Likely poor performing investment managers are relatively easy to identify. Great fund managers much more difficult to identify.

Good performing managers who can consistently add value over time can be identified. Albeit, a well-developed and disciplined investment research process is required.

Those managers that consistently add value are likely to be found regularly in the second quartile of peer analysis. They are neither the best nor the worst performing manager but over time consistently add value over a market index or passive investment. They are not an average manager.

These are key insights I have developed from just under 30 years of researching and collaborating with high calibre and talented investment professionals.

More importantly, modern day academic research is supportive of this view. The conventional wisdom of active management is being challenged, as highlighted in a previous Post.

The author, John Paterson, of this analysis was interviewed in a i3 article.

The key points of Peterson’s analysis and emphasized in the i3 article:

Many of the studies into the ability of active managers to consistently outperform are inherently flawed.

Most of these studies merely confirm that financial markets are not static, therefore they do not say anything about manager performance.

“The failure to find repeated top quartile performance in these ‘tests of manager consistency’ simply reflects the reality that markets are not Static, and says nothing about the existence, or otherwise, of manager consistency.”

The key flaw is that many of the studies on active management focus on the performance of only the top performing managers: whether top quartile performers are able to repeat their efforts from one period to the next.

A wider view of manager performance should be considered, all quartiles should be assessed to determine whether manager performance is random or not.

Those managers that that consistently achieved above average returns are more likely to be found in the second or third quartiles.

In the i3 interview, Paterson discusses more about the results of their research:

“Someone who consistently outperforms doesn’t necessarily look like a top quartile manager. They are more likely to be found in the second quartile,”.

The following comment is also made:

“Most asset managers intuitively know this, because markets are cyclical and if you do something that shoots the lights out in one period, it is likely to do the complete opposite in another period.”

The Australian Experience

Paterson’s analysis also found “Across the studies analysed, it was found that there is very strong evidence that investment managers available to Australian superannuation funds do perform consistently.”

Lastly Paterson comments “And experience tells us that super funds with more active managers have done better than those with largely passive mandates, and often at a lower level of volatility.”

Concluding Remarks

As I have previously Posted, there are a wide range of reasons for choosing an alternative to passive investing over and above the traditional industry debate that focuses on whether active management can outperform.

Other reasons for considering an alternatives to a passive index include no readily replicable market index exists, imbedded inefficiency within the Index, and available indices are unsuitable in meeting an investor’s objectives (e.g. Defined Pension Plans).

The decision to choose an alternative to passive investing varies across asset classes and investors.

Therefore, the traditional active versus passive debate needs to be broadened.

The article by Warren and Ezra, covered in a previous Post, When Should Investors Consider an Alternative to Passive Investing?, seeks to reconfigure and broaden the active versus passive debate.

They provide five reasons why investors might consider alternatives to passive management.

In doing so they provide examples of circumstances under which an alternative to passive management might be preferred and appreciably widen the debate.

The identification of managers that consistently add value is one reason to consider an alternative to passive management.

One of the key questions facing investors at the moment is whether inflation or deflation represents the bigger risk in the coming years.

Now more than ever, given the likely economic environment in the years ahead, investors need to consider all their options when building a portfolio for their future. This may mean a number of things, including: increasing diversification, investing in new or different markets, being active, and flexible to take advantage of unique opportunities as they arise.

Those portfolios overly reliant on traditional markets, such as equities and fixed income in particular, run the risk of failing to meet to their investment objectives over the next ten years.

Conundrum Facing Investors

A recent article by Alan Dunne, Managing Director, Abbey Capital, The Inflation-Deflation debate and its Implications for Asset Allocation, which recently appeared in AllAboutAlpha.com, clearly outlines the conundrum currently facing investors.

As the article highlights, one of the “key questions facing investors at the moment is whether inflation or deflation represents the bigger risk for the coming years. Economists are split on this….”

Following a detailed analysis of the current and likely future economic environment and potential influences on inflation or deflation (which is well worth reading) the article covers the Implications for Asset Allocations.

Inflation or Deflation: Implications for Asset Allocations

The article makes the following observations as far as asset class performance in different inflation environments, based on historical observations:

Deflation like in the 1930s, is negative for equities but positive for Bonds.

If inflation picks ups, or even stagflation, that would be negative for real returns on financial assets and real assets may be favoured.

They conclude: “the current uncertainty highlights the importance of holding diversified portfolios, with exposure to a range of traditional and alternative assets and strategies with the potential to deliver returns in different market environments.”

Current Environment

Abbey Capital anticipate greater co-ordination of policy between governments (fiscal policy) and central banks (monetary policy).

As they note, “many economists draw a parallel between the current scenario and the substantial increase in government debt during World War II. One of the consequences of higher debt levels is that we may see pressure on central banks to maintain interest rates at low levels and maintain asset purchases to ensure higher bond issuance is not disruptive for bond markets i.e. coordination of monetary and fiscal policies.”

I think this will be the case. The Bank of Japan has maintained a direct yield curve control policy for some time and the Reserve Bank of Australia has implemented a similar policy recently. Direct yield curve control is where the central bank will target an interest rate level for the likes of the 3-year government bond.

In the environment after World War II debt levels were brought back to more manageable levels by keeping interest rates low (a process known as financial repression).

From a government policy perspective, financial repression reduces the real value of debt over time. It is the most palatable of a number of options.

Financial repression is potentially negative for government bonds

With interest rates so low, and likely to remain low for some time given policies of financial repression the real return (after inflation) on many fixed income instruments and cash could be negative.

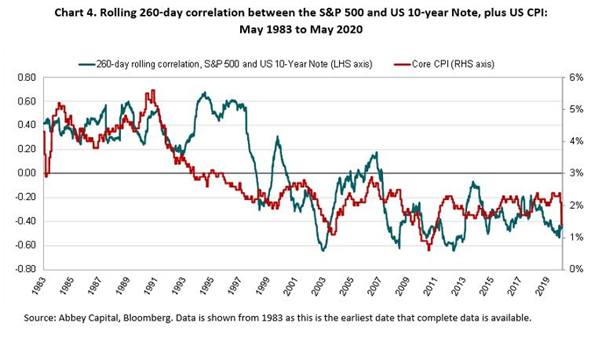

A higher level of inflation not only reduces the real return on bonds but potentially also reduces the diversification benefits of holding bonds in a portfolio with equities.

The diversification benefits of bonds in the traditional 60 / 40 equity-bond portfolio (Balanced Portfolio) has been a strong tail wind over the last 20 years.

The more recent low correlation between bonds and equities is evident in the Chart below, which was presented in the article.

The Chart also highlights that the relation of low correlation between equities and bonds, which benefits a Balanced Portfolio, has not always been present.

As can be seen in the Chart, in the 1980s, when inflation was a greater concern, inflation surprises were negative for both bonds and equities, they became positively correlated.

What should investors do?

“Investors are therefore left with the challenge of finding alternatives for government bonds, ideally with a low or negative correlation to equities and protection against possible inflation.”

The article runs through some possible investment solutions and approaches to meet the likely challenges ahead. I have outlined some of them below.

I think duration (interest rate risk) and credit can still play a role within a broad and truly diversified portfolio. Within credit this would likely involve expanding the universe to include the likes of high yield, securitised loans, private debt, inflation protections securities, and emerging market debt as examples.

The key and most important point is that a robust portfolio will be less reliant on tradition asset classes, traditional asset class betas, to drive investment return outcomes. This is likely to be vitally important in the years ahead.

Accordingly, investors will need to be more active, opportunistic, and maintain very broad and truly diversified portfolios. Not only within asset classes, such as the fixed income example provided above, but across the portfolio to include the likes of real assets and liquid alternatives.

Real assets

Abbey Capital comment that “Real assets such as property and infrastructure should provide protection against higher inflation for long-term investors but may not be attractive for investors valuing liquidity.”

Although the maintenance of portfolio liquidity is important, Real assets can play an important role within a robust portfolio.

For the different types of real assets, their investment characteristics, and likely performance and sensitivity to different economic environments, including economic growth, inflation, inflation protection, stagflation, and stagnation please see the Kiwi Investor Blog Post, Real Assets Offer Real Diversification. The extensive analysis has been undertake by PGIM.

Liquid Alternatives

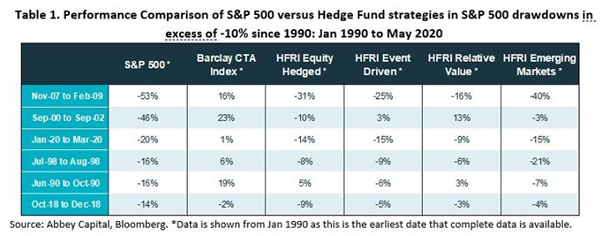

Abbey Capital provide a brief discussion on liquid alternatives with a focus on managed futures. Not surprisingly given their pedigree.

They provide the following Table which highlights the benefit of liquid alternatives and hedge funds at time of significant sharemarket declines (drawdowns).

Concluding Remarks

Being a managed futures manager, it is natural to be cautious of Abbey Capitals concluding remarks, being reminded of the Warren Buffet quote, “Never ask a barber if you need a haircut.”

Nevertheless, the Abbey Capital’s economic analysis and investment recommendations are consistent with a growing chorus, all singing from a similar song sheet. (Perhaps we could call this a “Barbers Quartet”!)

Without having an axe to grind, and in all seriousness, I have covered similar analysis and comments in previous Posts, the conclusions of which have a high degree of validity and should be considered, if not a purely from portfolio risk management perspective so as to understand any gaps in current portfolios for a number of likely economic environments.

The key and most important point is that robust portfolios will be less reliant on traditional asset classes, traditional asset class betas, to drive investment return outcomes.

Accordingly, investors will need to be more active, opportunistic, and maintain very broad and truly diversified portfolios

Therefore, it is hard to disagree with one of the concluding remarks by Abbey Capital “To account for the competing requirements in a portfolio of returns, low correlation to equities, liquidity and possible inflation protection, investors may need to build robust portfolios with a broader mix of assets and strategies.”

Other Reading

For those interested, previous Kiwi Investor Blog posts of relevance to the Abbey Capital article include:

Preparing your Portfolio for a period of Higher Inflation, this is the Post of most relevance to the current Post, and covers a recent Man article which undertook an analysis of the current economic environment and historical episodes of inflation and deflation.

Man conclude that although inflation is not an immediate threat, the likelihood of a period of higher inflation is likely in the future, and the time to prepare for this is now. Man recommends several investment strategies they think will outperform in a higher inflation environment.

It also includes analysis by PIMCO, where it is suggested to “diversify your diversifiers”.

Lastly, Sharemarket crashes – what works best in minimising losses, market timing or diversification, covers a research article by AQR, which concludes the best way to manage periods of severe sharemarket decline is to have a diversified portfolio, it is impossible to time these episodes. AQR evaluates the effectiveness of diversifying investments during sharemarket drawdowns using nearly 100 years of market data.

There are a wide range of reasons for choosing an alternative to passive investing over and above the traditional industry debate that focuses on whether active management can outperform an index.

Reasons for considering alternatives include no readily replicable market index exists, available indices are unsuitable in meeting an investor’s objectives, and/or there are some imbedded inefficiency within the Index.

Under these circumstances a passive approach no longer becomes optimal nor appropriate.

Or quite simply, an active manager with skill can be identified, this alone is sufficient to consider an alternative to passive indexing.

Importantly, the decision to choose an alternative to passive investing is likely to vary across asset classes, investors, and time.

Also, the active versus passive debate needs to be broadened, which to date seems too narrowly focused on comparing passive investments with the average returns from active equity managers.

Framework for choosing an Alternative to Passive Investing

They do this by presenting a framework for a more comprehensive consideration of alternatives to passively replicating a standard capitalisation-weighted index in any particular asset class.

In doing so they provide examples of circumstances under which a particular alternative to passive management might be preferred.

They offer no conclusions as to whether any specific approach is intrinsically superior. “Indeed, the overarching message is that best choices can vary across asset classes, investor circumstances, and perhaps even time.”

Warren and Ezra provide the following Framework for choosing an Alternative to Passive Investing:

Their framework appreciably widens the range of reasons for choosing an alternative to passive investing.

As can be seen in the Table above, they have identify five potential reasons investors should seek an alternative to passive index.

The first three reflect situations where a passive index is either unavailable or unsuitable, and two relate to investor expectations that active management can outperform passive benchmarks.

Below I have provided a description of the five reasons investors should seek an alternative to passive index.

Back ground Comments

Warren and Ezra provide some general comments on the state of the industry debate:

They think it is unreasonable to base broad conclusions about the relative efficacy of passive indexing on active managers’ average results in a single asset class or subclass, such as U.S. equities. They note, “What holds true in one market segment may not hold in another.”

They also object to the “implicit assumption that in the absence of demonstrable stock-selection skills among managers, passive index replication provides optimal exposure for investors.” This assumption does not take into account differences in investor objectives and circumstances. This is one of the core points of their article.

They maintain, what is missing in the industry debate is “recognition that appropriate structuring and management of investments may well depend on investors’ relative situations.”

Some Context

The default position for passive investing is a capitalisation-weighted (cap-weighting) index, such as the New Zealand NZSX 50 Index and US S&P 500.

Although somewhat technical, the application of a cap-weighting index rests on the three assumptions outlined below.

A breach in any of the following assumptions could justify giving consideration to an alternative approach to passive indexing.

Market efficiency.

Cap-weighting should be chosen under an assumption of perfectly efficient markets, where prices are always correct. Investors may consider alternatives if they believe markets are not fully efficient and that the repercussions of any inefficiencies can be either avoided or exploited.

Cap-weighting is aligned with investor objectives.

It is assumed that cap-weighting indices are aligned with investor objectives. However, this is not always the case. As we see below, a Defined Benefit plan most likely has different objectives relative to a cap-weighted fixed income index.

The same is true for an endowment, insurance company, or foundation.

Index efficacy.

The view of passive indexing as the default assumes that an index is available for the intended purpose. The theoretical view calls for indexes that effectively embody the market portfolio. The industry view requires indexes that deliver the desired type of asset class exposure. In practice, it is possible that for a given asset class no market index exists, or that available indexes have shortcomings in their construction.

The five reasons below for when investors might prefer an alternative to a passive approach are in situations where these three critical assumptions for passive indexing are broken. In such situations passive index is likely to be inappropriate.

The reasons below, also highlight the point that the active versus passive debate often fails to take into account differences in investor objectives and circumstances. The debate needs to be broadened.

Reason #1: No Readily Replicable Index is Available

Passive investing assumes an effective index exists that can be easily and readily replicated.

In some instances, an appropriate index to replicate is simply not available, for example:

Unlisted assets such as Private Equity, unlisted infrastructure and direct property

Within listed markets were a lack of liquidity exists it becomes difficult to replicate the index, such as small caps, emerging market equities, and high-yield debt.

In these incidences, although a passive product may be available, they “might not deliver a faithful replication of the asset class at low cost.” Accordingly passive investing is not appropriate.

Reason #2: The Passive Index Is at Odds with the Investor’s Objectives

Often a passive index is badly aligned with an investor’s objectives. In such cases an alternative approach may better meet these objectives, often requiring active management to deliver a more tailored investment solution.

By way of example:

Defined Benefit Pension Plan and tailored fixed-income mandates.

Best practice for a Defined Benefit (DB) plan is to implement a tailored fixed income mandate that closely matches expected liabilities.

In such a case a passive index approach is not appropriate given the duration and cashflows of the DB plan are unique and highly unlikely to be replicated by an investment into a passive index based on market capitalisation weights.

DB plan managers may also likely prefer more control over other exposures, such as credit quality relative to a passive index.

Such situations also exits for insurance companies, endowments, and foundations.

Notably, an individual investor has a unique set of future liabilities, represented by their own cashflows and duration. Accordingly, investing into a passive market index product may not be appropriate relative to their investment objectives. A more active decision should be made to meet cashflow, interest rate risk, and credit exposure objectives.

Listed infrastructure provides another example where the passive index may be at odds with the investor’s goals. Some investors may want to target certain sectors of the universe that provides greater inflation protection, thus requiring a different portfolio relative to that provided by a passive market index exposure.

The article also provides example in relation to Sustainable and ethical investing and Tax effectiveness.

Reason #3: The Standard Passive Index is Inefficiently Constructed

Where alternatives are available, it makes no sense to invest in an inefficient index. This represents a suboptimal approach, particularly if an alternative can deliver a better outcome.

The article presents two potential reasons an index might be inefficient and proves three examples.

They comment that an index might be inefficient for the following reasons:

the index is built on a narrow or unrepresentative universe; and

the index is constructed in a way that builds in some inefficiency.

As they highlight, these issues are best outlined through the discussion of examples. I briefly cover two.

Equities

Alternative indexing/passive approaches such as factor investing and fundamental investing are “active” decision relative to a market-capitalised index.

The basis for these alternative approaches is that equity capital market indices are flawed (Fundamental Investing) and inefficient (e.g. factor investing such as value and small caps outperform the broader market over time).

Fixed income

There are many shortcomings of fixed-income indices, the article focuses on two:

Fixed income indices do not fully represent the asset class. Therefore, more efficient portfolios may be built by including off-benchmark securities.

The largest issuers dominate fixed income indices and it can be argued these are the less attractive governments/companies to invest in, because they are most in need of funding (and hence of lower quality), or are issuing debt to take advantage of low interest rates, which are unattractive to the investor.

Reasons #4 and #5 The final two reasons are more aligned with the traditional question of whether investors can access managers that can be expected to outperform the index.

Reason #4 features that could lead to active investment managers outperforming the passive alternative in aggregate.

Active management is often defined as a zero-sum game before transaction costs, and a negative-sum game after transaction costs. Therefore, active management as a whole cannot outperform.

However, this dynamic need not apply to all investors and it is quite likely that there is a subsector of investors that can consistently outperform the index.

Therefore, a review of the environment in which managers operate might establish if they are able to maintain a competitive advantage.

The following features are outlined in the article to support such a situation:

Market inefficiency situations

Market inefficiencies offer the potential for active managers to outperform the index, nevertheless managers need to be appropriately placed to capture any excess rewards of these inefficiencies.

The following situations may provide a manager with a competitive advantage:

Information advantage: An active manager could have an advantage where the market is “widely populated by less-informed investors” e.g. emerging markets and small caps.

Preferential access to desirable assets: e.g. where active managers have better access to initial public offerings and sourcing lines of stock. In unlisted markets private equity manager has well established relationships and ability to provide capital and/or appropriate skills.

Economic value-add: e.g. in unlisted assets active management can add value to the underlying asset.

Opportunities arising from differing investor objectives

Opportunities for active management to benefit may exist when:

Some investors are comfortable with earning below-market returns e.g. investors who place greater weight on liquidity or are not willing to accept certain risk exposures

Investors have differing time horizons e.g. value investors exploit short-term focus of markets

Index fails to cover the opportunity set

The article makes the following points under this heading:

There is the potential to outperform by investing outside the index whenever the index does not provide a comprehensive coverage of the available market

The intensity of competition is also a factor in success or otherwise of an active manager. For example, the results on manager skill of the highly institutionalise US market may not translate into other markets and asset class where competition is less fierce.

Cyclicality of markets needs to be considered, with managers likely to perform in different market environments i.e. they tend to underperform when cross-sectional volatility is low, or markets are driven more by thematic forces. As they note, this has limited relevance in the long run, but may add a “timing element to any evaluation of active versus passive investment.”

Reason #5: Skilled Managers Can Be Identified

Where a skilled manager can be identified, this is a sufficient condition to adopt an alternative to passive management alone.

Nevertheless, the ability and capacity to identify a skilled manager is necessary where an alternative to passive management is to be contemplated.

The discussion makes the following points:

At the very least bad managers should be avoided

Markets can never be perfectly efficient, therefore some room exists for outperformance through skill

Not all fund managers are created equal, some are good and some are bad

The research capability and skill to identify and select a manager is an important consideration.

Implementation and Costs

It is important to note, the framework aims first to work out whether there is a case for rejecting a passive index default. The next step is then to ask how much an investor is willing to pay and how the alternative can be accessed.

“In most cases this alternative will be what is traditionally known as “actively managed investing.” In other circumstances this need not be the case, or the skills-based component may be minor.”

The cost versus the benefit and accessing the preferred alternative approach to passive index are key implementation issues.

Concluding Comments

Warren and Ezra make the point that too much of the debate on active versus Passive relies on the analysis of US equities, they think it is unreasonable to base broad conclusions about the efficiency of passive indexing on a single asset class or subclass.

For the record, please see this Post, Kiwi Wealth caught in an active storm, on my thoughts on the active vs passive debate, we really need to move on and broaden the discussion. The debate is not black vs White, as highlighted in this article, there are large grey areas.

Although inflation is not a threat currently the case for a period of higher than average inflation can be easily made.

From an investment perspective:

A period of high inflation is the most challenging period for traditional assets e.g. equities and Fixed Income;

Before the inflation period, as we move from the current period of deflation there is a period of reflation, during which things will feel okay for a while; and

During the higher inflation period the leadership of investment returns are likely to change.

Following an extensive review of previous inflation/deflationary episodes Man clearly articulate the case for a period of higher inflation is ahead.

As Man note the timing of moving to a higher inflation environment is uncertain.

As outlined below, they provide a check list of factors to monitor in anticipation of higher inflation.

Nevertheless, although the timing of a higher inflation environment is uncertain, Man argue the need for preparation is not and should commence now.

Investors need to be assessing the robust of their portfolios for a higher than average inflation environment now.

Man identify several strategies they expect will outperform during a period of higher inflation.

Investment Implications

The level and direction of inflation is important.

This is evident in the diagram below, which Man refer to as the Fire and Ice Framework.

The performance of investment strategies differs depending on the inflation environment.

As can be seen in the diagram, the traditional assets of equities and bonds (fixed income securities) have on average performed poorly in the inflation periods (Fire).

Also, of note is that the benefits of Bonds in providing portfolio diversification benefits are diminished during these periods, as signified by the positive stock-bond correlation relationship.

As Man note, and evident in the diagram above, the path to inflation is via reflation, so things will feel good for a while.

Importantly, there will be a regime change, those investment strategies that have flourished over the last 10 years are likely to struggle in the decade ahead.

The expected new winners in a higher inflation environment are succinctly captured in the following diagram.

As can been seen in the Table above, Man argue new investment strategies are needed within portfolios.

These include:

Alternative risk premia and long-short (L/S) type strategies, rather than traditional market exposures (long only, L/O) of equities and fixed income which are likely to generate real negative returns (See Fire and Ice Framework).

Real Assets, such inflation-linked bonds, precious metals, commodities, and real estate.

Man also expect leadership within equity markets to change toward value and away from growth and quality. Those companies with Pricing Power are also expected to benefit.

Several pitfalls to introducing the new strategies to a portfolio are outlined in the article.

Time for Preparation is now

As mentioned the timing of a transition to a higher inflation environment is uncertain. Certainly markets are not pricing one in now.

Nevertheless, the preparation for such an environment is now. Man highlight:

the likelihood of an inflationary regime is much higher than it has been in recent times;

the investment implications of this new regime would be so large that all the things that have worked are at risk of stopping to work; and

given that markets are not priced for higher inflation at all, the market inflationary regime may well start well before inflation actually kicks in, given the starting point.

Man believe investors have some time to prepare for the regime shift. Nevertheless, those preparations should start now.

In addition, Man provide a check list to monitor to determine progress toward a higher than average inflation environment.

Inflation Check List to Monitor

The paper undertakes a thorough review of different inflation regimes and the drivers of them. The review and analysis on inflation makes up a large share of the report and is well worth reviewing.

Man identify five significant regime changes to support their analysis:

Hoover’s Depression and Roosevelt’s New Deal (Deflation to Reflation)

WW2-1951 Debt Work-down (Inflation to Disinflation).

The Twin Oil Shocks of the 1970s (Inflation).

Paul Volcker (Disinflation).

The Global Financial Crisis (Deflation to Reflation and back again).

As noted in the list above, we are currently in a deflationary environment (again) – Thanks to the Coronavirus Pandemic.

Man expect the deflationary forces over the last decade are likely to fade in the years ahead. As a result inflation is likely to pick up. Central banks are also likely to allow an overshoot relative to inflation targets. Their independence could also be at risk.

They argue the current deflationary status quo is unsustainable, high debt levels leading to underinvestment in product assets resulting in lower levels of spare capacity and rising levels of inequality around the world will lead to policy responses by both governments and central banks that will result in a period of higher than average inflation.

They provide a checklist of factors to monitor, which includes:

Inflation Momentum, which is broadly neutral currently

Measures of inflation in the pipeline, which are currently deflationary

Economic slack, which is large and heavily deflationary at present

Labour market tightness, which is loose and heavily deflationary presently

Wage inflation, currently neutral to inflationary

Inflation Expectations, sending mixed signals at this time

Man conclude their dashboard is more deflationary than inflationary. They also believe this could change quite rapidly if demand picks up faster than expected.

Concluding Remarks

Man’s view on the outlook for inflation are not alone, a number of other organisations hold similar views.

Although inflation is not a problem now, it is highly likely to become of a greater concern to investors than recent history.

This will likely lead to a change in investment return leadership. Those investment strategies that have worked well over the last 10 years are unlikely to work so well in the decade ahead. Man propose some they think will perform better in such an environment, there are likely others.

A review of current portfolio holdings should be undertaken to determine the robustness to a different inflation regime. This is a key point.

The performance of real assets in different economic environments was covered in a previous Post, Real Assets offer real diversification benefits, this Post covered analysis undertaken by PGIM.

“The Bet” received considerable media attention following the 2017 Berkshire Hathaway shareholder letter in 2018.

To recap, the bet was between Warren Buffet and Protégé Partners, who picked five “funds of fund” hedge funds they expected would outperform the S&P 500 Index over the 10-year period ending December 2017. Buffet took the S&P 500 to outperform.

The bet was made in December 2007, when the market was reasonably expensive and the Global Financial Crisis (GFC) was just around the corner.

Buffet won. The S&P 500 easily outperformed the Hedge Fund selection over the 10-year period.

There are some astute investment lessons to be learnt from this bet, which are very clearly presented in this AllAboutAlpha article, A Rhetorical Oracle, by Bill Kelly.

Before reviewing these lessons, I’d like to make three points:

I’d never bet against Buffet!

I would not expect a Funds of Funds Hedge Fund to consistently outperform the S&P 500, let alone a combination of five Funds of Funds.

Most if not all, investor’s investment objective(s) is not to beat the S&P 500. Investment Objectives are personal and targeted e.g. Goal Based Investing to meet future retirement income or endowments

This is not to say Hedged Funds should not form part of a truly diversified investment portfolio. They should, as should other alternative investments.

Nevertheless, I am unconvinced Hedge Fund’s role is to provide equity plus like returns.

One objective in allocating to alternatives is to add return sources that make money on average and have low correlation to equities. Importantly, diversification is not the same thing as “hedging” a portfolio

Now, I have no barrow to push here, except advocating for the building of robust investment portfolios consistent with meeting your investment objectives. The level of fees also needs to be managed appropriately across a portfolio.

In this regard and consistent with the points in the AllAboutAlpha article:

Having a well-diversified portfolio is paramount and results in better risk-adjusted returns over time.

Being diversified across non-correlated or low correlated investments is important, leading to better risk-adjusted outcomes.

Adding low correlated investments to an equities portfolio, combined with a disciplined rebalancing policy, will likely add value above equities over time.

The investment focus should be on reducing portfolio volatility through true portfolio diversification so that wealth can be accumulate overtime.

Minimising loses results in higher returns over time. A portfolio that falls 50%, needs to gain 100% to get back to the starting capital. This means as equity markets take off a well-diversified multi-asset portfolio will not keep up. Nevertheless, the well diversified portfolio will not fall as much when the inevitable crash comes along.

It is true that equities are less risky over the longer term. Nevertheless, not many people can maintain a fully invested equities portfolio, given the wild swings in value (as highlighted by Buffett in his Shareholder Letter, Berkshire can fall 50% in value).

100% in equities is often not consistent with meeting one’s investment objectives. Buffet himself has recommended the 60/40 equities/bond allocation, with allocations adjusted around this target based on market valuations.

I am unlikely to ever suggest to be 100% invested in equities for the very reason of the second point in the article, as outlined below.

Investment Behavioural aspects.

How many clients would have held on to a 100% equity position during the high level of volatility experienced over the last 10-12 years, particularly in the 2008 – 2014 period. Not many I suspect. This would also be true of the most recent market collapse in 2020.

The research is very clear, on average investors do not capture the full value of equity market returns over the full market cycle, largely because of behavioural reasons.

A well-diversified portfolio, that lowers portfolio volatility, will assist an investor in staying the course in meeting their investment objectives.

An allocation to alternative strategies, including a well-chosen selection of Hedge Funds, will result in a truly diversified Portfolio, lowering portfolio volatility. See an earlier Post, the inclusion of Alternatives has been an evolutionary process, not a revolution.

Staying the course is the biggest battle for most investors. Therefore, take a longer-term view, focus on customised investment objectives, and maintain a truly diversified portfolio.

This will help the psychological battle as much as anything else.

I like this analogy of using standard deviation of returns as a measure of risk. It captures the risks associated with a very high volatile investment strategy such as being 100% invested in equities:

“A stream may have an average depth of five feet, but a traveler wading through it will not make it to the other side if its mid-point is 10 feet deep. Similarly, an overly volatile investing strategy may sink an investor before she gets to reap its anticipated rewards.”

Endowments and Sovereign wealth Funds lead the way in building robust investment portfolios in meeting a wide range of challenging investment objectives. This Post covers this and amongst other things, what true diversification is, it is not having more and more asset classes, a robust portfolio is broadly diversified across different risks and returns. A lot can be learnt from how Endowments construct portfolios, take a long term view, and seek to match their client’s liability profile. Although fees are important, an overriding focus on fees may be detrimental to building a robust portfolio and in meeting client investment objectives.

This Post builds on the Post above and looks at an investment framework for individuals, developed by EDHEC-Risk Institute and their Partners. It is a Goal Based Investment framework with a focus on capital value but also delivering a secure and stable level of replacement income in retirement.

This Post emphasises the need to focus on generating a stable and secure level of replacement income in retirement as an investment goal and highlights the approach that is required to achieve this. Such an approach would greatly enhance the outcomes of Target Date Funds. This Post also references the thoughts of Professor Robert Merton around having a greater focus on generating replacement income in retirement as an investment objective and that volatility of replacement income is a better measure of investment risk, as it is more aligned with investment objectives, unlike the volatility of capital or standard deviation of returns.

Kiwi Investor blog has covered many topics over the year, including the value of active management, the shocking state of the investment management industry globally, Responsible Investing, the high cost of index funds and being out of the market.

Of these, recent research into the failure of the 4% rule in almost all markets worldwide is well worth highlighting.

Kiwi Investor Blog has a primary focus on topics associated with building more robust portfolios and investment solutions.

The Blog has highlighted the research of EDHEC-Risk Institute throughout the year. EDHEC draw on the concept of Flexicurity. This is the concept that individuals need both security and flexibility when approaching investment decisions. This is surely a desirable goal and the hallmark of a robust investment portfolio. The knowledge is available to achieve this and the framework and rationale is covered in the Posts above.

I don’t think the Uber moment has been reached in the investment management industry yet. Technology will be very important, but so too will be the underlying investment solution. The investment solution needs to be more tailored to an individual’s investment objectives.

As outlined in the Posts highlighted above, the framework for the investment solution has emerging and is developing.

It is a goal based investment solution, more closely tailored to an individual’s investment aspirations, so as to provide a more secure and stable level of replacement income in retirement.

Flexicurity is the concept that individuals need both security and flexibility when approaching retirement investment decisions. See EDHEC-Risk Institute.

Annuities, although providing security, can be costly, they represent an irreversible investment decision, and often cannot contribute to inheritance and endowment objectives. Also, Annuities do not provide any upside potential.

Likewise, modern day investment products, from which there are many to choose from, provide flexibility yet not the security of replacement income in retirement. Often these Products focus solely on managing capital risk at the expense of the objective of generating replacement income in retirement. In short, as outlined by EDHEC-Risk, modern day Target Date Funds “provide flexibility but no security because of their lack of focus on generating minimum levels of replacement income in retirement.”

Therefore, a flexicure retirement solution is one that provides greater flexibility than an annuity and increased security in generating appropriate levels of replacement income in retirement than many modern day investment products do.

EDHEC offers a number enhancements to improve the outcomes of current investment products.

One such approach, and central to improving investment outcomes for the current generic Target Date Funds (TDF), is designing a more suitable investment solution in relation to the conservative allocation (e.g. cash and fixed income) within a TDF. Such an enhancement would also eliminate the need for an annuity in the earlier years of retirement.

From this perspective, the conservative allocations within a TDF are risky when it comes to generating a secure and stable level of replacement income in retirement. These risks are not widely understood nor managed appropriately.

The conservative allocations with a TDF can be improved by being employed to better matching future cashflow and income requirements. While also focusing on reducing the risk of inflation eroding the purchasing power of future income.

This requires moving away from current market based shorter term investment portfolios and implementing a more customised investment solution.

The investment approach to do this is readily available now and is based on the concept of Liability Driven Investing applied by Insurance Companies. Called Goal Based Investing for investment retirement solutions. #Goalbasedinvesting

The techniques and approaches are available and should be more readily used in developing a second generation of TDF (which can be accessed in some jurisdictions already).

This is relevant to improving the likely outcome for many in retirement. With this knowledge it would help make finance more useful again, in providing very real welfare benefits to society. #MakeFinanceUsefulAgain

Flexicure, is my word of the year! Hopefully, we will hear this being used further in relation to more Robust Investment Portfolios, particularly those promoted as Retirement Solutions.

As you know, my blog this year has had a heavy focus on retirement solutions and has drawn upon the analysis and framework of EDHEC-Risk Institute.

Nevertheless, the greatest enhancement would come from implementing a more targeted cashflow and income matching portfolio within the conservative allocations as discussed above.

Wishing you all the best for the festive season and a prosperous New Year.

As you will know the US economy is into its second longest period of economic expansion which commenced in June 2009.

Should the US economy continue to perform until July 2019, which appears likely, the US will enter its longest period of economic expansion. The longest expansion was 10 years, occurring during the tech expansion of the 1990s, the current expansion is nine years.

Similarly, the US sharemarket is into its longest bull market run, having not experienced a drop-in value of greater than 20% (bear market) since March 2009.

As a rule, sharemarkets generally enter bear markets in the event of a recession.

Nevertheless, while a recession is necessary, it is not sufficient for a sharemarket to enter a bear market.

Since 1957, the S&P 500, a measure of the US sharemarket:

three bear markets where “not” associated with a recession; and

three recessions happened without a bear market.

Statistically:

The average Bull Market period has lasted 8.8 years with an average cumulated total return of 461%.

The average Bear Market period lasted 1.3 years with an average loss of -41

Historically, and on average, equity markets tend not to peak until six – twelve months before the start of a recession.

Therefore, let’s look at some of the Recession indicators.

In a recent article by Brandywine, they ran through some of the key indicators for a US recession.

Federal Reserve Bank of Atlanta’s GDP Nowcast.

This measure is forecasting annualised economic growth of 4.4% in the third quarter of 2018. This follows actual annualised growth of 4.2% in the second quarter of 2018.

Actual US economic data is strong currently. Based on the following list:

US unemployment is 3.7%, its lowest since 1969

Consumer Confidence is at an 18 year high

US wages are growing at around 3%, the savings rate is close to 6%, leaving plenty of room for consumers to increase spending

Small business confidence is at all-time highs

Manufacturing and non-manufacturing surveys are at their best levels for some time (cycle highs)

Leading Indicators

The Conference Board’s Index of Leading Indicators, an index of 10 components that includes the likes of the ISM New Order Index, building permits, stock prices, and the Treasury yield curve.

The Conference Board’s Index is supportive of ongoing economic activity in the US.

An inverted yield curve, where shorter term interest rates (e.g. 2 years) are higher than longer term interest rates (e.g. 10 years) has a pretty good record in predicting a recession, in 18 months’ time on average.

With the recent rise of longer dated interest rates the prospect of an inverted yield curve now looks less likely.

Albeit, with the US Federal Reserve is likely to raise short term interest rates again this year and another 3-4 times next year the shape of the yield curve requires on going monitoring.

Having said that, an inverted yield curve alone is not sufficient as a predictor of economic recession and needs to be considered in conjunction with a number of other factors.

Brandywine conclude, “what does a review of some well-known recession indicators tell us about the current—and future—state of the U.S. expansion? The information provided by the indicators is mixed, but favors the continuation of the current expansion. The leading indicators are telling us the economy should continue to expand well into next year—at least.”

In favour of ongoing economic expansion is low unemployment, rising wages, simulative financial conditions (e.g. low interest rates are supportive of ongoing growth, as are high equity prices), high savings rate of consumer and their low levels of debt. Lastly government spending and solid corporate profitability is supportive of economic activity over the medium term.

As a word of caution, ongoing US – China trade dispute could derail global growth. Other factors to consider are higher interest rates in combination with a higher oil price.

Noting, Equity markets generally don’t contract until interest rates have gone into restrictive territory. This also appears some time away but is a key factor to monitor.

Lastly, a combination of higher oil prices and higher interest rates is negative for economic growth.

I have used on average a lot in this Post, just remember: “A stream may have an average depth of five feet, but a traveler wading through it will not make it to the other side if its mid-point is 10 feet deep. Similarly, an overly volatile investing strategy may sink an investor before she gets to reap its anticipated rewards.”

Happy investing.

Global Investment Ideas from New Zealand. Building more Robust Investment Portfolios.

Cambridge Associates recently published a research report concluding it does not pay to be out of the market.

” Investors who take money out of the market too early stand to “risk substantial underperformance,”

Cambridge advised investors concerned about the length of the current bull market not to bail out of equity markets earlier than necessary in an attempt to avoid exposure to downturns.

This seems timely given current market volatility.

As the article notes, it is hard to time markets “because trying to time re-entry to get back into the markets at lower levels leads to substantially lower long-term returns, the researchers found. For example, the report showed that being out of the market for just the two best quarters since the turn of the last century cut cumulative real returns on U.K. equities by more than 50 percent.”

“That effect is even more profound in the United States, where sitting out the best two quarters cut cumulative real returns by more than two thirds, according to the report.”

“While no investor should be ignoring valuations, becoming too focused on timing an exit has substantial risks,” said Alex Koriath, head of Cambridge’s European pensions practice, in a statement accompanying the research. “The best periods for returns tend to be very concentrated, meaning that exiting at the wrong time could drag down cumulative returns significantly.”

This is a pertinent issue given the US sharemarket is into its longest bull market run in history. Also, of interest, historically on average, markets perform very strongly over the final stages of a bull market run. Lastly, bull markets tend to, more often than not, end six-twelve months prior to a recession. Noting, this is not always the case. Albeit, the consensus is not forecasting a recession in the US for some time. It appears, the probability of a US recession in the next couple of years is low.

The key forward looking indicators, such as shape of the yield curve, significant widening of high yield credit spreads, rising unemployment, and falling future manufacturing orders are not signalling a recession is on the horizon in the US. Please see my earlier posts History of Sharemarket corrections – An Anatomy of equity market corrections

What is the answer?

It is difficult to time markets. AQR came to a similar conclusion in a recent article. AQR argue the best form of defence is a truly diversified portfolio. I agree and this is a core focus of this Blog.

As we know equity markets have drawdowns, declines in value of over 20%. In the recent AQR article they estimate that there have been 11 episodes of 20% plus drawdowns since 1926, a little over once every 10 years! Bearing in mind the last major drawdown was in 2008 – 09.

The average peak to trough has been -33% and on average it has taken 27 months to get back to the pre-drawdown levels.

As AQR note, we cannot consistently forecast and avoid these severe down markets. In my mind, conceptually these drawdowns are the risk of investing in equities. With that risk, comes higher returns over the longer term relative to investing in other assets.

At the very least we can try and reduce our exposure by strategically tilting portfolios, as AQR says, “if market timing is a sin, we have advocated to “sin a little””.

I agree with the Cambridge Associates article to never be out of the market completely and with AQR to strategically tilting the portfolio. These tilts should primarily be based on value, be subject to a disciplined research process, and focused more on risk reduction rather than chasing returns. This approach provides the opportunity to add value over the medium to longer term.

Nevertheless, by far a better solution is to truly diversify and build a robust portfolio. This is core to adding value, portfolio tilting is a complementary means of adding value over the medium to long term relative to truly diversifying the portfolio.

True diversification in this sense is to add investment strategies that are lowly correlated with equities, while at the same time are expected to make money over time. Specifically, they help to mitigate the drawdowns of equities. For example, adding listed property and listed infrastructure to an equity portfolio is not providing true portfolio diversification.

In this sense truly “alternative” investment strategies need to be considered e.g. Alternative Risk premia and hedge fund type strategies. Private equity and unlisted assets are also diversifiers.

Again conceptually, there is a cost to diversifying. However, it is the closest thing in finance to a free lunch from a risk/return perspective i.e. true portfolio diversification results a more efficient portfolio. Most of the diversifying investment strategies have lower returns to equities. There are costs to diversification whether using an options strategy, holding cash, or investing in alternative investment strategies as a means to reduce sharp drawdowns in portfolios.

Nevertheless, a more diversified portfolio is a more robust portfolio, and offers a better risk return outcome.

Also, very few investor’s objectives require to be 100% invested in equities. For most investors a 100% allocation to equities is too volatile for them, which raises the risk that investors act suboptimal during periods of market drawdowns and heightened levels of market volatility i.e. sell at the bottom of the market

A more robust and truly diversified portfolio reduces portfolio volatility increasing the likelihood of investors reaching their investment goals.

As AQR note, diversification is not the same thing as a hedge. Uncorrelated means returns are influenced by other risks. They have different return drivers.

From this perspective, it is also worth noting that adding diversifying strategies to any portfolio means adding new risks. The diversifiers will have their own periods of underperformance, hopefully this will be at a different times to when other assets in the portfolio are also underperforming. Albeit, just because they have periods of underperformance does not mean they are not portfolio diversifiers.

AQR perform a series of model portfolios which highlight the benefits of adding truly diversifying strategies to a traditional portfolio of equities and fixed interest.

No argument there as far as I am concerned.

Happy investing.

Global Investment Ideas from New Zealand. Building more Robust Investment Portfolios.

Their focus on the need for more robust retirement solutions based on Goal Based Investing is so critical.

EDHEC’s and the thoughts of Professor Robert Merton, as outlined in my previous Posts of focusing on income and the volatility of income, are important concepts that will have an immediate and lasting contribution and impact on the ongoing shape of retirement solutions.

As EDHEC outlines, we need investment solutions that provide the certainty of Annuities but with more flexibility. This is the industry challenge.

EDHEC’s and Merton’s work, analysis, and insights have an important and fundamental contribution to the building of more robust retirement solutions that should be considered by anyone working in this area.

Happy investing.

Global Investment Ideas from New Zealand. Building more Robust Investment Portfolios.