The case for holding Government Bonds is all about certainty. The question isn’t why would you own bonds but, in the current environment, why wouldn’t you own bonds to deliver certainty in such uncertain times?

This is the central argument for holding government bonds within a portfolio. The case for holding government bonds is well presented in a recent article by Darren Langer, from Nikko Asset Management, Why you can’t afford not to own government bonds.

As he argues, government bonds are the only asset where you know with absolute certainty the amount of income you will get over its life and how much it will be worth on maturity. For most other assets, you will only ever know the true return in arrears.

The article examines some of the reasons why owning government bonds makes good sense in today’s investment and economic climate. It is well worth reading.

Why you can’t afford not to own government bonds

The argument against holding government bonds are based on expectations of higher interest rates, higher inflation, and current extremely low yields.

As argued in the article, although these are all very valid reasons for not holding government bonds, they all require a world economy that is growing strongly. This is far from the case currently.

They key point being made here, in my opinion, is that the future is unknown, and there are numerous likely economic and market outcomes.

Therefore, investors need to consider an array of likely scenarios and test their assumptions of what is “likely” to happen. For example, what is the ‘normal’ level of interest rates? Are they likely to return to normal levels when the experience since the Global Financial Crisis has been a slow grind to zero?

Personally, although inflation is not an issue now, I do think we should be preparing portfolios for a period of higher inflation, as I outline here. Albeit, this does not negate the role of fixed income in a portfolio.

The article argues that current conditions appear to be different and given this it is not unrealistic to expect that inflation and interest rates are likely to remain low for many years and significantly lower than the past 30 years.

In an uncertain world, government bonds provide certainty. Given multiple economic and market scenarios to consider, maintaining an allocation to government bonds in a genuinely diverse and robust portfolio does not appear unreasonable on this basis.

Return expectations

Investors should be prepared for lower rates of returns across all assets classes, not just fixed income.

A likely scenario is that governments and central banks will target an environment of stable and low interest rates for a prolonged period.

In this type of environment, government bonds have the potential to provide a reasonable return with some certainty. The article argues, the benefits to owning bonds under these conditions are two-fold:

A positively sloped yield curve in a market where yields are at or near their ceiling levels. Investors can move out the curve (i.e. by buying longer maturity bonds) to pick up higher coupon income without taking on more risk.

Investors can, over time, ride a position down the positively-sloped yield curve (i.e. over time the bond will gain in value from the passing of time because shorter rates are lower than longer rates). This is often described as roll-down return.

The article concludes, that although fixed income may lose money during times of strong economic growth, rising interest rates, and higher inflation, these losses can be offset by the gains on riskier assets in a portfolio. Losses on fixed income are small compared to potential losses on other asset classes and are generally recovered more quickly.

No one would suggest a 100% allocation to government bonds is a balanced investment strategy; likewise, not having an allocation to bonds should also be considered unbalanced.

“But a known return in an uncertain world, where returns on all asset classes are likely to be lower than the past, might just be a good thing to have in a portfolio.”

The article on the case for government bonds helps bring some balance to the discussion around fixed income and the points within should be considered when determining portfolio investment strategies in the current environment.

Every year Byron Wien, from Blackstone’s Private Wealth Solutions group, holds a series of Benchmark Lunches where he invites an assortment of hedge fund managers, private equity and real estate leaders, academics, former government officials and economy and market observers.

These meetings, along with his annual “Top Ten Surprises”, not only provide great insights into current economic and market conditions but also provide perspectives to challenge consensus thinking. Particularly his top ten surprises.

In a sign of the times, this year’s Benchmark lunches where held via Zoom.

I briefly summarise some of the topics discussed below, access to the full discussion can be found here.

Economic Conditions

In general, the tone of the sessions was one of optimism tempered by uncertainty.

Most of the participants thought we would be back to something like the normalcy of 2019 by 2022.

There was divergence of opinion what normal would look like, albeit, to get there, a vaccine will need to be developed, tested, manufactured, and administered.

The economy would take some time to gain its own momentum and there will be some permanent changes.

There were some more specific comments in relation to the economy. It was felt that US unemployment would remain high for some time.

Not surprisingly, many expressed concerns for large portions of the economy which are in serious trouble: hotels, restaurants, resorts, cruise lines and airlines will take a long time to recover.

The strong bounce in manufacturing and housing was encouraging, reflecting very low interest rates.

Vaccine

There was considerable optimism amongst the group for a vaccine, reflecting there are many companies working to develop one. Several of these companies are conducting clinical trials and manufacturing doses in anticipation of regulatory approval. Efforts were being undertaken around the world, Europe, Asia, and the United States.

Many expected an effective vaccine to be available for essential workers by the end of this year, with the general public possibly receiving it by the second half of 2021, and by the middle of 2022 most people who wanted the vaccine could have it.

Nevertheless, there were a wider range of views on the details, such as how long the vaccine would last, whether booster shots would be required annually or more frequently to maintain immunity, and the willingness of people to get the shots.

My take from the commentary, the availability of the vaccine is not the end game, there will be lots of issues to work through once it becomes available.

Working remotely, property sectors, and social impacts

The pros and cons of working from home were discussed, which I think are well understood.

Several real estate investors attend the various sessions. They provided the following key insights:

Properties that were well financed could wait out the recession.

Some saw opportunities in the current environment.

Retail was most at risk, and that some damage to the sector would be permanent. It was highlighted that the US is over-stored and has nearly three times the retail space per capita than the next highest country, Canada.

There will be increased costs as people return to the office e.g. increased cleaning costs and perhaps the need to upgrade ventilation systems.

Another interesting statistic provided was that according to a June 2020 BLS study, around 40% of American workers have the ability to work remotely, but the other 60% have to be present physically to perform their duties, whether in hospitals, factories, service businesses or transportation.

It will be these people who will spend less on non-essential items.

An important issue to consider is the social impacts of higher unemployment and uncertainty arising from covid-19.

From a societal perspective the impacts are wide ranging, discussions included the impact on young children and their development, along with university graduates looking to enter the work force at a time of economic recession.

Effects of the enormous government and central bank policy response

Most participants expected interest rates and inflation to remain low for the next several years.

There was a level of scepticism toward Modern Monetary Theory and the ability of governments to print money indefinitely.

For the time being, the policy approach remains appropriate, so long as real growth is higher than the rate of inflation.

The recent weakness in the US dollar was noted. There could be several reasons for this, including Europe and Asia have done a better job of controlling the virus and are recovering more favourably.

Likewise, US factors could be playing a role, such as social unrest, poor discipline in limiting the spread of the virus, and gridlock in Washington. In addition, “The prospect of a sweep in November with both the presidency and the Senate moving to the Democrats and a less business-friendly environment in Congress may also have had an influence on the dollar.”

US Elections

Not everyone thought a Biden victory was a sure thing. There are a lot of issues to consider, albeit Biden has a considerable lead and he will be hard to beat.

The group felt the US as a country overall had shifted to the left.

US China relationship

The growing tensions between China and US is seen as an inevitable outgrowth of the long-term shift towards nationalism and away from globalization.

There was concern in relation to China’s policy towards Hong Kong and its military operations in the South China Sea.

On the positive side, Phase One trade negotiations were moving forward and imports from and exports to China continue. A Phase Two deal seems to be off the table for now.

Although bringing production home or relocating will be difficult, costly, and time-consuming, this trend is partially underway.

Energy Sector

A wide-ranging discussion on the energy sector was undertaken.

For a period of time the drop in oil demand this year was four times greater than during the Global Financial Crisis (GFC). The situation has improved, and it was noted China is consuming more oil currently compared to a year ago.

The US has accumulated excess inventory and US production will remain depressed for some time. At the current oil price shale oil production is unprofitable.

The expectation was that the Oil price will not exceed $50 a barrel for West Texas Intermediate until 2022 when the economy gets back to something close to normal. Political conditions in the Middle East will be more unstable until the price of crude recovers.

A key investment concept is volatility drag. Volatility drag provides a framework for considering the trade-off between the “cost” and “benefit” of reducing portfolio volatility.

The volatility of your portfolio matters. Reducing portfolio volatility helps deliver higher compound returns over the longer-term. This leads to a greater accumulation of wealth over time.

When introducing volatility reduction strategies into a Portfolio a cost benefit analysis should be undertaken.

The cost of reducing portfolio volatility cannot be considered in isolation.

The importance of volatility and its impact on an investment portfolio is captured in a recent article by Aberdeen Standard Investment (ASI), The long-term benefits of finding the right hedging strategy.

The ASI article is summarised below. Access to article via LinkedIn is here.

It is widely accept that avoiding large market losses and reducing portfolio volatility is vital in accumulating wealth and reaching your investment objectives, whether that is attaining a desired standard of living in retirement, an ongoing and uninterrupted endowment, or meeting Pension liabilities.

Understanding Volatility Drag

Volatility Drag is a key concept from the paper: if you lose 50% one year, and make 50% the next, your average return may be zero but you’re still down 25%. This is commonly referred to as the “volatility drag.”

The main disconnect some investors have is they look at returns over a discrete period, such as a year, or the simple average return over two years (zero in the case above).

Instead, investors should focus on the realised compound rate. The compound annualised return in the above example is -13.97% versus simple average return of zero.

ASI make the following point: “The compound (geometric) rate of return will only equal the arithmetic average rate of return if volatility is zero. As soon as you introduce volatility to the return series, the geometric IRR will start falling, relative to the average return.”

This is a key concept to understand. Volatility reduces compounded returns over time, therefore it impacts on accumulated wealth. The focus should be on the actual return investors receive, rather than discrete period returns. Most investment professionals understand this.

Cashflows, into and out of a Portfolio, also impact on actual returns and therefore accumulated wealth. This is why a 100% equities portfolio is unlikely to be appropriate for the vast majority of investors. The short comings of a high equity allocations is outlined in one of my previous Posts: Could Buffett be wrong?

Thought Experiment

In the article ASI offers a thought experiment to make their point, a choice between two hypothetical investments:

Investment A, has an average annual return of 1% with 5% volatility.

Investment B, has twice the average return (2%) but with four times the volatility (20%).

An investor with a long term horizon might allocate to the higher expected return investment and not worry about the higher levels of volatility. The view could be taken because you have a longer term investment horizon more risk can be taken to be rewarded with higher returns.

In the article ASI provides simulated track records of the two investments over 50 years (the graph is well worth looking at).

As would be expected, Investment B with the 20% volatility has a much wider range of possible paths than the lower-volatility Investment A.

What is most interesting “despite having double the average annual return, the more volatile strategy generally underperforms over the long term.”

This is evident in the Table below from the ASI article, based on simulated investment returns:

Average Annual Return

Standard Deviation of Annual Returns

Average total return after 50 years

Average realised internal rate of return (IRR)

A

1%

5%

+53%

0.88%

B

2%

20%

-3.0%

-0.07%

Note, how the IRR is lower than the average annual return e.g. Investment A, IRR is 0.88% versus average annual return of 1.0%. As noted above, they are only the same if volatility is zero.

The performance drag, or “cost”, is due to volatility.

Implications and recognising the importance of volatility

The concept of Volatility Drag provides a framework for considering the trade-off between the “cost” and benefit of reducing portfolio volatility.

The ASI article presents this specifically in relation to the benefits of portfolio hedges, as part of a risk mitigation strategy, and their costs with the following points:

The annual cost can be considered in the context of the potential benefits that come from lowering volatility and more effectively compounding returns.

Putting on exposures with flat or even negative expected returns can still increase your total portfolio return over time if they lower your volatility profile sufficiently.

It is meaningless, therefore, to look at the costs of hedges in isolation.

These points are relevant when considering introducing any volatility reduction strategies into an Investment Portfolio i.e. not just in relation to tail risk hedging. A cost benefit analysis should be undertaken, investment costs cannot be considered in isolation.

As ASI note, investors need to consider the overall portfolio impact of introducing new investment strategies, specifically the impact on the downside volatility of a portfolio is critical.

There are a number of ways of reducing portfolios volatility as outlined below, including the risk mitigation strategies of the ASI article.

Modern Portfolios

The key point is that the volatility of your portfolio matters. Reducing portfolio volatility helps in delivering better compound returns over the longer-term.

Therefore, exploring ways to reduce portfolio volatility is important.

ASI outline the expectation that volatility is likely to pick up in the years ahead, “especially considering the current extreme settings for fiscal and monetary policy combined with rising geopolitical tensions.”

They also make the following pertinent comment, “Uncertainty and volatility aren’t signals for investors to exit the market, but while they persist, we expect investors will benefit over the medium term from having strategies available to them that can help manage downside volatility.”

ASI also note that investors have access to a wide range of tools and strategies to manage volatility. This is particularly relevant in relation to the risk mitigation hedging strategies that manage downside volatility and are the focus of the ASI article.

Therefore, a modern day portfolio will implement several strategies and approaches to reduce portfolio volatility, primarily as a means to generate higher compound returns over time. This is evident when looking at industry leading sovereign wealth funds, pension funds, superannuation funds, endowments, and foundations around the world.

Strategies and Approaches to reducing Portfolio Volatility

There are a number of strategies and approaches to reducing portfolio volatility, Kiwi Investor Blog has recently covered the following:

Real Assets offer real diversification: this Post outlines the investment risk and return characteristics of the different types of Real Assets and the diversification benefits they can bring to a Portfolio under different economic scenarios, e.g. inflation, stagflation. Thus reducing portfolio volatility and enhancing long-term accumulated returns.

What do investors need in the current environment? – Rethink the ‘40’ in the 60/40 Portfolios?: With extremely low interest rates and the likelihood fixed income will not provide the level of portfolio diversification as experienced historically this Post concludes Investors will need to rethink their fixed income allocations and to think more broadly in diversifying their investment portfolio.

Investors seeking to generate higher returns are going to have to look for new sources of income, allocate to new asset classes, and potentially take on more risk.

Investing into a broader array of fixed income securities, dividend-paying equities, and alternatives such as real assets and private credit is likely required.

Investors will need to build more diversified portfolios.

These are key conclusions from a recent article written by Tony Rodriquez, of Nuveen, Rethinking the ‘40’ in 60/40 Portfolios, which appeared recently in thinkadvisor.com.

The 60/40 Portfolio being 60% equities and 40% fixed income, the Balanced Portfolio. The ‘40’ is the Balanced Portfolio’s 40% allocation to fixed income.

In my mind, the most value will be added in implementation of investment strategies and manager selection.

In addition, the opportunity for Investment Advisors and Consultants to add value to client investment outcomes over the coming years has probably never been more evident now than in recent history.

The value of good investment advice at this juncture will be invaluable.

Putting It All Together

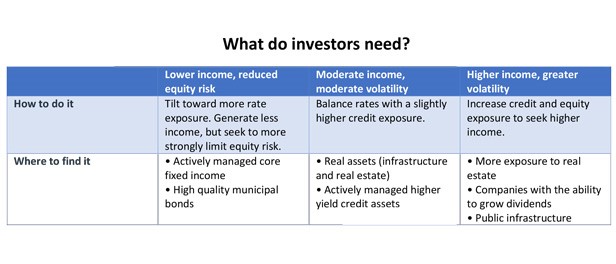

The thinkadvisor.com article provides the following Table.

Source: Nuveen

This Table is useful in considering potential investment ideas. Actions taken will depend on the individual’s circumstances, including investment objectives, and risk tolerance.

The Table provides a framework across three dimensions to consider how to tackle the current investment challenge of very low interest rates.

Those dimensions are:

The trade-off between level of income generated and risk tolerance (measured by portfolio volatility), e.g. lower income and reduced equity risk

“How to do it” in meeting the trade-off identified above e.g. increase credit and equity exposures to seek higher income

“Where to find it”, types of investments to implement How to do it e.g. active core fixed income, real assets (e.g. infrastructure and real estate), higher yielding credit assets.

Current Investment Environment

These insights reflect the current investment environment of extremely low interest rates.

More specifically the article starts with the following comments: “For decades, the 40% in the traditional 60/40 portfolio construction model was supposed to provide stable income with reduced volatility. But these days, finding income in the usual areas is as hard for me as a professional investor as it is for our clients.”

Tony calls for action, “With yields at historic lows, we’re forced to choose between accepting lower income or expanding into higher risk asset classes. We need to work together to change the definition of the 40 in the 60/40 split. So what do we do?”

This would be a worthy discussion for Investment Advisers and Consultants to have with their clients.

Returns from fixed income are relatively predictable, unlike equity market returns. Current fixed income yields are the best predictor of future returns. With global government bond yields around zero and global investment grade credit providing not much more, a return of greater than 1% p.a. from traditional global bond markets over the next 10 years is unlikely.

Fixed income returns over the next 10 years are highly likely to be below the rate of inflation. Therefore, the risk of the erosion of purchasing power from fixed income is very high. This is a portfolio risk that needs to be managed.

Although forecasted returns from equities are also low compared to history, they are higher than those expected from traditional fixed income markets.

What should Investors do?

The article provides some specific guidance in relation to fixed income investments and a view on the outlook for the global economy.

The key point from the article, in my mind, is that for investors to meet the current investment challenges over the next decade they are going to need a more broadly diversified portfolio than the traditional 60/40 portfolio.

I also think it is going to require greater levels of active management.

This will involve a rethink of the ‘40’ fixed income allocation. Specifically, the focus will be on generating higher returns and that fixed income is likely to provide less protection to a Balanced Portfolio at times of sharemarket declines than has been experienced historically.

Ultimately, a broader view of the 60/40 Portfolio’s construction will need to be undertaken.

This is likely to require thinking outside of the fixed income universe and implementing a more robust and truly diversified portfolio.

Implementation will be key, including strategy and manager selection.

There will still be a role for fixed income within a Portfolio, particularly duration. Depending on individual circumstances, higher yielding securities, emerging market debt, and active management of the entire fixed income universe, including duration, is something to consider. More of an absolute return focus may need to be contemplated.

Outside of fixed income, thought should be given to thinking broadly in implementing a more robust and truly diversified portfolio.

Kiwi Investor Blog has highlighted the following areas in previous Posts as a means to diversify a portfolio and address the current investment challenge:

Real Assets offer real diversification: this Post outlines the investment risk and return characteristics of the different types of Real Assets and the diversification benefits they can bring to a Portfolio under different economic scenarios, e.g. inflation, stagflation.

There have been a number of articles over recent months calling into question the robustness of the Balanced Portfolio of 60% Equities / 40% Fixed Income going forward. I have covered this issue in previous Posts, here and here.

Why the Balanced Portfolio is expected to underperform is outlined in this Post.

Lastly, also relevant to the above discussion, please see this Post on preparing Portfolios for higher levels of inflation.

Call to Action

In appealing to Tony’s call for action, there has probably never been a more important time in realising the value of good investment advice and honest conversations of investment objectives and portfolio allocations.

Perhaps it is time to push against some outdated conventions, seek new investments and asset classes.

The opportunity for Investment Advisors and Consultants to add value to client investment outcomes over the coming years has probably never been more evident now than in recent history.

The value of good investment advice at this juncture will be invaluable.

Addendum

For a perspective on the current market environment this podcast by Goldman Sachs may be of interest.

In the podcast, Goldman Sachs discuss their asset allocation strategy in the current environment, noting both fixed income and equities look expensive, this points to lower returns and higher risks for a Balanced Portfolio. They anticipate an environment of below average returns and above average volatility.

Those saving for retirement face the reality that fixed income may no longer serve as an effective portfolio diversifier and source of meaningful returns.

In future fixed income is unlikely to provide the same level of offset in a portfolio as has transpired historically when the inevitable sharp decline in sharemarkets occur – which tend to happen more often than anticipated.

The expected reduced diversification benefit of fixed income is a growing view among many investment professionals. In addition, forecast returns from fixed income, and cash, are extremely low. Both are likely to deliver returns around, if not below, the rate of inflation over the next 5 – 10 years.

Notwithstanding this, there is still a role for fixed income within a portfolio.

However, there is still a very important portfolio construction issue to address. It is a major challenge for retirement savings portfolios, particularly those portfolios with high allocations to cash and fixed income.

In effect, this challenge is about exploring alternatives to traditional portfolio diversification, as expressed by the Balanced Portfolio of 60% Equities / 40% Fixed Income. I have covered this issue in previous Posts, here and here.

Outdated Investment Strategy

There are many ways to approach the current challenge, which investment committees, Trustees, and Plan Sponsors world-wide must surely be considering, at the very least analysing and reviewing, and hopefully addressing.

One way to approach this issue, and the focus of this Post, is Tail Risk Hedging. (I comment on other approaches below.)

The case for Tail Risk Hedging is well presented in this opinion piece, Investors Are Clinging to an Outdated Strategy At the Worst Possible Time, which appeared in Institutional Investor.com

The article is written by Ron Lagnado, who is a director at Universa Investments. Universa Investments is an investment management firm that specialises in risk mitigation e.g. tail risk hedging.

The article makes several interesting observations and lays out the case for Tail Risk Hedging in the context of the underfunding of US Pension Plans. Albeit, there are other situations in which the consideration of Tail Risk Hedging would also be applicable.

The framework for Equity Tail Risk Hedging, recognises “that management of portfolio risk and equity tail risk, in particular, was the key driver of long-term compound returns.”

By way of positioning, the article argues that a reduction in Portfolio volatility leads to better investment outcomes overtime, as measured by the Compound Annual Growth Return (CAGR). There is validity to this argument, the reduction in portfolio volatility is paramount to successful investment outcomes over the longer-term.

The traditional Balance Portfolio, 60/40 mix of equities and fixed income, is supposed to mitigate the effects of extreme market volatility and deliver on return expectations.

Nevertheless, it is argued in the article that the Balanced Portfolio “limits portfolio volatility in benign market environments over the short term while making huge sacrifices in long-run performance.”

In other words, “It offers scant protection against tail risk and, at the same time, achieves an under-allocation to riskier assets with higher returns in long periods of economic expansion, such as the past decade.”

The article provides some evidence of this, highlighting that “large allocation to bonds still failed to provide enough protection to add value over the cycle — reducing the CAGR by 170 basis points.”

Essentially, the argument is made that the Balanced Portfolio has not delivered on its promise historically and is an outdated strategy, particularly considering the current market environment and the outlook for investment returns.

Meeting the Challenge – Tail Risk Hedging

The article calls for the consideration of different approaches to the traditional Balance Portfolio. Naturally, they call for Tail Risk Hedging.

In effect, the strategy is to maintain a higher allocation to equities and to protect the risk of large losses through implementing a tail risk hedge (protection of large equity loses).

It is argued that this will result in a higher CAGR over the longer term given a higher allocation to equities and without the drag on performance from fixed income.

The Tail Risk Hedge strategy is implemented via an options strategy.

As they note, there is no free lunch with this strategy, an “options strategies trade small losses over extended periods when equities are rising for extremely large gains during the less frequent but devastating drawdowns.”

This is the inverse to some investment strategies, which provide incremental gains over extended periods and then short sharp losses. There is indeed no free lunch.

My View

The article concludes, “diversification for its own sake is not a strategy for success.”

I would have to disagree. True portfolio diversification is the closest thing to a free lunch in Portfolio Management.

However, this does not discount the use of Tail Risk Hedging.

The implementation of any investment strategy needs to be consistent with client’s investment philosophy, objectives, fee budgets, ability to implement, and risk appetite, including the level of comfort with strategies employed.

Broad portfolio diversification versus Tail Risk Hedging has been an area of hot debate recently. It is good to take in and consider a wide range of views.

The debate between providing portfolio protection (Tail Risk Hedging vs greater Portfolio Diversification) hit colossal proportions earlier in the year with a twitter spat between Nassim Nicholas Taleb, author of Black Swan and involved in Universa Investments, and Cliff Asness, a pioneer in quant investing and founder of AQR.

I provide a summary of their contrasting perspectives to portfolio protection as outlined in a Bloomberg article in this Post. There are certainly some important learnings and insights in contrasting their different approaches.

The Post also covered a PIMCO article, Hedging for Different Market Environments.

A key point from the PIMCO article is that not one strategy can be effective in all market environments. This is an important observation.

Therefore, maintaining an array of diversification strategies is preferred, PIMCO suggest “investors should diversify their diversifiers”.

They provide the following Table, which outlines an array of “Portfolio Protection” strategies.

In Short, and in general, Asness is supportive of correlation based like hedging strategies (Trend and Alternative Risk Premia) and Taleb the Direct Hedging approach.

From the Table above we can see in what type of market environment each “hedging” strategy is Most Effective and Least Effective.

For balance, more on the AQR perspective can be found here.

You could say I have a foot in both camps and are pleased I do not have a twitter account, as I would likely be in the firing line from both Asness and Taleb!

To conclude

I think we can all agree that fixed income is going to be less of a portfolio diversifier in future and produce lower returns in the future relative to the last 10-20 years.

This is an investment portfolio challenge that must be addressed.

We should also agree that avoiding large market losses is vital in accumulating wealth and reaching your investment objectives, whether that is attaining a desired standard of living in retirement, ongoing and uninterrupted endowment, or meeting future Pension liabilities.

In my mind, staying still is not going to work over the next 5-10 years and the issues raised by the Institutional Investor.com article do need to be addressed. The path taken is likely to be determined by individual circumstances.

“ESG is not an equity return factor in the traditional, academic sense”.…… “Nevertheless, ESG can be a very powerful theme in the portfolio management process in the years ahead.”

These are two key conclusions from a recent Research Affiliates article, Is ESG a Factor?

ESG investing is incorporating Environment, Social and Governance considerations into investment portfolios.

Research Affiliates conclude “that ESG does not need to be a factor for investors to achieve their ESG and performance goals.”

They also call for greater clarity around exactly what ESG is and what it is not.

“Currently, various stakeholders are sending a whole host of mixed messages. Investors, particularly fiduciaries, need education and alignment. If ESG remains a heterogeneous basket of claims, we will likely never see it fulfill its vast promise.”

Lastly, they believe ESG is likely to be a powerful theme for the new owners of capital, in particular woman and millennials. Increasingly investors will prioritise ESG in their portfolios in the years ahead.

In my view, it is a stretch to say ESG is an investment factor in the context of Factor Investing. Nevertheless, the active management of ESG considerations into the investment process has the potential to add value.

You can’t capture the benefits of ESG by just being an ESG investor. Capturing the benefits from ESG are harder to attain relative to implementing an equity factor strategy such as value or low volatility.

The risks, and therefore the rewards of ESG, are more company specific.

Therefore, it is not good enough to say one incorporates ESG into the investment management process to gain the benefits from ESG.

There is no specific ESG factor that can be “harvested” passively. The ESG value add comes from implementing successfully and having the ability to identify company specific ESG risks.

What Is a Factor?

Before we can determine if ESG is an investment factor we first need to establish what an investment factor is.

In short, factors are characteristics associated with long-term risk and return outcomes associated with investing into a group of securities.

The “market”, sharemarkets and fixed income markets are factors themselves (Market Factors). We know that over time we can expect to generate a return over cash, a premia over cash (premia), from investing in sharemarkets, credit markets (corporate debt), and longer-term fixed income securities (interest rate duration).

Within markets there are also investment factors, which have been shown to deliver a premia (excess return adjusted for risk) over the “market factors” identified above.

The most common of these investment factors, and one receiving a lot of media attention currently, is the value factor. There are other well know and academically supported factors, including momentum, carry, quality, and low volatility. Investment factors are also known as Premias or Style Premia.

To be considered a robust investment factor, it is generally considered their needs to be support from an economic perspective or there is a behavioural-based explanation for the factor.

For those interested, I have previously Posted on Factor Investing, and this article on Andrew Ang discussing Factor Investment might also be of interest.

Research Affiliates have their own framework on determining the robustness of a Factor, which can be found here.

The Evidence – Is ESG an investment Factor?

To determine if ESG is a factor, Research Affiliates maintain it should satisfy the following three critical requirements, it should be:

grounded in a long and deep academic literature;

robust across definitions; and

robust across geographies.

Academic Literature

The common factors of value, momentum, and low beta have been thoroughly researched and have a track record spanning several decades, as Research Affiliates conclude “very little debate currently exists regarding their robustness.”

In reviewing the academic literature on ESG, Research Affiliates find little agreement on the robust of generating excess returns. (Their article provides a good source of academic ESG research for those interested.)

In their view ESG is not an equity return factor in the traditional academic sense.

In my mind there is value in undertaking a Responsible Investing approach, including the incorporation of ESG into the investment management process. This can be the case yet ESG not be a Factor as defined in academia. The research covered in the above Post provides support for this view.

Factors should be robust across definitions.

This is an interesting observation. Research Affiliates argue that “even slight variations in the definition of a factor should still produce similar performance results.”

They use value as an example, using different valuation metrics for value results in similar results over the longer-term. The value factor is robust across different definitions of value.

Unfortunately, ESG does not have a common definition and is a broad continuum of philosophies, approaches, and strategies.

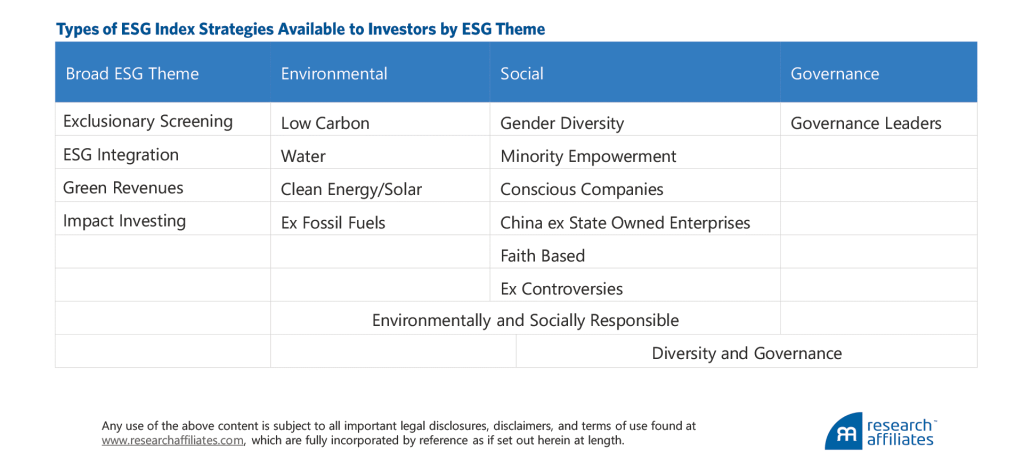

The broad spectrum is highlighted in the following Table presented in the Research Affiliates article to emphasise “ESG has no common standard definition and is a broad term that encapsulates a range of themes and subthemes.”

As they note, the strategies align more with investor preferences rather than a particular investment factor.

In the article Research Affiliates present the findings of their research to display how variations in the definition of ESG results in different performance outcomes.

From this analysis, they conclude:

None of the ESG strategies as defined displayed material excess returns;

There was a lack of historical track record, which is a significant impediment to conducting research in ESG investing; and

Only after decades of quality data will it be possible to accurately test the claim that EG is a robust factor.

Research Affiliates also highlight there is an issue with the lack of consistency among ESG rating providers which hinders the ability to determine if ESG is a robust factor. They provide an example of this in the Article.

With regards to the last requirement, Research Affiliates find that ESG performance results are not robust across regions.

ESG Is Not a Factor, but Could Be a Powerful Theme

“ESG does not need to be a factor for investors to achieve their ESG and performance goals.”

Encouragingly, Research Affiliates see a role for the incorporation of ESG within an investment portfolio. I Agree!

They highlight that there are companies with poor ESG characteristics and that these risks should be incorporated into the stock selection process.

These risks are company specific risks, idiosyncratic risks technically speaking.

Research Affiliates consider carbon as an example, particularly coal. Notably there has been a move away from coal in the US. Therefore, “Investment managers who do not consider and integrate the ESG risk of, in this case, climate change may be blindsided.”

The successful implementation of ESG is a key determinant in capturing the value from company specific characteristics. Specifically, having the ability to identify mispricing of securities due to ESG risk.

It is not good enough to say one incorporates ESG into the investment management process and therefore the portfolios will benefit.

There is no a specific ESG factor that can be “harvested” passively, the value add comes from implementing successfully and having the ability to identify company specific risks.

Increasing Adoption of ESG Investing

Lastly, and quickly, Research Affiliates note that there is a “large shift in investor preference toward ESG is occurring as two distinct groups—women and millennials—take greater control of household assets.” This is backed up by third party research which notes that there will be a wave of assets ready to invest in highly rated ESG companies.

A regulatory push globally is also likely to accelerate this trend.

Likely poor performing investment managers are relatively easy to identify. Great fund managers much more difficult to identify.

Good performing managers who can consistently add value over time can be identified. Albeit, a well-developed and disciplined investment research process is required.

Those managers that consistently add value are likely to be found regularly in the second quartile of peer analysis. They are neither the best nor the worst performing manager but over time consistently add value over a market index or passive investment. They are not an average manager.

These are key insights I have developed from just under 30 years of researching and collaborating with high calibre and talented investment professionals.

More importantly, modern day academic research is supportive of this view. The conventional wisdom of active management is being challenged, as highlighted in a previous Post.

The author, John Paterson, of this analysis was interviewed in a i3 article.

The key points of Peterson’s analysis and emphasized in the i3 article:

Many of the studies into the ability of active managers to consistently outperform are inherently flawed.

Most of these studies merely confirm that financial markets are not static, therefore they do not say anything about manager performance.

“The failure to find repeated top quartile performance in these ‘tests of manager consistency’ simply reflects the reality that markets are not Static, and says nothing about the existence, or otherwise, of manager consistency.”

The key flaw is that many of the studies on active management focus on the performance of only the top performing managers: whether top quartile performers are able to repeat their efforts from one period to the next.

A wider view of manager performance should be considered, all quartiles should be assessed to determine whether manager performance is random or not.

Those managers that that consistently achieved above average returns are more likely to be found in the second or third quartiles.

In the i3 interview, Paterson discusses more about the results of their research:

“Someone who consistently outperforms doesn’t necessarily look like a top quartile manager. They are more likely to be found in the second quartile,”.

The following comment is also made:

“Most asset managers intuitively know this, because markets are cyclical and if you do something that shoots the lights out in one period, it is likely to do the complete opposite in another period.”

The Australian Experience

Paterson’s analysis also found “Across the studies analysed, it was found that there is very strong evidence that investment managers available to Australian superannuation funds do perform consistently.”

Lastly Paterson comments “And experience tells us that super funds with more active managers have done better than those with largely passive mandates, and often at a lower level of volatility.”

Concluding Remarks

As I have previously Posted, there are a wide range of reasons for choosing an alternative to passive investing over and above the traditional industry debate that focuses on whether active management can outperform.

Other reasons for considering an alternatives to a passive index include no readily replicable market index exists, imbedded inefficiency within the Index, and available indices are unsuitable in meeting an investor’s objectives (e.g. Defined Pension Plans).

The decision to choose an alternative to passive investing varies across asset classes and investors.

Therefore, the traditional active versus passive debate needs to be broadened.

The article by Warren and Ezra, covered in a previous Post, When Should Investors Consider an Alternative to Passive Investing?, seeks to reconfigure and broaden the active versus passive debate.

They provide five reasons why investors might consider alternatives to passive management.

In doing so they provide examples of circumstances under which an alternative to passive management might be preferred and appreciably widen the debate.

The identification of managers that consistently add value is one reason to consider an alternative to passive management.

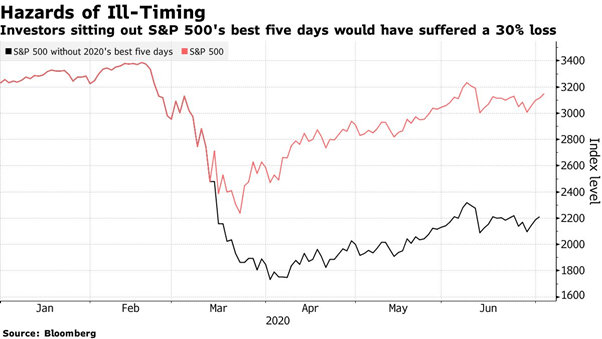

Missing the sharemarket’s five best days in 2020 would have led to a 30% loss compared to doing nothing.

The 2020 covid-19 sharemarket crash provides a timely example of the difficulty and cost of trying to time markets.

The volatility from global sharemarkets has been extreme this year, nevertheless, the best thing would had been to sit back and enjoy the ride, as is often the case.

By way of example, the US S&P 500 sharemarket index reached a historical high on 19th February 2020. The market then fell into bear market territory (a decline of 20% or more) in record time, taking just 16 trading days, beating the previous record of 44 days set in 1929.

After falling 33% from the 19th February high global equity markets bounced back strongly over the following weeks, recording their best 50-day advance.

The benchmark dropped more than 5% on five days, four of which occurred in March. The same month also accounted for four of the five biggest gains.

Within the sharp bounce from the 23rd March lows, the US sharemarkets had two 9% single-day increases. Putting this into perspective, this is about equal to an average expected yearly return within one day!

For all the volatility, the US markets are nearly flat for the period since early February.

A recent Bloomberg article provides a good account of the cost of trying to time markets.

The Bloomberg article provides “One stark statistic highlighting the risk focuses on the penalty an investor incurs by sitting out the biggest single-day gains. Without the best five, for instance, a tepid 2020 becomes a horrendous one: a loss of 30%.”

As highlighted in the Bloomberg article, we all want to be active, we may even panic and sit on the side line, the key point is often the decision to get out can be made easily, however, the decision to get back in is a lot harder.

The cost of being wrong can be high.

Furthermore, there are better ways to manage market volatility, even as extreme as we have encountered this year.

For those interested, the following Kiwi Investor Blog Posts are relevant:

Avoiding large market losses is vital to accumulating wealth and reaching your investment objectives, whether that is attaining a desired standard of living in retirement or a lasting endowment.

The complexity and different approaches to providing portfolio protection has been highlighted by a recent twitter spat between Nassim Nicholas Taleb and Cliff Asness.

The differences in perspectives and approaches is very well captured by Bloomberg’s Aaron Brown article, Taleb-Asness Black Swan Spat Is a Teaching Moment.

I provide a summary of this debate in Table format in this Post.

Also covered in this Post is an article by PIMCO on Hedging for Different Market Scenarios. This provides another perspective and a summary of different strategies and their trade-offs in different market environments.

Not every type of risk-mitigating strategy can be expected to work in every type of market environment.

Therefore, maintaining an array of diversification strategies is preferred “investors should diversify their diversifiers”.

The best way to manage periods of severe sharemarket declines is to have a diversified portfolio, it is impossible to time these episodes.

AQR has evaluated the effectiveness of diversifying investments during market drawdowns, which I cover in this Post.

They recommend adding investments that make money on average and have a low correlation to equities.

Although “hedges”, e.g. Gold, may make money at times of sharemarket crashes, there is a cost, they tend to do worse on average over the longer term.

Alternative investments are more compelling relative to the traditional asset classes in diversifying a portfolio, they provide the benefits of diversification and have higher returns.

Portfolio diversification involves adding new “risks” to a portfolio, this can be hard to comprehend.

One of the key questions facing investors at the moment is whether inflation or deflation represents the bigger risk in the coming years.

Now more than ever, given the likely economic environment in the years ahead, investors need to consider all their options when building a portfolio for their future. This may mean a number of things, including: increasing diversification, investing in new or different markets, being active, and flexible to take advantage of unique opportunities as they arise.

Those portfolios overly reliant on traditional markets, such as equities and fixed income in particular, run the risk of failing to meet to their investment objectives over the next ten years.

Conundrum Facing Investors

A recent article by Alan Dunne, Managing Director, Abbey Capital, The Inflation-Deflation debate and its Implications for Asset Allocation, which recently appeared in AllAboutAlpha.com, clearly outlines the conundrum currently facing investors.

As the article highlights, one of the “key questions facing investors at the moment is whether inflation or deflation represents the bigger risk for the coming years. Economists are split on this….”

Following a detailed analysis of the current and likely future economic environment and potential influences on inflation or deflation (which is well worth reading) the article covers the Implications for Asset Allocations.

Inflation or Deflation: Implications for Asset Allocations

The article makes the following observations as far as asset class performance in different inflation environments, based on historical observations:

Deflation like in the 1930s, is negative for equities but positive for Bonds.

If inflation picks ups, or even stagflation, that would be negative for real returns on financial assets and real assets may be favoured.

They conclude: “the current uncertainty highlights the importance of holding diversified portfolios, with exposure to a range of traditional and alternative assets and strategies with the potential to deliver returns in different market environments.”

Current Environment

Abbey Capital anticipate greater co-ordination of policy between governments (fiscal policy) and central banks (monetary policy).

As they note, “many economists draw a parallel between the current scenario and the substantial increase in government debt during World War II. One of the consequences of higher debt levels is that we may see pressure on central banks to maintain interest rates at low levels and maintain asset purchases to ensure higher bond issuance is not disruptive for bond markets i.e. coordination of monetary and fiscal policies.”

I think this will be the case. The Bank of Japan has maintained a direct yield curve control policy for some time and the Reserve Bank of Australia has implemented a similar policy recently. Direct yield curve control is where the central bank will target an interest rate level for the likes of the 3-year government bond.

In the environment after World War II debt levels were brought back to more manageable levels by keeping interest rates low (a process known as financial repression).

From a government policy perspective, financial repression reduces the real value of debt over time. It is the most palatable of a number of options.

Financial repression is potentially negative for government bonds

With interest rates so low, and likely to remain low for some time given policies of financial repression the real return (after inflation) on many fixed income instruments and cash could be negative.

A higher level of inflation not only reduces the real return on bonds but potentially also reduces the diversification benefits of holding bonds in a portfolio with equities.

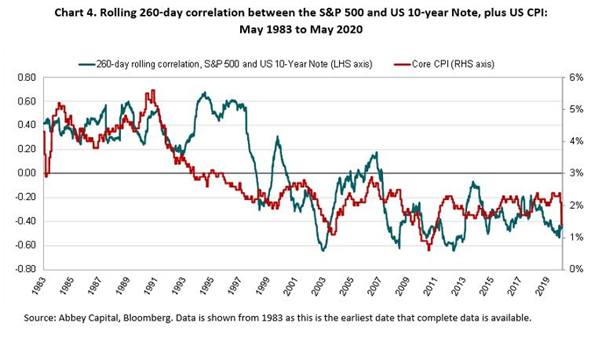

The diversification benefits of bonds in the traditional 60 / 40 equity-bond portfolio (Balanced Portfolio) has been a strong tail wind over the last 20 years.

The more recent low correlation between bonds and equities is evident in the Chart below, which was presented in the article.

The Chart also highlights that the relation of low correlation between equities and bonds, which benefits a Balanced Portfolio, has not always been present.

As can be seen in the Chart, in the 1980s, when inflation was a greater concern, inflation surprises were negative for both bonds and equities, they became positively correlated.

What should investors do?

“Investors are therefore left with the challenge of finding alternatives for government bonds, ideally with a low or negative correlation to equities and protection against possible inflation.”

The article runs through some possible investment solutions and approaches to meet the likely challenges ahead. I have outlined some of them below.

I think duration (interest rate risk) and credit can still play a role within a broad and truly diversified portfolio. Within credit this would likely involve expanding the universe to include the likes of high yield, securitised loans, private debt, inflation protections securities, and emerging market debt as examples.

The key and most important point is that a robust portfolio will be less reliant on tradition asset classes, traditional asset class betas, to drive investment return outcomes. This is likely to be vitally important in the years ahead.

Accordingly, investors will need to be more active, opportunistic, and maintain very broad and truly diversified portfolios. Not only within asset classes, such as the fixed income example provided above, but across the portfolio to include the likes of real assets and liquid alternatives.

Real assets

Abbey Capital comment that “Real assets such as property and infrastructure should provide protection against higher inflation for long-term investors but may not be attractive for investors valuing liquidity.”

Although the maintenance of portfolio liquidity is important, Real assets can play an important role within a robust portfolio.

For the different types of real assets, their investment characteristics, and likely performance and sensitivity to different economic environments, including economic growth, inflation, inflation protection, stagflation, and stagnation please see the Kiwi Investor Blog Post, Real Assets Offer Real Diversification. The extensive analysis has been undertake by PGIM.

Liquid Alternatives

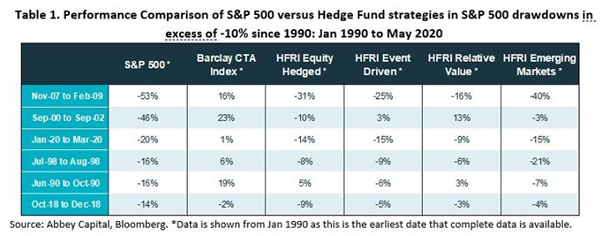

Abbey Capital provide a brief discussion on liquid alternatives with a focus on managed futures. Not surprisingly given their pedigree.

They provide the following Table which highlights the benefit of liquid alternatives and hedge funds at time of significant sharemarket declines (drawdowns).

Concluding Remarks

Being a managed futures manager, it is natural to be cautious of Abbey Capitals concluding remarks, being reminded of the Warren Buffet quote, “Never ask a barber if you need a haircut.”

Nevertheless, the Abbey Capital’s economic analysis and investment recommendations are consistent with a growing chorus, all singing from a similar song sheet. (Perhaps we could call this a “Barbers Quartet”!)

Without having an axe to grind, and in all seriousness, I have covered similar analysis and comments in previous Posts, the conclusions of which have a high degree of validity and should be considered, if not a purely from portfolio risk management perspective so as to understand any gaps in current portfolios for a number of likely economic environments.

The key and most important point is that robust portfolios will be less reliant on traditional asset classes, traditional asset class betas, to drive investment return outcomes.

Accordingly, investors will need to be more active, opportunistic, and maintain very broad and truly diversified portfolios

Therefore, it is hard to disagree with one of the concluding remarks by Abbey Capital “To account for the competing requirements in a portfolio of returns, low correlation to equities, liquidity and possible inflation protection, investors may need to build robust portfolios with a broader mix of assets and strategies.”

Other Reading

For those interested, previous Kiwi Investor Blog posts of relevance to the Abbey Capital article include:

Preparing your Portfolio for a period of Higher Inflation, this is the Post of most relevance to the current Post, and covers a recent Man article which undertook an analysis of the current economic environment and historical episodes of inflation and deflation.

Man conclude that although inflation is not an immediate threat, the likelihood of a period of higher inflation is likely in the future, and the time to prepare for this is now. Man recommends several investment strategies they think will outperform in a higher inflation environment.

It also includes analysis by PIMCO, where it is suggested to “diversify your diversifiers”.

Lastly, Sharemarket crashes – what works best in minimising losses, market timing or diversification, covers a research article by AQR, which concludes the best way to manage periods of severe sharemarket decline is to have a diversified portfolio, it is impossible to time these episodes. AQR evaluates the effectiveness of diversifying investments during sharemarket drawdowns using nearly 100 years of market data.

There are a wide range of reasons for choosing an alternative to passive investing over and above the traditional industry debate that focuses on whether active management can outperform an index.

Reasons for considering alternatives include no readily replicable market index exists, available indices are unsuitable in meeting an investor’s objectives, and/or there are some imbedded inefficiency within the Index.

Under these circumstances a passive approach no longer becomes optimal nor appropriate.

Or quite simply, an active manager with skill can be identified, this alone is sufficient to consider an alternative to passive indexing.

Importantly, the decision to choose an alternative to passive investing is likely to vary across asset classes, investors, and time.

Also, the active versus passive debate needs to be broadened, which to date seems too narrowly focused on comparing passive investments with the average returns from active equity managers.

Framework for choosing an Alternative to Passive Investing

They do this by presenting a framework for a more comprehensive consideration of alternatives to passively replicating a standard capitalisation-weighted index in any particular asset class.

In doing so they provide examples of circumstances under which a particular alternative to passive management might be preferred.

They offer no conclusions as to whether any specific approach is intrinsically superior. “Indeed, the overarching message is that best choices can vary across asset classes, investor circumstances, and perhaps even time.”

Warren and Ezra provide the following Framework for choosing an Alternative to Passive Investing:

Their framework appreciably widens the range of reasons for choosing an alternative to passive investing.

As can be seen in the Table above, they have identify five potential reasons investors should seek an alternative to passive index.

The first three reflect situations where a passive index is either unavailable or unsuitable, and two relate to investor expectations that active management can outperform passive benchmarks.

Below I have provided a description of the five reasons investors should seek an alternative to passive index.

Back ground Comments

Warren and Ezra provide some general comments on the state of the industry debate:

They think it is unreasonable to base broad conclusions about the relative efficacy of passive indexing on active managers’ average results in a single asset class or subclass, such as U.S. equities. They note, “What holds true in one market segment may not hold in another.”

They also object to the “implicit assumption that in the absence of demonstrable stock-selection skills among managers, passive index replication provides optimal exposure for investors.” This assumption does not take into account differences in investor objectives and circumstances. This is one of the core points of their article.

They maintain, what is missing in the industry debate is “recognition that appropriate structuring and management of investments may well depend on investors’ relative situations.”

Some Context

The default position for passive investing is a capitalisation-weighted (cap-weighting) index, such as the New Zealand NZSX 50 Index and US S&P 500.

Although somewhat technical, the application of a cap-weighting index rests on the three assumptions outlined below.

A breach in any of the following assumptions could justify giving consideration to an alternative approach to passive indexing.

Market efficiency.

Cap-weighting should be chosen under an assumption of perfectly efficient markets, where prices are always correct. Investors may consider alternatives if they believe markets are not fully efficient and that the repercussions of any inefficiencies can be either avoided or exploited.

Cap-weighting is aligned with investor objectives.

It is assumed that cap-weighting indices are aligned with investor objectives. However, this is not always the case. As we see below, a Defined Benefit plan most likely has different objectives relative to a cap-weighted fixed income index.

The same is true for an endowment, insurance company, or foundation.

Index efficacy.

The view of passive indexing as the default assumes that an index is available for the intended purpose. The theoretical view calls for indexes that effectively embody the market portfolio. The industry view requires indexes that deliver the desired type of asset class exposure. In practice, it is possible that for a given asset class no market index exists, or that available indexes have shortcomings in their construction.

The five reasons below for when investors might prefer an alternative to a passive approach are in situations where these three critical assumptions for passive indexing are broken. In such situations passive index is likely to be inappropriate.

The reasons below, also highlight the point that the active versus passive debate often fails to take into account differences in investor objectives and circumstances. The debate needs to be broadened.

Reason #1: No Readily Replicable Index is Available

Passive investing assumes an effective index exists that can be easily and readily replicated.

In some instances, an appropriate index to replicate is simply not available, for example:

Unlisted assets such as Private Equity, unlisted infrastructure and direct property

Within listed markets were a lack of liquidity exists it becomes difficult to replicate the index, such as small caps, emerging market equities, and high-yield debt.

In these incidences, although a passive product may be available, they “might not deliver a faithful replication of the asset class at low cost.” Accordingly passive investing is not appropriate.

Reason #2: The Passive Index Is at Odds with the Investor’s Objectives

Often a passive index is badly aligned with an investor’s objectives. In such cases an alternative approach may better meet these objectives, often requiring active management to deliver a more tailored investment solution.

By way of example:

Defined Benefit Pension Plan and tailored fixed-income mandates.

Best practice for a Defined Benefit (DB) plan is to implement a tailored fixed income mandate that closely matches expected liabilities.

In such a case a passive index approach is not appropriate given the duration and cashflows of the DB plan are unique and highly unlikely to be replicated by an investment into a passive index based on market capitalisation weights.

DB plan managers may also likely prefer more control over other exposures, such as credit quality relative to a passive index.

Such situations also exits for insurance companies, endowments, and foundations.

Notably, an individual investor has a unique set of future liabilities, represented by their own cashflows and duration. Accordingly, investing into a passive market index product may not be appropriate relative to their investment objectives. A more active decision should be made to meet cashflow, interest rate risk, and credit exposure objectives.

Listed infrastructure provides another example where the passive index may be at odds with the investor’s goals. Some investors may want to target certain sectors of the universe that provides greater inflation protection, thus requiring a different portfolio relative to that provided by a passive market index exposure.

The article also provides example in relation to Sustainable and ethical investing and Tax effectiveness.

Reason #3: The Standard Passive Index is Inefficiently Constructed

Where alternatives are available, it makes no sense to invest in an inefficient index. This represents a suboptimal approach, particularly if an alternative can deliver a better outcome.

The article presents two potential reasons an index might be inefficient and proves three examples.

They comment that an index might be inefficient for the following reasons:

the index is built on a narrow or unrepresentative universe; and

the index is constructed in a way that builds in some inefficiency.

As they highlight, these issues are best outlined through the discussion of examples. I briefly cover two.

Equities

Alternative indexing/passive approaches such as factor investing and fundamental investing are “active” decision relative to a market-capitalised index.

The basis for these alternative approaches is that equity capital market indices are flawed (Fundamental Investing) and inefficient (e.g. factor investing such as value and small caps outperform the broader market over time).

Fixed income

There are many shortcomings of fixed-income indices, the article focuses on two:

Fixed income indices do not fully represent the asset class. Therefore, more efficient portfolios may be built by including off-benchmark securities.

The largest issuers dominate fixed income indices and it can be argued these are the less attractive governments/companies to invest in, because they are most in need of funding (and hence of lower quality), or are issuing debt to take advantage of low interest rates, which are unattractive to the investor.

Reasons #4 and #5 The final two reasons are more aligned with the traditional question of whether investors can access managers that can be expected to outperform the index.

Reason #4 features that could lead to active investment managers outperforming the passive alternative in aggregate.

Active management is often defined as a zero-sum game before transaction costs, and a negative-sum game after transaction costs. Therefore, active management as a whole cannot outperform.

However, this dynamic need not apply to all investors and it is quite likely that there is a subsector of investors that can consistently outperform the index.

Therefore, a review of the environment in which managers operate might establish if they are able to maintain a competitive advantage.

The following features are outlined in the article to support such a situation:

Market inefficiency situations

Market inefficiencies offer the potential for active managers to outperform the index, nevertheless managers need to be appropriately placed to capture any excess rewards of these inefficiencies.

The following situations may provide a manager with a competitive advantage:

Information advantage: An active manager could have an advantage where the market is “widely populated by less-informed investors” e.g. emerging markets and small caps.

Preferential access to desirable assets: e.g. where active managers have better access to initial public offerings and sourcing lines of stock. In unlisted markets private equity manager has well established relationships and ability to provide capital and/or appropriate skills.

Economic value-add: e.g. in unlisted assets active management can add value to the underlying asset.

Opportunities arising from differing investor objectives

Opportunities for active management to benefit may exist when:

Some investors are comfortable with earning below-market returns e.g. investors who place greater weight on liquidity or are not willing to accept certain risk exposures

Investors have differing time horizons e.g. value investors exploit short-term focus of markets

Index fails to cover the opportunity set

The article makes the following points under this heading:

There is the potential to outperform by investing outside the index whenever the index does not provide a comprehensive coverage of the available market

The intensity of competition is also a factor in success or otherwise of an active manager. For example, the results on manager skill of the highly institutionalise US market may not translate into other markets and asset class where competition is less fierce.

Cyclicality of markets needs to be considered, with managers likely to perform in different market environments i.e. they tend to underperform when cross-sectional volatility is low, or markets are driven more by thematic forces. As they note, this has limited relevance in the long run, but may add a “timing element to any evaluation of active versus passive investment.”

Reason #5: Skilled Managers Can Be Identified

Where a skilled manager can be identified, this is a sufficient condition to adopt an alternative to passive management alone.

Nevertheless, the ability and capacity to identify a skilled manager is necessary where an alternative to passive management is to be contemplated.

The discussion makes the following points:

At the very least bad managers should be avoided

Markets can never be perfectly efficient, therefore some room exists for outperformance through skill

Not all fund managers are created equal, some are good and some are bad

The research capability and skill to identify and select a manager is an important consideration.

Implementation and Costs

It is important to note, the framework aims first to work out whether there is a case for rejecting a passive index default. The next step is then to ask how much an investor is willing to pay and how the alternative can be accessed.

“In most cases this alternative will be what is traditionally known as “actively managed investing.” In other circumstances this need not be the case, or the skills-based component may be minor.”

The cost versus the benefit and accessing the preferred alternative approach to passive index are key implementation issues.

Concluding Comments

Warren and Ezra make the point that too much of the debate on active versus Passive relies on the analysis of US equities, they think it is unreasonable to base broad conclusions about the efficiency of passive indexing on a single asset class or subclass.

For the record, please see this Post, Kiwi Wealth caught in an active storm, on my thoughts on the active vs passive debate, we really need to move on and broaden the discussion. The debate is not black vs White, as highlighted in this article, there are large grey areas.