It is estimated US public pension plans would need to leverage a Balance Portfolio of 60% equities and 40% fixed income by 47% to achieve their 7.25% actuarial return target in the years ahead.

Such is the challenge facing all investors in the current low interest rate environment.

Investors face some very tough decisions in the future and may be forced to consider significant asset allocation shifts. Increasing the tolerance for risk and illiquidity are likely actions required to boost future investment returns.

Investors are going to have consider something different, from a return perspective, buying bonds is not going to cut it. Likely actions may include considering substitutes to fixed income to provide portfolio stability and some diversification during periods of equity market weakness.

The reality is that asset allocation decisions can only do so much.

These are the key conclusions from an article written by Rob Croce, PhD, of Mellon and Aaron Filbeck, that recently appeared in AllAboutAlpha.

The article covers three potential solutions for investors to consider in boosting future investment returns.

Meeting the Pension Fund Challenge

The above conclusions are determined in the context of the challenge facing US public pension plans.

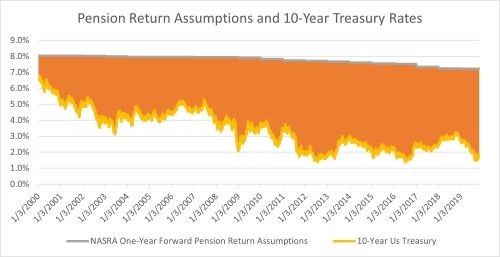

On average US pension plans currently have target returns assumptions of 7.25% on average, this is down from 8% in 2000.

In the year 2000, US 10-year government bond interest rates were 6%. Therefore there “was little headwind to meeting return objectives”….

However, with the dramatic fall in interest rates over the last 20 years, the “gap” between long-term interest rates and return assumptions has widened materially. This is highlighted in Figure 1 below, from the article.

The gap is currently around 6%, compared to 2% in 2000!

Source: NASRA, Bloomberg, CAIA calculations

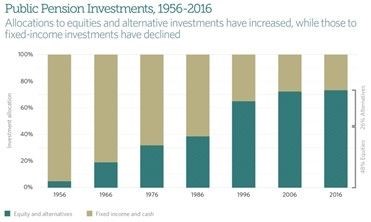

What have US pension plans done over the last 20 years as the return gap has widened:

- Reduced their allocations to fixed income;

- Allocated more to equities; and

- Allocated more to alternatives.

“ According to Public Plans Data, from 2001 to 2009, the average pension allocation to alternative investments increased from 8.7% to 15.7%, which only accelerated after the Global Financial Crisis (GFC). Over the next decade, allocations to alternatives nearly doubled, reaching nearly 27% by the end of 2019.”

The increased allocation to Equities and Alternatives at the expense of fixed income is highlighted in the following Figure also provided in the article.

Source: Pew Research. Data as of 2016

At the same time US pension plans remain underfunded.

The challenge facing US pension plans has been known for some time, the article notes, “In general, pension trustees seem to be faced with two potential solutions – take on more (or differentiated) risks or improve funding statuses through higher taxation or slashing benefits.”

How big is the Pension Fund Return Challenge?

The article analyses potential solutions to “filling the gap” between current interest rates and the assumed target rate of return for US pension funds.

The first approach uses risk premia-based analysis, focusing on the amount of return that can be generated over and above holding just risk-free short-term US Government bonds.

Starting with a traditional Balanced Portfolio, 60% domestic stocks and 40% U.S. 10-year bonds, the analysis seeks to determine how much risk would need to be taken to reach the 7.25% return target. Assuming historical return premia, but with the current level of interest rates.

In relation to return assumptions, the Article notes “Since 1928, stocks have outperformed the risk free asset by 6.2% at 20% volatility and 10-year U.S. government bonds have outperformed the risk-free asset by 1.5%, for Sharpe ratios of 0.3 and 0.2, respectively. For cash, we have decided to use its current near-zero return, rather than its 3.3% average return during that period.”

The results, “there is effectively no unlevered portfolio of stocks and bonds that can reliably deliver many investors’ 7.25% target return over time. Because of the nature of the problem, the solution will likely force pension investors to consider taking on leverage.”

This reflects the low interest rate environment, returns on equities will be lower on an absolute return basis. Although equities are still expected to earn a “premium” above cash, the absolute return will be lower given the cash rate is so low (0%). The 6% equity premium is earnt on 0%, not the average 3.3% cash rate since 1928.

The article estimates, for the Balance Portfolio to achieve the 7.25% return objective it would need to be levered by 47%. This would increase the Portfolio’s volatility to 17.75% from 12%.

As they note, this is not a sustainable solution. Nevertheless, it provides an indication of how much more risk needs to be taken to achieve the 7.25% return target in the current low interest rate environment.

Therefore, the article highlights the return challenge all investors face. The leveraging of portfolios is not going to be a viable option for most investors.

The Potential Role of Alternatives

The article looks at two “hypothetical alternative allocations as potential solutions for U.S. pension funds to hit their 7.25% return, one illiquid and the other liquid.”

- Private Equity (illiquid).

- Hedge Funds or Diversified Assets (liquid)

Their analysis seeks to achieve the return outcome of 7.25% with less volatility than the levered Balance Portfolio above of 17.75% with an allocation to Private Equity and Liquid Alternatives separately.

Based on their analysis, and assumptions, they conclude the inclusion of Private Equity and Liquid Alterative strategies could help in reaching the 7.25% return assumption.

They note that Private Equity and Liquid Alternatives are “two examples provide different solutions for the same problem”.

The article also notes that there are many strategies that do not make sense e.g. anything that takes them further from their return target for the sake of diversification or anything illiquid with an expected return below their target portfolio return.

Key insights

The article wraps up with some key insights, including “buying bonds isn’t going to cut it from a return target perspective today,”…..

They also demonstrated that to meet return targets US pension plans are going to have consider something different. “And while each pension fund is different, risk tolerance and liquidity needs will need to be managed.”

“We think that the current, low yield environment could potentially open institutions up to the idea of using low-risk liquid absolute return strategies as substitutes for fixed income investments. We believe they will increasingly look for investments that provide portfolio stability values and some diversification during risk-off environments, similar to that of traditional fixed income, but potentially provide the return of fixed income two decades ago.”

Reading this article made me think of the following John Maynard Keynes quotes:

“The difficulty lies not so much in developing new ideas as in escaping from old ones.”

“When my information changes, I alter my conclusions. What do you do, sir?”

“It is better to be roughly right than precisely wrong.”

Please see my Disclosure Statement