Extremely high valuations at a time of overwhelming uncertainty sits at the core of the case against US equities. The US equity market appears to be priced for a perfect outcome.

For those that demand a margin of safety, there is very little safety margin right now in US equities.

GMO’s James Montier recently outlined the reasons not to be cheerful toward US equities.

This contrasts with Goldman Sachs 10 reasons why the US equity market will move higher from here, which I covered in my last Post.

In the GMO article it is argued the US sharemarket is priced with too much certainty for a positive outcome. Nevertheless, with so much uncertainty, such as shape of the economic recovery and effectiveness of efforts in containing further outbreaks of the coronavirus, investors should demand a margin of safety, “wriggle room for bad outcomes if you like”.

The article concludes there is no margin of safety in the pricing of US stocks today.

In his view, “The U.S. stock market looks increasingly like the hapless Wile E. Coyote, running off the edge of a cliff in pursuit of the pesky Roadrunner but not yet realizing the ground beneath his feet had run out some time ago”.

This view in part reflects that GMO does not fully support the narrative that has primarily driven the recovery in the US stock market over recent months and is expected to provide further support.

The centre of the positive market outlook narrative is the US Federal Reserves’ (Fed) Quantitative Easing program (QE). QE involves the buying of market securities, leading to an expansion of the Fed’s Balance Sheet.

In short, Montier thinks it is tricky to argue any direct linkage from the Fed’s balance sheet expansion programs to equities. In previous Fed QE periods longer-term interest rates rose, which is not supportive of equities. It is also observed, in other parts of the world where interest rates are low, equity markets are not trading on extreme valuations like in the US.

On this he concludes the “Fed-based explanations are at best ex post justifications for the performance of the stock market; at worst they are part of a dangerously incorrect narrative driving sentiment (and prices higher).”

Further detail is provided below on why he is skeptical of positive market outlook narrative centred around ongoing support for the Fed’s policy.

The article concludes:

“Investing is always about making decisions while under a cloud of uncertainty. It is how one deals with the uncertainty that distinguishes the long-term value-based investors from the rest. Rather than acting as if the uncertainty doesn’t exist (the current fad), the value investor embraces it and demands a margin of safety to reflect the unknown. There is no margin of safety in the pricing of U.S. stocks today. Voltaire observed, “Doubt is not a pleasant condition, but certainty is absurd.” The U.S. stock market appears to be absurd.”

This view is consistent with a “long term value” based investor and has some validity. From this perspective, the investment rationale provides a counterbalance to Goldman’s 10 reasons.

The counter argument to GMO’s interest rate view is that the fall in interest rates reflects higher private sector savings and easier monetary policy rather than pessimism about growth and corporate earnings. Reflecting the expansionary polices of both governments and central banks corporate earnings will recover. Although weaker, the temporary fall in corporate earnings are not in proportion to that implied by lower interest rates. This means lower interest rates really do justify higher market valuations.

Also, the two contrasting views could be correct, the only difference being a matter of time.

Implementation of investment strategy is key at this juncture in the economic and market cycle, more so than at any time over the last 20 years.

Historical sharemarket movements and over valuation

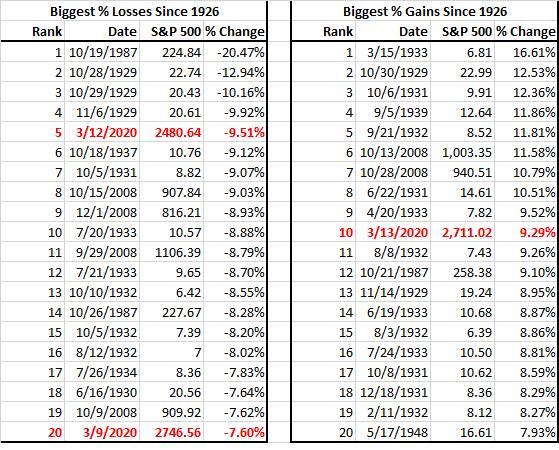

Since reaching the lows of 23rd March 2020, the U.S. equity market has rallied almost 50% and other world markets nearly 40%.

The movements in markets have been historic from the perspective of both the speed and scale of the market declines and their rebound.

GMO provide the following graph to demonstrate how sharp the fall and rebound by comparing the Covid-19 decline to others in history, as outlined in the following graph they provide:

The sharp rebound in markets has pushed the US markets back up to extreme valuation levels.

The article outlines the following observations:

- In 1929 the U.S. market P/E was 37% above its long-term average, and earnings relative to 10-year earnings were 46% above their normal level

- In 2000 the market P/E was 98% above its average, and earnings relative to 10-year average earnings were 37% above their normal level.

As displayed in the following graph provided, valuations are in the 95th percentile, “right up there in terms of one of the most expensive markets of all time”.

It is clear to see there is very little margin for safety with such high valuation levels set against an uncertainty economic environment.

Accommodative US Federal Reserve Policy

A portion of the GMO article addresses the notion that an expanding Fed Balance Sheet will continue to support US equities. The notion being that QE lowers interest rates, reducing the discount rate, and therefore drives up stock markets.

James prefers to focus on fundamentals and therefore has several issues with this viewpoint:

- He is skeptical of a clear link between interest rates and equity valuations. As noted, Japan and Europe both have exceptionally low interest rates, but their stock markets are not trading on extreme market valuation like the US.

- Interest rates are low because economic growth is low, this needs to be reflected in company valuations. See the note below, Role of Interest Rates for a fuller explanation.

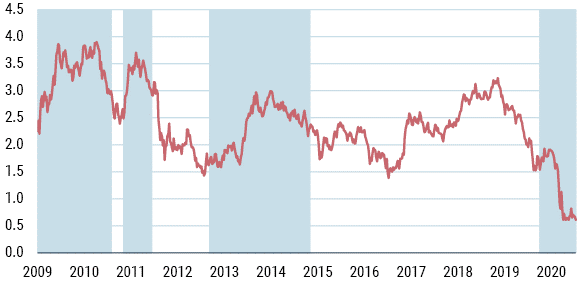

- QE hasn’t actually managed to lower interest rates. As can be seen in the Graph below, all three of the completed cycles of QE have actually ended with interest rates higher than they were when the QE began.

The graph also highlights how low US interest rates are!

A Note on the Role of Interest Rates

The following extract from the Article outlines James’ explanation as to the Role of Interest Rates:

“I am no longer unique in my questioning of the role of interest rates. The good people at AQR Capital released a paper in May 2020 entitled “Value and Interest Rates: Are Rates to Blame for Value’s Torments?” In it they say, “As the risk-free interest rate is one component of the discount rate, when interest rates go up, the discount rate increases and the asset price falls – if everything else stays constant. Hence, if expected cash flows are unchanged and if the risk premium associated with those cash flows is unchanged (where the risk premium is determined by both the amount of risk exposure the cash flows have and the price of aggregate risk to those exposures in the economy), then the formula tells us how prices will change when riskless interest rates change. However, in the case of stocks, these other components rarely stay constant. Changes in real or nominal interest rates are often accompanied by (or are often a response to) changes in expected inflation and/or changes in expected economic growth, and hence expected cashflows are often changing as well. There may also be a change in the required risk premium, which is the other (and often larger) component of the discount rate. All of these components have their own dynamics and are likely simultaneously being affected by macroeconomic conditions in possibly different ways.”

Please see my Disclosure Statement