measured investments may well offer attractive opportunities.

Please seek professional investment advice before making any investment decision.

For those interested, my previous Post outlined one reason why it might be the right thing for someone to reduce their sharemarket exposure and three reasons why they might not.

The Impact of Market Movements and Benefits of Rebalancing

My previous Post emphasised maintaining a disciplined investment approach.

Key among these is the consideration of continuing to rebalance an investment Portfolio.

Regular rebalancing of an investment portfolio adds value, this has been well documented by the research. The importance and benefits of Rebalancing was covered in a previous Kiwi Investor Blog Post which may be of interest: The balancing act of the least liked investment activity.

Rebalancing is a key investment discipline of a professional investment manager. A benefit of having your money professionally managed.

Assuming sharemarkets have fallen 25%, and no return from Fixed Income, within a Balanced Portfolio (60% Shares and 40% Fixed Income) the Sharemarket allocation has fallen to 53% of the portfolio.

Therefore, portfolios are less risky currently relative to longer-term investment objectives. A disciplined investment approach would suggest a strategy to address this issue needs to be developed.

As an aside, within a New Zealand Balanced Portfolio, if no rebalancing had been undertaken the sharemarket component would have grown from 60% to 67% over the last three years, reflecting the New Zealand Sharemarket has outperformed New Zealand Fixed Income by 10.75% per year over the last three years.

This meant, without rebalancing, Portfolios were running higher risk relative to long-term investment objectives entering the current Bear Market.

Although regular rebalancing would have trimmed portfolio returns on the way up, it would also have reduced Portfolio risk when entering the Bear Market.

As mentioned, the research is compelling on the benefits of rebalancing, it requires investment discipline. In part this reflects the drag on performance from volatility. In simple terms, if markets fall by 25%, they need to return 33% to regain the value lost.

Investing in a Challenging Investment Environment

No doubt, you will discuss any current concerns you have with your Trusted Advisor.

In a previous Post I reflected on the tried and true while investing in a Challenging investment environment.

I have summarised below:

Seek “True” portfolio Diversification

The following is technical in nature and I will explain below.

A recent AllAboutAlpha article referenced a Presentation by Deutsche Bank that makes “a very compelling case for building a more diversified portfolio across uncorrelated risk premia rather than asset class silos”.

For the professional Investor this Presentation is well worth reading: Rethinking Portfolio Construction and Risk Management.

The Presentation emphasises “The only insurance against regime shifts, black swans, the peso problem and drawdowns is to seek out multiple sources of risk premia across a host of asset classes and geographies, designed to harvest different features (value, momentum, illiquidity etc.) of the return generating process, via a large number of small, uncorrelated exposures”

We are currently experiencing a Black Swan, an unexpected event which has a major effect.

In a nutshell, the above comments are about seeking “true” portfolio diversification.

Portfolio diversification does not come from investing in more and more asset classes. This has diminishing diversification benefits over the longer term and particularly at time of market crisis.

True portfolio diversification is achieved by investing in different risk factors (also referred to as premia) that drive the asset classes e.g. duration (movements in interest rates), economic growth, low volatility, value, and market momentums by way of example.

Investors are compensated for being exposed to a range of different risks. For example, those risks may include market risk (e.g. equities and fixed income), smart beta (e.g. value and momentum factors), alternative, and hedge fund risk premia. And of course, “true alpha” from active management, returns that cannot be explained by the risk exposures just outlined.

There has been a disaggregation of investment returns.

US Endowment Funds and Sovereign Wealth Funds have led the charge on true portfolio diversification, along with the heavy investment into alternative investments and factor exposures.

They are a model of world best investment management practice.

Therefore, seek true portfolio diversification this is the best way to protect portfolio outcomes and reduce the reliance on sharemarkets and interest rates to drive portfolio outcomes. As the Deutsche Bank Presentation says, a truly diversified portfolio provides better protection against large market falls and unexpected events e.g. Black Swans.

True diversification leads to a more robust portfolio.

Customised investment solution

Often the next bit of advice is to make sure your investments are consistent with your risk preference.

Although this is important, it is also fundamentally important that the investment portfolio is customised to your investment objectives and takes into consideration a wider range of issues than risk preference and expected returns and volatility from investment markets.

For example, level of income earned up to retirement, assets outside super, legacies, desired standard of living in retirement, and Sequencing Risk (the period of most vulnerability is either side of the retirement age e.g. 65 here in New Zealand).

Also look to financial planning options to see through difficult market conditions.

Think long-term

I think this is a given, and it needs to be balanced with your investment objectives as outlined above.

Try to see through market noise and volatility.

It is all right to do nothing, don’t be compelled to trade, a less traded portfolio is likely more representative of someone taking a longer term view.

Remain disciplined.

There are a lot of Investment Behavioural issues to consider at this time to stop people making bad decisions, the idea of the Regret Portfolio approach may resonate, and the Behavioural Tool Kit could be of interest.

AllAboutAlpha has a great tagline: “Seek diversification, education, and know your risk tolerance. Investing is for the long term.”

Kiwi Investor Blog is all about education, it does not provide investment advice nor promote any investment, and receives no financial benefits. Please follow the links provided for a greater appreciation of the topic in discussion.

And, please, build robust investment portfolios. As Warren Buffet has said: “Predicting rain doesn’t count. Building arks does.” ………………….. Is your portfolio an all-weather portfolio?

Stay safe and healthy.

Happy investing.

Please see my Disclosure Statement