We need to change the conversation on investment management fees. The debate on fees needs to be based on facts rather than myths. Despite often being framed in this way, the debate on investment management fees is not black versus white.

What matters is not the fee level, but the manager’s ability to deliver a satisfactory outcome to investors after fees. Either way, it is no good paying high fees or the lowest possible fees if your investment objectives have not been achieved. Therefore, amongst the key questions to ask are, are you satisfied with the investment outcomes after the fees you have paid? – have your investment objectives or retirement goals been achieved?

After fee returns are important. Therefore, higher fee investment strategies should not necessarily be avoided if they can assist in meeting your investment objectives. In the current investment environment, the use of higher fee investment strategies may be necessary to achieve your investment objectives.

Therefore, Investors should focus on given the investment outcomes have I minimised the fees paid.

In my mind, this would be consistent with the FMA’s value for money focus. (FMA is New Zealand’s Regulatory)

At the same time, fees should not be the overriding concern and investors must analyse fees in the overall context of managing their portfolios appropriately.

Investment management fee Myths

The 5 most common myths about investment management fees are:

- Fees should be as low as possible

- Incentive fees are always better than fixed fees

- High water marks always help investors

- Hedge Funds are where the alpha is. They deserve their high fees

- You can always separate alpha from beta, and pay appropriate fees for each

This paper, Five Myths About Fees, address the above myths in detail.

Although all the myths are important, the myth that fees should be as low as possible probably resonates most with investors.

Investment management fees for active management are higher than index management and involve a wealth transfer from the investor to the investment manager. This is a fact.

However, the paper is clear, investors should look to maximise excess returns (they term alpha) after fees. Another way of looking at this, for a given level of excess returns, fees should be minimised. This is an important concept when considering the discussion below around broadening the discussion on fees.

The paper also notes, investors should pay higher fees to those managers that are more consistent. For example, if two managers provide the same level of excess return, but one does so by taking less risk, investors should pay higher fees to this manager (the manager who achieves the same excess return but with lower risk – technically speaking, this is the manager with the higher information ratio).

In summary, the take-outs on the myth fees should be as low as possible:

- Fees must remain below expected excess returns e.g., a manager that charges active fees but only delivers enhanced index returns should be avoided.

- Managers who consistently add value warrant higher fees.

In relation to do managers add value, see this Post, Challenging the Conventional Wisdom of Active Management.

The paper on the five fee myths is wide ranging. It also provides insights into the key elements of the fee negotiation game and determining the conditions under which higher fees should be paid.

Key conclusions from the article, particularly after addressing Myth 4 & 5:

- most investment strategies offer a combination of cheaply accessible market index returns (beta) and active management excess returns (alpha). While many institutional investors look to separate beta and alpha for most investors this is too limiting and difficult. Many talented investment managers appear in investment strategies which include both beta and excess returns (alpha).

- Investors should consider fees before deciding on an investment strategy, not look at an investment strategy and then consider fees.

- At the same time, fees should not be the overriding concern.

- High fee investment strategies are worthwhile if they deliver sufficient return and lower risk.

- Investors must analyse fees in the overall context of managing their portfolios appropriately.

A framework for Changing the discussion on fees

Despite it often framed this way, the debate on fees is not black versus white.

From this respective, understanding the disaggregation of investment returns can help in broaden the debate on fees and also help determine the appropriateness of fees being paid.

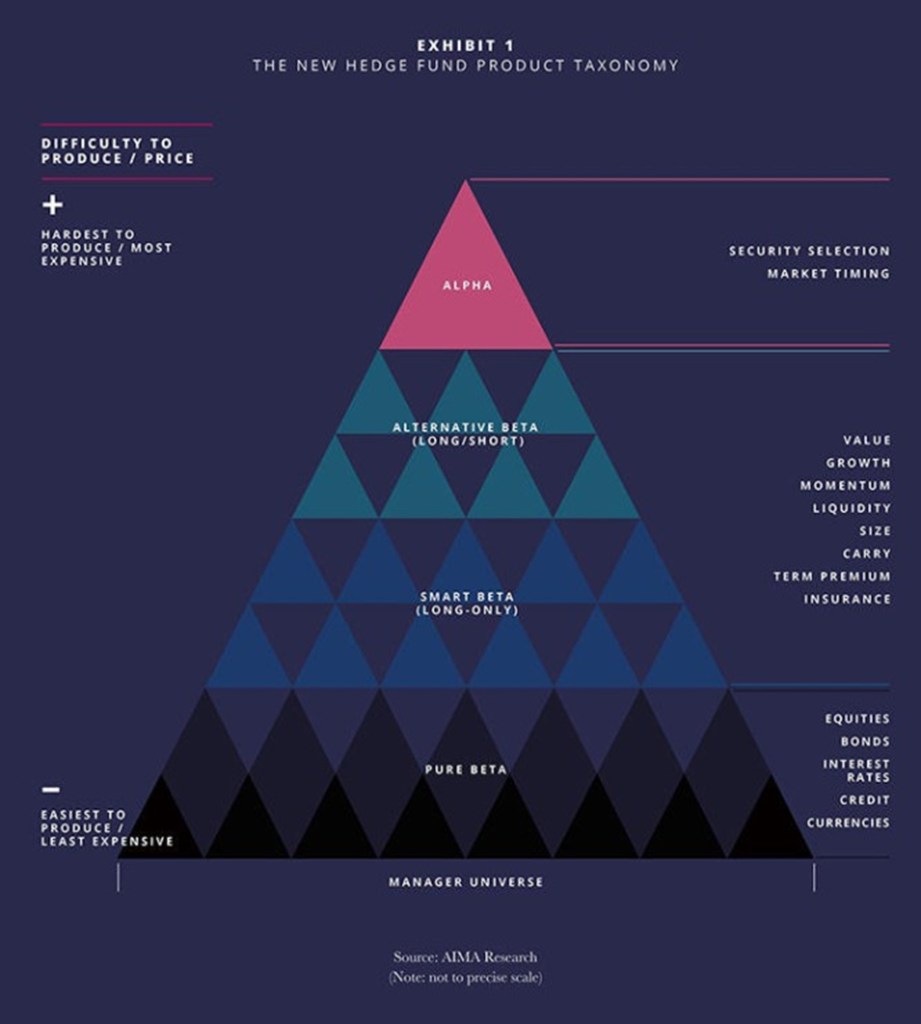

From a broad view, investment returns can be disaggregated in to the following three parts:

- Market beta. Think equity market exposures to the NZX50 or S&P 500 indices (New Zealand and America equity market exposures respectively). Market Index funds provide market beta returns i.e. they track the returns of the market e.g. S&P 500 and NZX50. Beta is cheap, as low as 0.01% for large institutional investors.

- Factor betas and Alternative hedge fund beta exposures. Of the sources of investment returns these are a little more ambiguous and contentious than the others. This mainly arises from use of terminology and the number of investable factors that are rewarding. My take is as follows, Factor betas and Alternative hedge fund beta fit between market betas (above) and alpha (explained below).

- Factor Beta exposures. These are the factor exposures for which I think there are a limited number. The common factors include value, momentum, low volatility, size, quality/profitability, carry. They are often referred to as Smart beta.

- Alternative hedge fund betas. Many hedge fund returns are sourced from well understood investment strategies. Therefore, a large proportion of hedge fund returns can be explained by common hedge fund risk exposures, also known as hedge fund beta or alternative risk premia or risk premia. Systematic, or rule based, investment strategies can be developed to capture a large portion of hedge fund returns that can be attributed to a hedge fund strategy (risk premia) e.g. long/short equity, managed futures, global macro, and arbitrage hedge fund strategies. The alternative hedge fund betas do not capture the full hedge fund returns as a portion can be attributed to manager skill, which is not beta and more easily accessible, it is alpha.

- Alpha is what is left after all the betas. It is manager skill. Alpha is a risk adjusted measure. In this regard, a manager outperforming an index is not necessarily generating alpha. The manager may have taken more risk than the index to generate the excess returns and/or they may have an exposure to one of the factor betas or hedge fund betas which could have been captured more cheaply to generate the excess return. In short, what is often claimed as alpha is often explained by a factor or alternative hedge fund beta outlined above. Albeit, there are some managers than can deliver true alpha. Nevertheless, it is rare.

These broad sources of return are captured in the diagram below, provided in a hedge fund industry study produced by the AIMA (Alternative Investment Management Association).

The disaggregation of return framework is useful for a couple of important investment considerations. We can use this framework to determine:

- Appropriateness of the fees paid. Obviously for market beta low fees are paid e.g. index fund fees. Fees increase for the factor betas and then again for the alternative hedge fund betas. Lastly, higher fees are paid to obtain alpha, which is the hardest to produce.

- If a manager is adding value – this was touched on above. Can a manager’s outperformance, “alpha”, be explained by “beta” exposures, or is it truly unique and can be put down to manager skill.

The consideration of this framework is consistent with the observations from the article above covering the 5 myths of Investment Management Fees.

Lastly, personally I think a well-diversified portfolio would include an exposure to all of the return sources outlined above, at the very least.

Many institutional investors understand that true portfolio diversification does not come from investing in many different asset classes but comes from investing in different risk factors. See More Asset Classes Does not Equal More Diversification.

From this perspective, the objective is to implement a portfolio with exposures to a broad set of different return and risk outcomes.

Please read my Disclosure Statement

For Outsourced Chief Investment Officer (OCIO) and investment consulting services please see here.

Global Investment Ideas from New Zealand. Building more Robust Investment Portfolios.

YES, YES, YES

And yet MBIE has just changed the default KiwiSaver providers based on “level of fees” and “service provided” and ignored performance. Doh.

LikeLike

YES & NO.

The bigger question is can investors identify active managers (beforehand) that provide “true” alpha? Then the fee conversation comes into it, for do the investors get the benefit of this alpha?

Your thoughts?

LikeLike

Yes. The ability of managers to add value is referenced to the Post, Challenging Conventional Wisdom of Active Management. Also, the alternative betas and hedge fund betas are known to add value after fees, so these need to be considered too, not just true alpha.

LikeLike

In the Challenging Conventional Wisdom of Active Management paper, they do a reasonable job of presenting both sides of the argument.

Yet, there is more disconfirming evidence on both sides of the research they present, e.g. You mentioned Kosowski, Timmerman, Wermer and White(2006). However, Blake, Caulfied, Ioannidis and Tonks( 2014) and Riley (2019) found different conclusions. Same as the active share polarising debate. (My belief is you can prove anything, it’s the disconfirming evidence that we should be looking at)

Then value-added for the fund manager is separate from investors gaining the benefit of this value ( Berk/Green 2005). So that’s where fees come into it. Then it is identifying these “skilled” managers beforehand. This is a considerable barrier for retail investors to overcome. Institutions may have a better advantage than retail, yet not sure how much. ( Goyal & Wahal 2008)

LikeLike

Hi, fantastic comment. In my mind, for the retail investor, in addition to getting good advice, the focus should be on what you want to achieve in retirement, rather than paying the lowest possible fees. Achieving a desired standard of living in retirement is the true measure of success. A focus on fees may not lead to achieving your retirement goals, particularly in the current investment environment. After fee outcomes are important, especially for retail investors. From this perspective, the inclusion of higher fee investment strategies may be necessary in achieving desired retirement goals.

LikeLike

My understanding is these are 2 separate conversations. So the difference between tactics vs vision/purpose.

So the fee conversation links to the active vs smart beta vs passive funds debate which is a tactic (Similarly, another tactic is property vs shares). I think retail investors should be looking for low fees in their fund strategy.

The purpose/vision is incorporated from the “value” of advice which is very different. This brings up questions like: “What is a meaningful retirement to you?” “What do you want to achieve?” “Why is money important to you?” Or the George Kinder questions.

This is what investors should be paying( maybe a lot for…) from financial advisers.

Thus from this specific purpose, the investor can make tactical decisions that work for them.

There have been measurements of advice value, e.g. Vanguard- Advisor Alpha, Morningstar-Gamma. However, these measurements are very arbitrary.

Thanks for the replies. I am enjoying the conversation.

LikeLiked by 1 person

Hi, yes, they can be viewed as separate discussions. Absolutely agree with your comments in relation to the value of seeking advice and the key source of value an Adviser can deliver and focus on. With regards to fees, I think rather than being a tactic it is about most efficiently using fees to access the different sources of return to achieve investment and retirement goals. This is not about minimising fees, but minimising fees for the investment outcomes you are trying to achieve. The focus on fees may lead to investors not achieving their investment goals, and the cost of this is very high.

LikeLike

That makes sense about fees to investment outcomes. I am coming from a retail investor point of view. So here are additional comments.

1. This is where in general lower fees are linked to higher returns( vanguard/ Morningstar research ) Nanigan( 2018) finds the active/ passive funds a moot point due to a competitive low fees active fund has similar outcomes to passive funds.

2. I agree with smart beta( alt beta). However, do you get net alpha?. Grey( alpha architect) comments on mixed research( academic vs companies that promote factor investing funds) with trading costs on value/ momentum. Then (as you mentioned) are active managers producing alpha or coat-tailing on factor risk exposure. Retail investors will be unaware of this.

3. Not sure about alternative hedge( I don’t understand the product). Can the retail investor have access to the product and then pick the superior manager beforehand? Or, for that matter, Institutions?.

Portnoy( investor’s paradox 2014) comments on Dewaele et a( 2011) where the difficulty on funds of hedge funds picking a manager. They concluded 5% of professional fund of fund managers show skill. (net alpha). You would have better insights into institutional investing.

4. Dispersion of outcome. Active funds, Alternative beta & alternative hedge, will have a wider dispersion of outcomes. So then, can the average investor( or even institutions ) stay the course? Over underperformance periods, e.g. value the last decade.

Overall are we making it too complicated for our own good? Simple ( or via a algorithm) can be better than complex( Haldane 2012).

I think it is to acknowledge there are many shades of grey and not to get too dogmatic about any ideas/beliefs.

LikeLike

I agree it’s important to focus on investment outcomes after considering the fees paid.

LikeLike

I agree that fees have to be viewed in context. It’s returns net of fees that really matter, rather than the explicit fee level itself.

It should be highlighted more often, that ‘active managers’ are often capturing factor betas rather than delivering real alpha, usually for a very hefty fee. Perhaps this explains the general correlation between higher-cost investments under-performing lower cost ones over time.

LikeLiked by 1 person