The case for holding Government Bonds is all about certainty. The question isn’t why would you own bonds but, in the current environment, why wouldn’t you own bonds to deliver certainty in such uncertain times?

This is the central argument for holding government bonds within a portfolio. The case for holding government bonds is well presented in a recent article by Darren Langer, from Nikko Asset Management, Why you can’t afford not to own government bonds.

As he argues, government bonds are the only asset where you know with absolute certainty the amount of income you will get over its life and how much it will be worth on maturity. For most other assets, you will only ever know the true return in arrears.

The article examines some of the reasons why owning government bonds makes good sense in today’s investment and economic climate. It is well worth reading.

Why you can’t afford not to own government bonds

The argument against holding government bonds are based on expectations of higher interest rates, higher inflation, and current extremely low yields.

As argued in the article, although these are all very valid reasons for not holding government bonds, they all require a world economy that is growing strongly. This is far from the case currently.

They key point being made here, in my opinion, is that the future is unknown, and there are numerous likely economic and market outcomes.

Therefore, investors need to consider an array of likely scenarios and test their assumptions of what is “likely” to happen. For example, what is the ‘normal’ level of interest rates? Are they likely to return to normal levels when the experience since the Global Financial Crisis has been a slow grind to zero?

Personally, although inflation is not an issue now, I do think we should be preparing portfolios for a period of higher inflation, as I outline here. Albeit, this does not negate the role of fixed income in a portfolio.

The article argues that current conditions appear to be different and given this it is not unrealistic to expect that inflation and interest rates are likely to remain low for many years and significantly lower than the past 30 years.

In an uncertain world, government bonds provide certainty. Given multiple economic and market scenarios to consider, maintaining an allocation to government bonds in a genuinely diverse and robust portfolio does not appear unreasonable on this basis.

Return expectations

Investors should be prepared for lower rates of returns across all assets classes, not just fixed income.

A likely scenario is that governments and central banks will target an environment of stable and low interest rates for a prolonged period.

In this type of environment, government bonds have the potential to provide a reasonable return with some certainty. The article argues, the benefits to owning bonds under these conditions are two-fold:

A positively sloped yield curve in a market where yields are at or near their ceiling levels. Investors can move out the curve (i.e. by buying longer maturity bonds) to pick up higher coupon income without taking on more risk.

Investors can, over time, ride a position down the positively-sloped yield curve (i.e. over time the bond will gain in value from the passing of time because shorter rates are lower than longer rates). This is often described as roll-down return.

The article concludes, that although fixed income may lose money during times of strong economic growth, rising interest rates, and higher inflation, these losses can be offset by the gains on riskier assets in a portfolio. Losses on fixed income are small compared to potential losses on other asset classes and are generally recovered more quickly.

No one would suggest a 100% allocation to government bonds is a balanced investment strategy; likewise, not having an allocation to bonds should also be considered unbalanced.

“But a known return in an uncertain world, where returns on all asset classes are likely to be lower than the past, might just be a good thing to have in a portfolio.”

The article on the case for government bonds helps bring some balance to the discussion around fixed income and the points within should be considered when determining portfolio investment strategies in the current environment.

A key investment concept is volatility drag. Volatility drag provides a framework for considering the trade-off between the “cost” and “benefit” of reducing portfolio volatility.

The volatility of your portfolio matters. Reducing portfolio volatility helps deliver higher compound returns over the longer-term. This leads to a greater accumulation of wealth over time.

When introducing volatility reduction strategies into a Portfolio a cost benefit analysis should be undertaken.

The cost of reducing portfolio volatility cannot be considered in isolation.

The importance of volatility and its impact on an investment portfolio is captured in a recent article by Aberdeen Standard Investment (ASI), The long-term benefits of finding the right hedging strategy.

The ASI article is summarised below. Access to article via LinkedIn is here.

It is widely accept that avoiding large market losses and reducing portfolio volatility is vital in accumulating wealth and reaching your investment objectives, whether that is attaining a desired standard of living in retirement, an ongoing and uninterrupted endowment, or meeting Pension liabilities.

Understanding Volatility Drag

Volatility Drag is a key concept from the paper: if you lose 50% one year, and make 50% the next, your average return may be zero but you’re still down 25%. This is commonly referred to as the “volatility drag.”

The main disconnect some investors have is they look at returns over a discrete period, such as a year, or the simple average return over two years (zero in the case above).

Instead, investors should focus on the realised compound rate. The compound annualised return in the above example is -13.97% versus simple average return of zero.

ASI make the following point: “The compound (geometric) rate of return will only equal the arithmetic average rate of return if volatility is zero. As soon as you introduce volatility to the return series, the geometric IRR will start falling, relative to the average return.”

This is a key concept to understand. Volatility reduces compounded returns over time, therefore it impacts on accumulated wealth. The focus should be on the actual return investors receive, rather than discrete period returns. Most investment professionals understand this.

Cashflows, into and out of a Portfolio, also impact on actual returns and therefore accumulated wealth. This is why a 100% equities portfolio is unlikely to be appropriate for the vast majority of investors. The short comings of a high equity allocations is outlined in one of my previous Posts: Could Buffett be wrong?

Thought Experiment

In the article ASI offers a thought experiment to make their point, a choice between two hypothetical investments:

Investment A, has an average annual return of 1% with 5% volatility.

Investment B, has twice the average return (2%) but with four times the volatility (20%).

An investor with a long term horizon might allocate to the higher expected return investment and not worry about the higher levels of volatility. The view could be taken because you have a longer term investment horizon more risk can be taken to be rewarded with higher returns.

In the article ASI provides simulated track records of the two investments over 50 years (the graph is well worth looking at).

As would be expected, Investment B with the 20% volatility has a much wider range of possible paths than the lower-volatility Investment A.

What is most interesting “despite having double the average annual return, the more volatile strategy generally underperforms over the long term.”

This is evident in the Table below from the ASI article, based on simulated investment returns:

Average Annual Return

Standard Deviation of Annual Returns

Average total return after 50 years

Average realised internal rate of return (IRR)

A

1%

5%

+53%

0.88%

B

2%

20%

-3.0%

-0.07%

Note, how the IRR is lower than the average annual return e.g. Investment A, IRR is 0.88% versus average annual return of 1.0%. As noted above, they are only the same if volatility is zero.

The performance drag, or “cost”, is due to volatility.

Implications and recognising the importance of volatility

The concept of Volatility Drag provides a framework for considering the trade-off between the “cost” and benefit of reducing portfolio volatility.

The ASI article presents this specifically in relation to the benefits of portfolio hedges, as part of a risk mitigation strategy, and their costs with the following points:

The annual cost can be considered in the context of the potential benefits that come from lowering volatility and more effectively compounding returns.

Putting on exposures with flat or even negative expected returns can still increase your total portfolio return over time if they lower your volatility profile sufficiently.

It is meaningless, therefore, to look at the costs of hedges in isolation.

These points are relevant when considering introducing any volatility reduction strategies into an Investment Portfolio i.e. not just in relation to tail risk hedging. A cost benefit analysis should be undertaken, investment costs cannot be considered in isolation.

As ASI note, investors need to consider the overall portfolio impact of introducing new investment strategies, specifically the impact on the downside volatility of a portfolio is critical.

There are a number of ways of reducing portfolios volatility as outlined below, including the risk mitigation strategies of the ASI article.

Modern Portfolios

The key point is that the volatility of your portfolio matters. Reducing portfolio volatility helps in delivering better compound returns over the longer-term.

Therefore, exploring ways to reduce portfolio volatility is important.

ASI outline the expectation that volatility is likely to pick up in the years ahead, “especially considering the current extreme settings for fiscal and monetary policy combined with rising geopolitical tensions.”

They also make the following pertinent comment, “Uncertainty and volatility aren’t signals for investors to exit the market, but while they persist, we expect investors will benefit over the medium term from having strategies available to them that can help manage downside volatility.”

ASI also note that investors have access to a wide range of tools and strategies to manage volatility. This is particularly relevant in relation to the risk mitigation hedging strategies that manage downside volatility and are the focus of the ASI article.

Therefore, a modern day portfolio will implement several strategies and approaches to reduce portfolio volatility, primarily as a means to generate higher compound returns over time. This is evident when looking at industry leading sovereign wealth funds, pension funds, superannuation funds, endowments, and foundations around the world.

Strategies and Approaches to reducing Portfolio Volatility

There are a number of strategies and approaches to reducing portfolio volatility, Kiwi Investor Blog has recently covered the following:

Real Assets offer real diversification: this Post outlines the investment risk and return characteristics of the different types of Real Assets and the diversification benefits they can bring to a Portfolio under different economic scenarios, e.g. inflation, stagflation. Thus reducing portfolio volatility and enhancing long-term accumulated returns.

What do investors need in the current environment? – Rethink the ‘40’ in the 60/40 Portfolios?: With extremely low interest rates and the likelihood fixed income will not provide the level of portfolio diversification as experienced historically this Post concludes Investors will need to rethink their fixed income allocations and to think more broadly in diversifying their investment portfolio.

Investors seeking to generate higher returns are going to have to look for new sources of income, allocate to new asset classes, and potentially take on more risk.

Investing into a broader array of fixed income securities, dividend-paying equities, and alternatives such as real assets and private credit is likely required.

Investors will need to build more diversified portfolios.

These are key conclusions from a recent article written by Tony Rodriquez, of Nuveen, Rethinking the ‘40’ in 60/40 Portfolios, which appeared recently in thinkadvisor.com.

The 60/40 Portfolio being 60% equities and 40% fixed income, the Balanced Portfolio. The ‘40’ is the Balanced Portfolio’s 40% allocation to fixed income.

In my mind, the most value will be added in implementation of investment strategies and manager selection.

In addition, the opportunity for Investment Advisors and Consultants to add value to client investment outcomes over the coming years has probably never been more evident now than in recent history.

The value of good investment advice at this juncture will be invaluable.

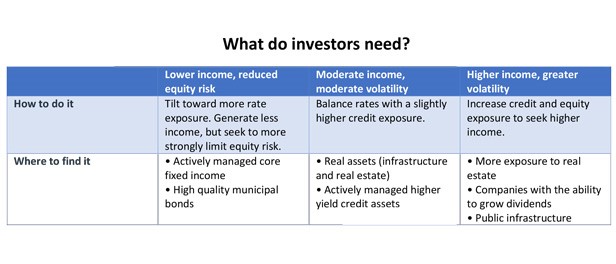

Putting It All Together

The thinkadvisor.com article provides the following Table.

Source: Nuveen

This Table is useful in considering potential investment ideas. Actions taken will depend on the individual’s circumstances, including investment objectives, and risk tolerance.

The Table provides a framework across three dimensions to consider how to tackle the current investment challenge of very low interest rates.

Those dimensions are:

The trade-off between level of income generated and risk tolerance (measured by portfolio volatility), e.g. lower income and reduced equity risk

“How to do it” in meeting the trade-off identified above e.g. increase credit and equity exposures to seek higher income

“Where to find it”, types of investments to implement How to do it e.g. active core fixed income, real assets (e.g. infrastructure and real estate), higher yielding credit assets.

Current Investment Environment

These insights reflect the current investment environment of extremely low interest rates.

More specifically the article starts with the following comments: “For decades, the 40% in the traditional 60/40 portfolio construction model was supposed to provide stable income with reduced volatility. But these days, finding income in the usual areas is as hard for me as a professional investor as it is for our clients.”

Tony calls for action, “With yields at historic lows, we’re forced to choose between accepting lower income or expanding into higher risk asset classes. We need to work together to change the definition of the 40 in the 60/40 split. So what do we do?”

This would be a worthy discussion for Investment Advisers and Consultants to have with their clients.

Returns from fixed income are relatively predictable, unlike equity market returns. Current fixed income yields are the best predictor of future returns. With global government bond yields around zero and global investment grade credit providing not much more, a return of greater than 1% p.a. from traditional global bond markets over the next 10 years is unlikely.

Fixed income returns over the next 10 years are highly likely to be below the rate of inflation. Therefore, the risk of the erosion of purchasing power from fixed income is very high. This is a portfolio risk that needs to be managed.

Although forecasted returns from equities are also low compared to history, they are higher than those expected from traditional fixed income markets.

What should Investors do?

The article provides some specific guidance in relation to fixed income investments and a view on the outlook for the global economy.

The key point from the article, in my mind, is that for investors to meet the current investment challenges over the next decade they are going to need a more broadly diversified portfolio than the traditional 60/40 portfolio.

I also think it is going to require greater levels of active management.

This will involve a rethink of the ‘40’ fixed income allocation. Specifically, the focus will be on generating higher returns and that fixed income is likely to provide less protection to a Balanced Portfolio at times of sharemarket declines than has been experienced historically.

Ultimately, a broader view of the 60/40 Portfolio’s construction will need to be undertaken.

This is likely to require thinking outside of the fixed income universe and implementing a more robust and truly diversified portfolio.

Implementation will be key, including strategy and manager selection.

There will still be a role for fixed income within a Portfolio, particularly duration. Depending on individual circumstances, higher yielding securities, emerging market debt, and active management of the entire fixed income universe, including duration, is something to consider. More of an absolute return focus may need to be contemplated.

Outside of fixed income, thought should be given to thinking broadly in implementing a more robust and truly diversified portfolio.

Kiwi Investor Blog has highlighted the following areas in previous Posts as a means to diversify a portfolio and address the current investment challenge:

Real Assets offer real diversification: this Post outlines the investment risk and return characteristics of the different types of Real Assets and the diversification benefits they can bring to a Portfolio under different economic scenarios, e.g. inflation, stagflation.

There have been a number of articles over recent months calling into question the robustness of the Balanced Portfolio of 60% Equities / 40% Fixed Income going forward. I have covered this issue in previous Posts, here and here.

Why the Balanced Portfolio is expected to underperform is outlined in this Post.

Lastly, also relevant to the above discussion, please see this Post on preparing Portfolios for higher levels of inflation.

Call to Action

In appealing to Tony’s call for action, there has probably never been a more important time in realising the value of good investment advice and honest conversations of investment objectives and portfolio allocations.

Perhaps it is time to push against some outdated conventions, seek new investments and asset classes.

The opportunity for Investment Advisors and Consultants to add value to client investment outcomes over the coming years has probably never been more evident now than in recent history.

The value of good investment advice at this juncture will be invaluable.

Addendum

For a perspective on the current market environment this podcast by Goldman Sachs may be of interest.

In the podcast, Goldman Sachs discuss their asset allocation strategy in the current environment, noting both fixed income and equities look expensive, this points to lower returns and higher risks for a Balanced Portfolio. They anticipate an environment of below average returns and above average volatility.

Those saving for retirement face the reality that fixed income may no longer serve as an effective portfolio diversifier and source of meaningful returns.

In future fixed income is unlikely to provide the same level of offset in a portfolio as has transpired historically when the inevitable sharp decline in sharemarkets occur – which tend to happen more often than anticipated.

The expected reduced diversification benefit of fixed income is a growing view among many investment professionals. In addition, forecast returns from fixed income, and cash, are extremely low. Both are likely to deliver returns around, if not below, the rate of inflation over the next 5 – 10 years.

Notwithstanding this, there is still a role for fixed income within a portfolio.

However, there is still a very important portfolio construction issue to address. It is a major challenge for retirement savings portfolios, particularly those portfolios with high allocations to cash and fixed income.

In effect, this challenge is about exploring alternatives to traditional portfolio diversification, as expressed by the Balanced Portfolio of 60% Equities / 40% Fixed Income. I have covered this issue in previous Posts, here and here.

Outdated Investment Strategy

There are many ways to approach the current challenge, which investment committees, Trustees, and Plan Sponsors world-wide must surely be considering, at the very least analysing and reviewing, and hopefully addressing.

One way to approach this issue, and the focus of this Post, is Tail Risk Hedging. (I comment on other approaches below.)

The case for Tail Risk Hedging is well presented in this opinion piece, Investors Are Clinging to an Outdated Strategy At the Worst Possible Time, which appeared in Institutional Investor.com

The article is written by Ron Lagnado, who is a director at Universa Investments. Universa Investments is an investment management firm that specialises in risk mitigation e.g. tail risk hedging.

The article makes several interesting observations and lays out the case for Tail Risk Hedging in the context of the underfunding of US Pension Plans. Albeit, there are other situations in which the consideration of Tail Risk Hedging would also be applicable.

The framework for Equity Tail Risk Hedging, recognises “that management of portfolio risk and equity tail risk, in particular, was the key driver of long-term compound returns.”

By way of positioning, the article argues that a reduction in Portfolio volatility leads to better investment outcomes overtime, as measured by the Compound Annual Growth Return (CAGR). There is validity to this argument, the reduction in portfolio volatility is paramount to successful investment outcomes over the longer-term.

The traditional Balance Portfolio, 60/40 mix of equities and fixed income, is supposed to mitigate the effects of extreme market volatility and deliver on return expectations.

Nevertheless, it is argued in the article that the Balanced Portfolio “limits portfolio volatility in benign market environments over the short term while making huge sacrifices in long-run performance.”

In other words, “It offers scant protection against tail risk and, at the same time, achieves an under-allocation to riskier assets with higher returns in long periods of economic expansion, such as the past decade.”

The article provides some evidence of this, highlighting that “large allocation to bonds still failed to provide enough protection to add value over the cycle — reducing the CAGR by 170 basis points.”

Essentially, the argument is made that the Balanced Portfolio has not delivered on its promise historically and is an outdated strategy, particularly considering the current market environment and the outlook for investment returns.

Meeting the Challenge – Tail Risk Hedging

The article calls for the consideration of different approaches to the traditional Balance Portfolio. Naturally, they call for Tail Risk Hedging.

In effect, the strategy is to maintain a higher allocation to equities and to protect the risk of large losses through implementing a tail risk hedge (protection of large equity loses).

It is argued that this will result in a higher CAGR over the longer term given a higher allocation to equities and without the drag on performance from fixed income.

The Tail Risk Hedge strategy is implemented via an options strategy.

As they note, there is no free lunch with this strategy, an “options strategies trade small losses over extended periods when equities are rising for extremely large gains during the less frequent but devastating drawdowns.”

This is the inverse to some investment strategies, which provide incremental gains over extended periods and then short sharp losses. There is indeed no free lunch.

My View

The article concludes, “diversification for its own sake is not a strategy for success.”

I would have to disagree. True portfolio diversification is the closest thing to a free lunch in Portfolio Management.

However, this does not discount the use of Tail Risk Hedging.

The implementation of any investment strategy needs to be consistent with client’s investment philosophy, objectives, fee budgets, ability to implement, and risk appetite, including the level of comfort with strategies employed.

Broad portfolio diversification versus Tail Risk Hedging has been an area of hot debate recently. It is good to take in and consider a wide range of views.

The debate between providing portfolio protection (Tail Risk Hedging vs greater Portfolio Diversification) hit colossal proportions earlier in the year with a twitter spat between Nassim Nicholas Taleb, author of Black Swan and involved in Universa Investments, and Cliff Asness, a pioneer in quant investing and founder of AQR.

I provide a summary of their contrasting perspectives to portfolio protection as outlined in a Bloomberg article in this Post. There are certainly some important learnings and insights in contrasting their different approaches.

The Post also covered a PIMCO article, Hedging for Different Market Environments.

A key point from the PIMCO article is that not one strategy can be effective in all market environments. This is an important observation.

Therefore, maintaining an array of diversification strategies is preferred, PIMCO suggest “investors should diversify their diversifiers”.

They provide the following Table, which outlines an array of “Portfolio Protection” strategies.

In Short, and in general, Asness is supportive of correlation based like hedging strategies (Trend and Alternative Risk Premia) and Taleb the Direct Hedging approach.

From the Table above we can see in what type of market environment each “hedging” strategy is Most Effective and Least Effective.

For balance, more on the AQR perspective can be found here.

You could say I have a foot in both camps and are pleased I do not have a twitter account, as I would likely be in the firing line from both Asness and Taleb!

To conclude

I think we can all agree that fixed income is going to be less of a portfolio diversifier in future and produce lower returns in the future relative to the last 10-20 years.

This is an investment portfolio challenge that must be addressed.

We should also agree that avoiding large market losses is vital in accumulating wealth and reaching your investment objectives, whether that is attaining a desired standard of living in retirement, ongoing and uninterrupted endowment, or meeting future Pension liabilities.

In my mind, staying still is not going to work over the next 5-10 years and the issues raised by the Institutional Investor.com article do need to be addressed. The path taken is likely to be determined by individual circumstances.

The achievements of the Yale Endowment are significant and well documented.

Their achievements can largely be attributed to the successful and bold management of their Endowment Funds.

They have been pioneers in Investment Management. Many US Universities and global institutions have followed suit or implemented a variation of the Yale’s “Endowment Model”.

Without a shadow of a doubt, those involved with Endowments, Foundations, Charities, and saving for retirement can learn some valuable investment lessons by reviewing the investment approach undertaken by Yale.

In fiscal 2019 the Yale Endowment provided $1.4 billion, or 32%, of the University’s $4.2 billion operating income.

To put this into context, the Yale Endowment 2019 Annual Report notes that the other major sources of revenues for the University were medical services of $1.1 billion (26%); grants and contracts of $824 million (20%); net tuition, room and board of $392 million (9%); gifts of $162 million (4%); and other income and transfers of $368 million (9%).

Spending from the Endowment has grown during the last decade from $1.2 billion to $1.4 billion, an annual growth rate of 1.5%.

The Endowment Fund’s payments have gone far and wide, including scholarships, Professorships, maintenance, and books.

Yale’s spending and investment policies provide substantial levels of cash flow to the operating budget for current scholars, while preserving Endowment purchasing power for future generations.

What a wonderful contribution to society, just think of the social good the Yale Endowment has delivered.

Yale’s Investment Policy

As highlighted in their 2019 Annual Report:

Over the past ten years the Endowment grew from $16.3 billion to $30.3 billion;

The Fund has generated annual returns of 11.1% during the ten-year period; and

The Endowment’s performance exceeded its benchmark and outpaced institutional fund indices.

In relation to Investment Objectives the Endowment Funds seek to provide resources for current operations and preserving purchasing power (generating returns greater than the rate of inflation).

This dictates the Endowment has a bias toward equity like investments. Yale note:

“The University’s vulnerability to inflation further directs the Endowment away from fixed income and toward equity instruments. Hence, more than 90% of the Endowment is targeted for investment in assets expected to produce equity-like returns, through holdings of domestic and international equities, absolute return strategies, real estate, natural resources, leveraged buyouts and venture capital.”

Accordingly, Yale seeks to allocate over the longer term approximately one-half of the portfolio to illiquid asset classes of leverage buyouts, venture capital, real estate, and natural resources.

This is very evident in the Table below, which presents Yale’s asset allocation as at 30 June 2019 and the US Educational Institutional Mean allocation.

This Table appeared in the 2019 Yale Annual Report, I added the last column Yale vs the Educational Institutional Mean.

Yale University

Educational Institution Mean

Yale vs Mean

Absolute Return

23.2%

20.6%

2.6%

Domestic Equity

2.7%

20.8%

-18.1%

Foreign Equity

13.7%

21.9%

-8.2%

Leverage Buyouts

15.9%

7.1%

8.8%

Natural Resources

4.9%

7.7%

-2.8%

Real Estate

10.1%

3.4%

6.7%

Venture Capital

21.1%

6.6%

14.5%

Cash and Fixed Income

8.4%

11.9%

-3.5%

100%

100%

Non-Traditional Assets

75.2%

45.4%

29.8%

Traditional Assets

24.8%

54.6%

The Annual Report provides a comment on each asset class and their expected risk and return profile, an overview of how Yale manage the asset classes, historical performance, and future longer-term risk and return outlook.

High Allocation to Non-Traditional Assets

As can be seen in the Table above Yale has a very low allocation to traditional asset classes (domestic equities, foreign equities, cash and fixed income), and a very high allocation to non-traditional assets classes, absolute returns, leverage buyouts, venture capital, real estate, and natural resources.

This is true not only in an absolute sense, but also relative to other US Educational Institutions. Who in their own right have a high allocation to non-traditional asset classes, 45.4%, but almost 30% lower than Yale.

“Over the last 30 years Yale has reduced their dependence on domestic markable securities by relocating assets to non-traditional assets classes. In 1989 65% of investments were in US equities and fixed income, this compares to 9.8% today.”

By way of comparison, NZ Kiwi Saver Funds on average have less than 5% of their assets invested in non-traditional asset classes.

A cursory view of NZ university’s endowments also highlights a very low allocations to non-traditional asset classes.

There can be good reasons why other investment portfolios may not have such high allocations to non-traditional asset classes, including liquidity requirements (which are less of an issue for an Endowment, Charity, or Foundation) and investment objectives.

Rationale for High Allocation to Non-Traditional Assets

Although it is well known that Yale has high allocations to non-traditional assets, the rationale for this approach is less well known.

The 2019 Yale Annual Report provides insights as to the rationale of the investment approach.

Three specific comments capture Yale’s rationale:

“The higher allocation to non-traditional asset classes stems from their return potential and diversifying power”

Yale is active in the management of their portfolios and they allocate to those asset classes they believe offer the best long-term value. Yale determine the mix to asset class based on their expected return outcomes and diversification benefits to the Endowment Funds.

“Alternative assets, by their very nature, tend to be less efficiently priced than traditional marketable securities, providing an opportunity to exploit market inefficiencies through active management.”

Yale invest in asset classes they see offering greater opportunities to add value. For example, they see greater opportunity to add value in the alternative asset classes rather than in Cash and Fixed Income.

“The Endowment’s long time horizon is well suited to exploit illiquid and the less efficient markets such as real estate, natural resources, leveraged buyouts, and venture capital.”

This is often cited as the reason for their higher allocation to non-traditional assets. As an endowment, with a longer-term investment horizon, they can undertake greater allocations to less liquid asset classes.

Sovereign wealth Funds, such as the New Zealand Super Fund, often highlight the benefit of their endowment characteristics and how this is critical in shaping their investment policy.

Given their longer-term nature Endowments are able to invest in less liquid investment opportunities. They will likely benefit from these allocations over the longer-term.

Nevertheless, other investment funds, such as the Australian Superannuation Funds, have material allocations to less liquid asset classes.

Therefore, an endowment is not a necessary condition to invest in non-traditional and less liquid asset classes, the acknowledgement of the return potential and diversification benefits are sufficient reasons to allocate to alternatives and less liquid asset classes.

In relation to the return outlook, the Yale 2019 Annual report commented the “Today’s actual and target portfolios have significantly higher expected returns than the 1989 portfolio with similar volatility.”

Smaller Endowments and Foundations are following Yale

In the US smaller Endowments and Foundations are adopting the investment strategies of the Yale Endowment model.

They have adopted an investment strategy that is more align with an endowment more than twice their size.

Portfolio size should not be an impediment to investing in more advanced and diversified investment strategies.

There is the opportunity to capture the key benefits of the Endowment model, including less risk being taken, by implementing a more diversified investment strategy. Thus, delivering a more stable return profile.

This is attractive to donors.

The adoption of a more diversified portfolio not only makes sense on a longer-term basis, but also given where we are in the economic and market cycle.

The value is in implementation and sourcing appropriate investment strategies.

In this Post, I outline how The Orange County Community Foundation (OCCF) runs its $400m investments portfolio like a multi-billion-dollar Endowment.

Diversification and Its Long-Term Benefits

For those interested, the annual report has an in-depth section on portfolio diversification.

This section makes the following key following points while discussing the benefits of diversification in a historical context:

“Portfolio diversification can be painful in the midst of a bull market. When investing in a single asset class produces great returns, market observers wonder about the benefits of creating a well-structured portfolio.”

“The fact that diversification among a variety of equity-oriented alternative investments sometimes fails to protect portfolios in the short run does not negate the value of diversification in the long run.”

“The University’s discipline of sticking with a diversified portfolio has contributed to the Endowment’s market leading long-term record. For the thirty years ending June 30, 2019, Yale’s portfolio generated an annualized return of 12.6% with a standard deviation of 6.8%. Over the same period, the undiversified institutional standard of 60% stocks and 40% bonds produced an annualized return of 8.7% with a standard deviation of 9.0%. “

“Yale’s diversified portfolio produced significantly higher returns with lower risk.”

There are also sections on Spending Policy and Investment Performance.

One of the key questions facing investors at the moment is whether inflation or deflation represents the bigger risk in the coming years.

Now more than ever, given the likely economic environment in the years ahead, investors need to consider all their options when building a portfolio for their future. This may mean a number of things, including: increasing diversification, investing in new or different markets, being active, and flexible to take advantage of unique opportunities as they arise.

Those portfolios overly reliant on traditional markets, such as equities and fixed income in particular, run the risk of failing to meet to their investment objectives over the next ten years.

Conundrum Facing Investors

A recent article by Alan Dunne, Managing Director, Abbey Capital, The Inflation-Deflation debate and its Implications for Asset Allocation, which recently appeared in AllAboutAlpha.com, clearly outlines the conundrum currently facing investors.

As the article highlights, one of the “key questions facing investors at the moment is whether inflation or deflation represents the bigger risk for the coming years. Economists are split on this….”

Following a detailed analysis of the current and likely future economic environment and potential influences on inflation or deflation (which is well worth reading) the article covers the Implications for Asset Allocations.

Inflation or Deflation: Implications for Asset Allocations

The article makes the following observations as far as asset class performance in different inflation environments, based on historical observations:

Deflation like in the 1930s, is negative for equities but positive for Bonds.

If inflation picks ups, or even stagflation, that would be negative for real returns on financial assets and real assets may be favoured.

They conclude: “the current uncertainty highlights the importance of holding diversified portfolios, with exposure to a range of traditional and alternative assets and strategies with the potential to deliver returns in different market environments.”

Current Environment

Abbey Capital anticipate greater co-ordination of policy between governments (fiscal policy) and central banks (monetary policy).

As they note, “many economists draw a parallel between the current scenario and the substantial increase in government debt during World War II. One of the consequences of higher debt levels is that we may see pressure on central banks to maintain interest rates at low levels and maintain asset purchases to ensure higher bond issuance is not disruptive for bond markets i.e. coordination of monetary and fiscal policies.”

I think this will be the case. The Bank of Japan has maintained a direct yield curve control policy for some time and the Reserve Bank of Australia has implemented a similar policy recently. Direct yield curve control is where the central bank will target an interest rate level for the likes of the 3-year government bond.

In the environment after World War II debt levels were brought back to more manageable levels by keeping interest rates low (a process known as financial repression).

From a government policy perspective, financial repression reduces the real value of debt over time. It is the most palatable of a number of options.

Financial repression is potentially negative for government bonds

With interest rates so low, and likely to remain low for some time given policies of financial repression the real return (after inflation) on many fixed income instruments and cash could be negative.

A higher level of inflation not only reduces the real return on bonds but potentially also reduces the diversification benefits of holding bonds in a portfolio with equities.

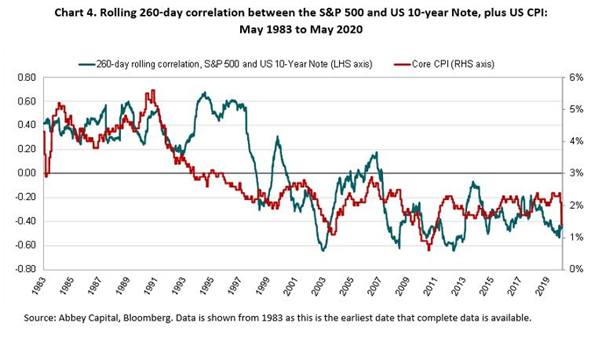

The diversification benefits of bonds in the traditional 60 / 40 equity-bond portfolio (Balanced Portfolio) has been a strong tail wind over the last 20 years.

The more recent low correlation between bonds and equities is evident in the Chart below, which was presented in the article.

The Chart also highlights that the relation of low correlation between equities and bonds, which benefits a Balanced Portfolio, has not always been present.

As can be seen in the Chart, in the 1980s, when inflation was a greater concern, inflation surprises were negative for both bonds and equities, they became positively correlated.

What should investors do?

“Investors are therefore left with the challenge of finding alternatives for government bonds, ideally with a low or negative correlation to equities and protection against possible inflation.”

The article runs through some possible investment solutions and approaches to meet the likely challenges ahead. I have outlined some of them below.

I think duration (interest rate risk) and credit can still play a role within a broad and truly diversified portfolio. Within credit this would likely involve expanding the universe to include the likes of high yield, securitised loans, private debt, inflation protections securities, and emerging market debt as examples.

The key and most important point is that a robust portfolio will be less reliant on tradition asset classes, traditional asset class betas, to drive investment return outcomes. This is likely to be vitally important in the years ahead.

Accordingly, investors will need to be more active, opportunistic, and maintain very broad and truly diversified portfolios. Not only within asset classes, such as the fixed income example provided above, but across the portfolio to include the likes of real assets and liquid alternatives.

Real assets

Abbey Capital comment that “Real assets such as property and infrastructure should provide protection against higher inflation for long-term investors but may not be attractive for investors valuing liquidity.”

Although the maintenance of portfolio liquidity is important, Real assets can play an important role within a robust portfolio.

For the different types of real assets, their investment characteristics, and likely performance and sensitivity to different economic environments, including economic growth, inflation, inflation protection, stagflation, and stagnation please see the Kiwi Investor Blog Post, Real Assets Offer Real Diversification. The extensive analysis has been undertake by PGIM.

Liquid Alternatives

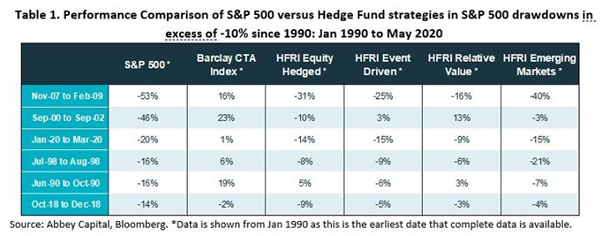

Abbey Capital provide a brief discussion on liquid alternatives with a focus on managed futures. Not surprisingly given their pedigree.

They provide the following Table which highlights the benefit of liquid alternatives and hedge funds at time of significant sharemarket declines (drawdowns).

Concluding Remarks

Being a managed futures manager, it is natural to be cautious of Abbey Capitals concluding remarks, being reminded of the Warren Buffet quote, “Never ask a barber if you need a haircut.”

Nevertheless, the Abbey Capital’s economic analysis and investment recommendations are consistent with a growing chorus, all singing from a similar song sheet. (Perhaps we could call this a “Barbers Quartet”!)

Without having an axe to grind, and in all seriousness, I have covered similar analysis and comments in previous Posts, the conclusions of which have a high degree of validity and should be considered, if not a purely from portfolio risk management perspective so as to understand any gaps in current portfolios for a number of likely economic environments.

The key and most important point is that robust portfolios will be less reliant on traditional asset classes, traditional asset class betas, to drive investment return outcomes.

Accordingly, investors will need to be more active, opportunistic, and maintain very broad and truly diversified portfolios

Therefore, it is hard to disagree with one of the concluding remarks by Abbey Capital “To account for the competing requirements in a portfolio of returns, low correlation to equities, liquidity and possible inflation protection, investors may need to build robust portfolios with a broader mix of assets and strategies.”

Other Reading

For those interested, previous Kiwi Investor Blog posts of relevance to the Abbey Capital article include:

Preparing your Portfolio for a period of Higher Inflation, this is the Post of most relevance to the current Post, and covers a recent Man article which undertook an analysis of the current economic environment and historical episodes of inflation and deflation.

Man conclude that although inflation is not an immediate threat, the likelihood of a period of higher inflation is likely in the future, and the time to prepare for this is now. Man recommends several investment strategies they think will outperform in a higher inflation environment.

It also includes analysis by PIMCO, where it is suggested to “diversify your diversifiers”.

Lastly, Sharemarket crashes – what works best in minimising losses, market timing or diversification, covers a research article by AQR, which concludes the best way to manage periods of severe sharemarket decline is to have a diversified portfolio, it is impossible to time these episodes. AQR evaluates the effectiveness of diversifying investments during sharemarket drawdowns using nearly 100 years of market data.

“The Bet” received considerable media attention following the 2017 Berkshire Hathaway shareholder letter in 2018.

To recap, the bet was between Warren Buffet and Protégé Partners, who picked five “funds of fund” hedge funds they expected would outperform the S&P 500 Index over the 10-year period ending December 2017. Buffet took the S&P 500 to outperform.

The bet was made in December 2007, when the market was reasonably expensive and the Global Financial Crisis (GFC) was just around the corner.

Buffet won. The S&P 500 easily outperformed the Hedge Fund selection over the 10-year period.

There are some astute investment lessons to be learnt from this bet, which are very clearly presented in this AllAboutAlpha article, A Rhetorical Oracle, by Bill Kelly.

Before reviewing these lessons, I’d like to make three points:

I’d never bet against Buffet!

I would not expect a Funds of Funds Hedge Fund to consistently outperform the S&P 500, let alone a combination of five Funds of Funds.

Most if not all, investor’s investment objective(s) is not to beat the S&P 500. Investment Objectives are personal and targeted e.g. Goal Based Investing to meet future retirement income or endowments

This is not to say Hedged Funds should not form part of a truly diversified investment portfolio. They should, as should other alternative investments.

Nevertheless, I am unconvinced Hedge Fund’s role is to provide equity plus like returns.

One objective in allocating to alternatives is to add return sources that make money on average and have low correlation to equities. Importantly, diversification is not the same thing as “hedging” a portfolio

Now, I have no barrow to push here, except advocating for the building of robust investment portfolios consistent with meeting your investment objectives. The level of fees also needs to be managed appropriately across a portfolio.

In this regard and consistent with the points in the AllAboutAlpha article:

Having a well-diversified portfolio is paramount and results in better risk-adjusted returns over time.

Being diversified across non-correlated or low correlated investments is important, leading to better risk-adjusted outcomes.

Adding low correlated investments to an equities portfolio, combined with a disciplined rebalancing policy, will likely add value above equities over time.

The investment focus should be on reducing portfolio volatility through true portfolio diversification so that wealth can be accumulate overtime.

Minimising loses results in higher returns over time. A portfolio that falls 50%, needs to gain 100% to get back to the starting capital. This means as equity markets take off a well-diversified multi-asset portfolio will not keep up. Nevertheless, the well diversified portfolio will not fall as much when the inevitable crash comes along.

It is true that equities are less risky over the longer term. Nevertheless, not many people can maintain a fully invested equities portfolio, given the wild swings in value (as highlighted by Buffett in his Shareholder Letter, Berkshire can fall 50% in value).

100% in equities is often not consistent with meeting one’s investment objectives. Buffet himself has recommended the 60/40 equities/bond allocation, with allocations adjusted around this target based on market valuations.

I am unlikely to ever suggest to be 100% invested in equities for the very reason of the second point in the article, as outlined below.

Investment Behavioural aspects.

How many clients would have held on to a 100% equity position during the high level of volatility experienced over the last 10-12 years, particularly in the 2008 – 2014 period. Not many I suspect. This would also be true of the most recent market collapse in 2020.

The research is very clear, on average investors do not capture the full value of equity market returns over the full market cycle, largely because of behavioural reasons.

A well-diversified portfolio, that lowers portfolio volatility, will assist an investor in staying the course in meeting their investment objectives.

An allocation to alternative strategies, including a well-chosen selection of Hedge Funds, will result in a truly diversified Portfolio, lowering portfolio volatility. See an earlier Post, the inclusion of Alternatives has been an evolutionary process, not a revolution.

Staying the course is the biggest battle for most investors. Therefore, take a longer-term view, focus on customised investment objectives, and maintain a truly diversified portfolio.

This will help the psychological battle as much as anything else.

I like this analogy of using standard deviation of returns as a measure of risk. It captures the risks associated with a very high volatile investment strategy such as being 100% invested in equities:

“A stream may have an average depth of five feet, but a traveler wading through it will not make it to the other side if its mid-point is 10 feet deep. Similarly, an overly volatile investing strategy may sink an investor before she gets to reap its anticipated rewards.”

Based on the US Department of Labor (DOL) guidance US retirement plans, Defined Contribution (DC), can include certain private equity strategies into diversified investment options, such as target date or balanced funds, while complying with ERISA (laws that govern US retirement plans).

This is anticipated to result in better outcomes for US investors.

It is also anticipated to provide a further tailwind for the Private Equity sector which is expected to experience significant growth over the decade ahead, as outlined

Private equity investments have long been incorporated in defined benefit (DB) plans, DC plans, 401(k) retirement plans similar to KiwiSaver Funds offered in New Zealand and superannuation funds around the world, have mainly steered away from incorporating Private Equity in their plans due to litigation concerns.

By way of summary, the DOL provides the following guidance. In adding a private equity allocation, the risks and benefits associated with the investment should be considered.

In making this determination, the fiduciary should consider:

whether adding the asset allocation fund with a private equity component would offer plan participants the opportunity to invest their accounts among more diversified investment options within an appropriate range of expected returns net of fees and the diversification of risks over a multi-year period;

whether using third-party investment experts as necessary or managed by investment professionals have the capabilities, experience, and stability to manage an asset allocation fund that includes private equity effectively;

limit the allocation to private equity in a way that is designed to address the unique characteristics associated with such an investment, including cost, complexity, disclosures, and liquidity, and has adopted features related to liquidity and valuation.

It is worth noting that the SEC (U.S. Securities and Exchange Commission) has adopted a 15% limit on investments into illiquid assets by US open-ended Funds such as Mutual Funds (similar to Unit Trusts) and ETFs.

In addition, the DOL suggests consideration should be given to the plan’s features and participant profile e.g. ages, retirement age, anticipated employee turnover, and contribution and withdrawal patterns.

The DOL letter outlines a number of other appropriate considerations, such as Private Equity to be independently valued in accordance with agreed valuation procedures.

It is important to note the guidance is in relation to Private Equity being offered as part of a multi-asset class vehicle structure as a custom target date, target risk, or balanced fund. Private Equity cannot be offered as a standalone investment option.

It is estimated that as much as $400 billion of new assets could be assessed by Private Equity businesses as a result of the DOL guidance, as outlined in this FT article.

Increased innovation is expected, more Private Equity vehicles that offer lower fees and higher levels of liquidity will be developed.

A number of Private Equity firms are expected to benefit.

For example, Partners Group and Pantheon stand to benefit, see below for comments, they launched Private Equity Funds with daily pricing and liquidity in 2013. These Funds were designed for 401(k) plans.

As you would expect, they reference research by the Georgetown Center for Retirement Initiatives which concludes that including a moderate allocation to private equity in a target-date fund could increase the participant’s annual retirement income by at least 6%.

They also comment, private markets provide valuable diversification in an investment portfolio in light of a shrinking public markets sector that has seen the number of US publicly-traded companies decline by around 50% since 1996.

This observation is consistent with one of the key findings from the recently published CAIA Association report, The Next Decade of Alternative Investments: From Adolescence to Responsible Citizenship.

The DOL guidance will provide another tailwind for Private Equity.

For those interested, this paper by the TIAA provides valuable insights into the optimal way of building an allocation to Private Equity within a portfolio.

Potentially significant Industry Impact

The DOL Letter has been well received by industry participants as outlined in this P&I article.

The article stresses that the guidance will help quell some sponsor’s litigation fears and with a good prudent process Private Equity can be added to a portfolio.

The DOL believes the guidance letter “helps level the playing field for ordinary investors and is another step by the department to ensure that ordinary people investing for retirement have the opportunities they need for a secure retirement.”

The DOL Letter is in response to a Groom Law Group request on behalf of its clients Pantheon Ventures and Partners Group, who have developed private equity strategies that can accommodate DC plans. The DOL specifically referenced Partners Groups Funds and commented their Private Equity Funds are “designed to be used as a component of a managed asset allocation fund in an individual account plan.”

Partners Group said in a statement that the DOL has taken “a major step toward modernizing defined contribution plans and providing participants with a more secure retirement. At a time when working families are struggling to save, this guidance gives fiduciaries the certainty they need to finally provide main street Americans access to the same types of high-performing, diversifying investments as wealthy and large institutional investors, all within the safety of their 401(k) plans.”

Further comments by Partner Group can be found here.

Avoiding large market losses is vital to accumulating wealth and reaching your investment objectives, whether that is attaining a desired standard of living in retirement or an ongoing and uninterrupted endowment.

The complexity and different approaches to providing portfolio protection (tail-risk hedging) has been highlighted by a recent twitter spat between Nassim Nicholas Taleb, author of Black Swan, and Cliff Asness, a pioneer in quant investing.

PIMCO provide a brief summary of different strategies and their trade-offs in diversifying a Portfolio.

They outline four approaches to diversify the risk from investing in sharemarkets (equity risk).

In addition to tail risk hedging, the subject of the twitter spat above between Taleb and Asness, and outlined below, PIMCO consider three other strategies to increase portfolio diversification: Long-term Fixed Income securities (Bonds), managed futures, and alternative risk premia.

PIMCO provide the following Graph to illustrate the effectiveness of the different “hedging” strategies varies by market scenario.

As PIMCO note “it’s important for investors to know in what types of environments each strategy is more likely to work and in what environments each are likely to be less effective.”

As they emphasise “not every type of risk-mitigating strategy can be expected to work in every type of market sell-off.”

A brief description of the diversifying strategies is provided below:

Long Bonds – holding long term (duration) high quality government bonds (e.g. US and NZ 10-year or long Government Bonds) have been effective when there are sudden declines in sharemarkets. They are less effective when interest rates are rising. (Although not covered in the PIMCO article, there are some questions as to their effectiveness in the future given extremely low interest rates currently.)

Managed Futures, or trend following strategies, have historically performed well when markets trend i.e. there is are consistent drawn-out decline in sharemarkets e.g. tech market bust of 2000-2001. These strategies work less well when markets are very volatile, short sharp movements up and down.

Alternative risk premia strategies have the potential to add value to a portfolio when sharemarkets are non-trending. Although they generally provide a return outcome independent of broad market movements they struggle to provide effective portfolio diversification benefits when there are major market disruptions. Alternative risk premia is an extension of Factor investing.

Tail risk hedging, is often explained as providing a higher degree of reliability at time of significant market declines, this is often at the expense of short-term returns i.e. there is a cost for market protection.

A key point from the PIMCO article is that not one strategy can be effective in all market environments.

Therefore, maintaining an array of diversification strategies is preferred “investors should “diversify their diversifiers””.

It is well accepted you cannot time markets and the best means to protect portfolios from large market declines is via a well-diversified portfolio, as outlined in this Kiwi Investor Blog Post found here, which coincidentally covers an AQR paper. (The business Cliff Asness is a Founding Partner.)

A summary of the key differences in perspectives and approaches between Taleb and Asness as outlined in Aaron Brown’s Bloomberg’s article, Taleb-Asness Black Swan Spat Is a Teaching Moment.

My categorisations

Asness

Taleb

Defining a tail event

Asness refers to the worst events in history for investors, such as the 5% worst one-month returns for the S&P 500 Index.

Research by AQR shows that steep declines that last three months or less do little or no damage to 10-year returns.

It is the long periods of mediocre returns, particularly three years or longer, that damages longer term performance.

Taleb defines “tail events” not by frequency of occurrence in the past, but by unexpectedness. (Black Swan)

Therefore, he is scathing of strategies designed to do well in past disasters, or based on models about likely future scenarios.

Different Emphasis

The emphasis is not only on surviving the tail event but to design portfolios that have the highest probability of generating acceptable long-term returns. These portfolios will give an unpleasant experience during bad times.

Taleb prefers tail-risk hedges that deliver lots of cash in the worst times. Cash provides a more pleasant outcome and greater options at times of a crisis.

Investors are likely facing a host of challenges at the time of market crisis, both financial and nonfinancial, and cash is better.

Different approaches

AQR strategies usually involve leverage and unlimited-loss derivatives.

Taleb believes this approach just adds new risks to a portfolio. The potential downsides are greater than the upside.

Costs

AQR responds that Taleb’s preferred approaches are expensive that they don’t reduce risk.

Also, the more successful the strategy, the more expensive it becomes to implement, that you give up your gains over time e.g. put options on stocks

Taleb argues he has developed methods to deliver cash in crises that are cheap enough that they actually add to long-term returns while reducing risk.

Investor behaviours

Asness argues that investors often adopt Taleb’s like strategies after a severe market decline. Therefore, they pay the high premiums as outlined above. Eventually, they get tire of the paying the premiums during the good times, exit the strategy, and therefore miss the payout on the next crash.

Taleb emphasises the bad decisions investors make during a market crisis/panic, in contrast to AQR’s emphasis on bad decisions people make after the market crisis.

In a well-diversified portfolio, when one asset class is performing extremely well (like global equity markets), the diversified portfolio is unlikely to keep pace.

In these instances, the investor is likely to regret that they had reduced their exposure to that asset class in favour of greater portfolio diversification.

This is a key characteristic of having a well-diversified portfolio. On many occasions, some part of the portfolio will be “underperforming” (particularly relative to the asset class that is performing strongly).

Nevertheless, stay the course, over any given period, diversification will have won or lost but as that period gets longer diversification is more and more likely to win.

True diversification comes from introducing new risks into a portfolio. This can appear counter-intuitive. These new risks have their own risk and return profile that is largely independent of other investment strategies within the Portfolio. These new risks will perform well in some market environments and poorly in others.

Nevertheless, overtime the sum is greater than the parts.

The majority of the above insights are from a recent Willis Tower Watson (WTW) article on Diversification, Keep Calm and Diversify.

The article provides a clear and precise account of portfolio diversification. It is a great resource for those new to the topic and for those more familiar.

WTW conclude with the view “that true diversification is the best way to achieve strong risk adjusted returns and that portfolios with these characteristics will fare better than equities and diversified growth funds with high exposures to traditional asset classes in the years to come.”

Playing with our minds – Recent History

As the WTW article highlights the last ten-twenty years has been very unusual for both equity and bond markets have delivered excellent returns.

This is illustrated in the following chart they provide, the last two rolling 10-year periods have been periods of exceptional performance for a Balanced Portfolio (60%/40% equity/fixed income portfolio).

WTW made the following observations:

The last ten years has tested the patience of investors when it comes to diversification;

WTW believe investors will be better served going forwards by building robust portfolios that exploit a range of return drivers such that no single risk dominates performance. (In a Balanced Portfolio of 60% equities, equities account for over 90% of portfolio risk.)

They argue true portfolio diversification is achieved by investing in a range of strategies that have low and varying levels of sensitivity (correlation) to traditional asset classes and in some instances have none at all.

Other sources of return, and risks, include investing in investment strategies with low levels of liquidity, accessing manager skill e.g. active returns above a market benchmark are a source of return diversification, and diversifying strategies that access return sources independent of traditional equity and fixed income returns. These strategies are also lowly correlated to traditional market returns.

Sources of Portfolio Diversification

Hedge Funds and Liquid Alternatives

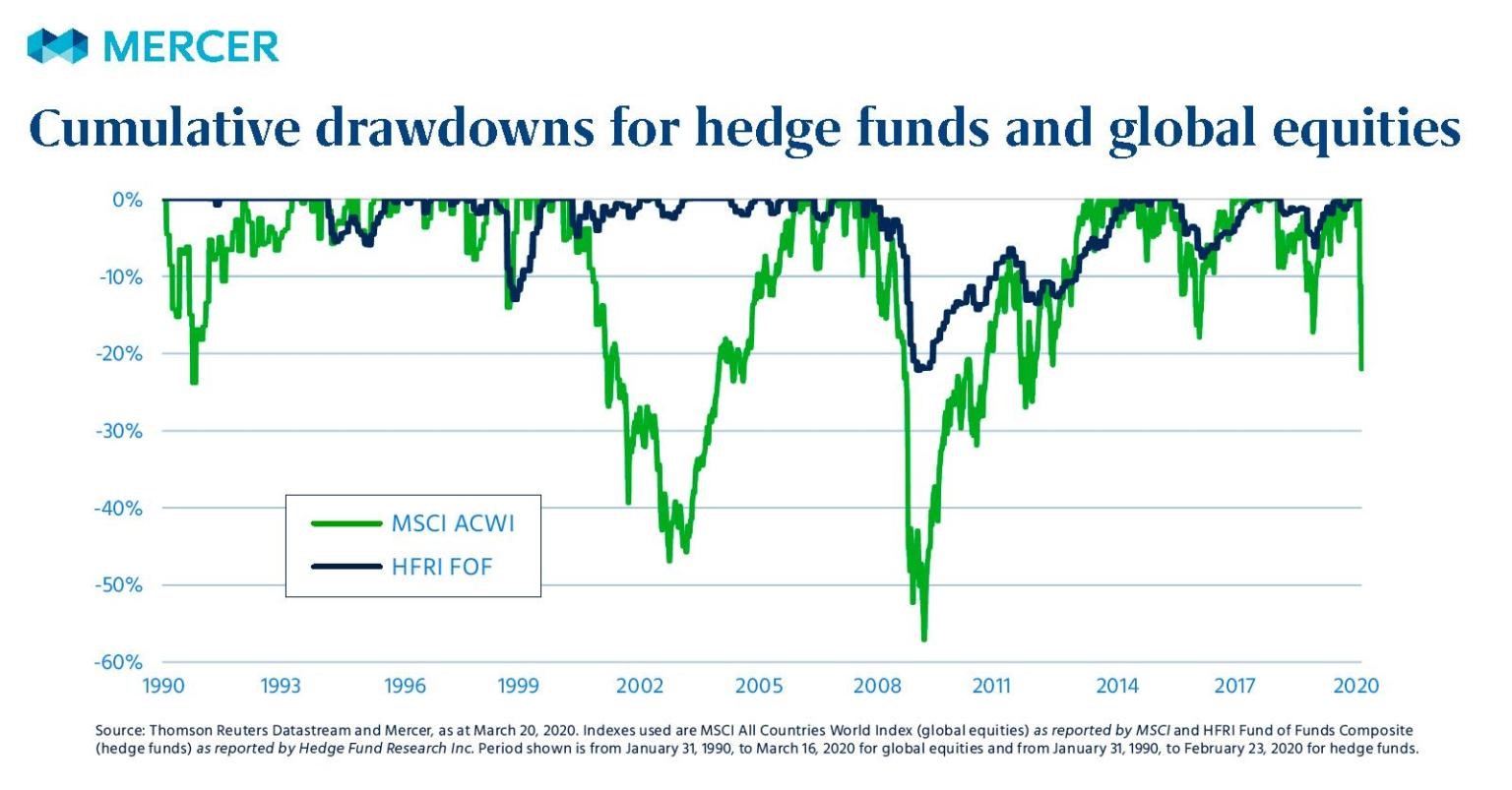

Hedge Funds and Liquid Alternatives are an example of diversifying strategies mentioned above. As outlined in this Post, covering a paper by Vanguard, they both bring diversifying benefits to a traditional portfolio.

It is worth highlighting that hedge fund and liquid alternative strategies do not provide a “hedge” to equity and fixed income markets.

Therefore they do not always provide a positive return when equity markets fall. Albeit, they do not decline as much at times of market crisis, as we have recently witnesses. Technically speaking their drawdowns (losses) are smaller relative to equity markets.

As evidenced in the Graph below provided by Mercer.

Private Markets

TWT also note there are opportunities within Private Markets to increase portfolio diversification.

There will be increasing opportunities in Private markets because fewer companies are choosing to list and there are greater restrictions on the banking sector’s ability to lend.

This is consistent with key findings of the recently published CAIA Association report, The Next Decade of Alternative Investments: From Adolescence to Responsible Citizenship.

The factors mentioned above, along with the low interest rate environment, the expected shortfall in superannuation accounts to meet future retirement obligations, and the maturing of emerging markets are expected to drive the growth in alternative investments over the decade ahead.

TWT expect to see increasing opportunities across private markets, including a “range from investments in the acquisition, development, and operation of natural resources, infrastructure and real estate assets, fast-growing companies in overlooked parts of capital markets, and innovative early-stage ventures that can benefit from long-term megatrends.”

Continuing the theme of lending where the banks cannot, they also see the opportunity for increasing portfolios with allocations to Private Debt.

WTW provided the following graph, source data from Preqin

Real Assets

In addition to Hedge Funds, Liquid Alternatives, and Private markets (debt and equity), Real Assets are worthy of special mention.

Real assets such as Farmland, Timberland, Infrastructure, Natural Resources, Real Estate, TIPS (Inflation Protected Fixed Income Securities), Commodities, Foreign Currencies, and Gold offer real diversification benefits relative to equities and fixed income in different macro-economic environments, such as low economic growth, high inflation, stagflation, and stagnation.

These are a conclusive findings of a recent study by PGIM. The PGIM report on Real Assets can be found here. I provided a summary of their analysis in this Post: Real Assets offer real diversification benefits.

Conclusion

To diversify a portfolio it is recommended to add risk and return sources that make money on average and have a low correlation to equities.

Diversification should be true both in normal times and when most needed: during tough periods for sharemarkets.

Diversification is not the same thing as a hedge. Although “hedges” make money at times of sharemarket crashes, there is a cost, investments with better hedging characteristics tend to do worse on average over the longer term. Think of this as the cost of “insurance”.

Therefore, alternatives investments, as outlined above, are more compelling relative to the traditional asset classes in diversifying a portfolio, they provide the benefits of diversification and on average over time their returns tend to keep up with sharemarket returns.

Importantly, investing in more and more traditional asset classes does not equal more diversification e.g. listed property. As outlined in this Post.

As outlined above, we want to invest in a combination of lowly correlated asset classes, where returns are largely independent of each other. A combination of investment strategies that have largely different risk and return drivers.